Small Cap Mining: October Review

It's good to hit some home runs

Good Morning Team.

As we enter the fourth quarter, it strikes me that AIM and the wider small cap world is feeling alive again.

If you’d simply bought the AIM All-Share or AIM 100, you’d be up roughly 7-8% year-to-date.

That’s right.

If you’d not even tried to pick any stocks, the small caps are delivering the same return as if you had invested in LGEN (though who doesn’t love dividend day?)

Looking at junior resource, I can only see good days ahead.

If you have a decent asset, reasonable management and a bit of cash in the bank, then investors, brokers and even market makers are going to treat you better going forward.

In fact, I’d go so far as to say that we will see the sector eclipse the pandemic runs over the next few years.

But before we consider resources, a moment on the crumbling UK government.

The Prime Minister is a barrister who cannot distinguish truth from fiction.

He’s also the least popular UK PM, ever.

The Chancellor outright lied on her CV.

The Deputy PM (in charge of housing) was fired for stamp duty fraud.

The anti-corruption minister was charged with corruption.

The Business Secretary pretended to be a solicitor.

Oh and David Lammy, Darren Jones & Torsten Bell are running things behind the scenes - the man who called Trump a ‘woman-hating, neo-Nazi-sympathising sociopath’ is the new Deputy PM, the chap who said that the majority of Channel migrants were ‘children, babies and women’ is the Minister for Intergovernmental Relations and the guy who wants to tax all wealth into the dirt is running the pensions brief.

These are not serious people, and the writing is on the wall.

Deutsche Bank calculates that since taking office, the government has pushed through tax hikes worth almost 9 times the amount it has raised through spending cuts.

This is equivalent to £235.7 billion over this parliament in tax rises compared to just £27.1 billion of fiscal reductions. And that’s including the previous welfare reforms that have since been cancelled.

5.5% on the 30-year is hideous, and it’s not going to get better, because the UK is not a mate you’d want to lend your money to.

Reeves is stuck between a rock and a hard place - I covered the potential November tax rises for a client last week - but the bottom line is that her government refuses to rein in spending…and every tax rise from here will only damage growth.

To the extent that whatever tax rises she implements means we will just be right back here a few months down the road.

Anyway, Japan’s 30-year yield hit 3.30%, the highest level in history earlier this month. It’s calmed down a bit, but I’ve warned in the past on what this might mean.

With the US Dollar devaluing and Japan uninterested in buying US debt, this might all end in tears.

Golden Years

Speaking of the US, remember when US Secretary of the Treasury Scott Bessent told us that:

‘The entire global trading system until Richard Nixon took us off was tied to gold.’

Well now the US Treasury’s gold reserves have surpassed $1 trillion in value, more than 90 times what’s stated on the government’s balance sheet.

The world’s biggest pile of gold passed the milestone (assuming it’s actually there) after prices rose above $3,824.50 an ounce on Monday.

Its official value, however, is based on the $42.22 an ounce price set by Congress in 1973, fixed at just over $11 billion.

Yeah, gold’s not got more expensive. The Dollar has collapsed.

While another government shutdown looms (because despite the bravado, the US has the same fiscal issues as the UK, but on steroids), it’s worth considering my view that the US may move back to a gold standard.

But even if it doesn’t do this, the temptation to revalue its gold stockpile using current pricing would generate nearly $1 trillion for the coffers.

The problem, of course, is that it would only be theoretical. The US can’t sell its gold unless to another large buyer (China most likely), and this would allow China to launch its own Yuan-backed gold standard that much easier, making it a real competitor to USD for the global currency.

But if you think the US won’t revalue, consider that Italy, Germany and South Africa all did in recent decades.

Or just consider Roosevelt.

He confiscated virtually every scrap of gold in the United States - because back in 1933 (the Great Depression) - the US was on the gold standard, and everyone was hoarding their pet rocks.

Executive Order 6102 ordered that all persons had to deliver their gold to the Federal Reserve or a bank by 1 May 1933, with violators fined up to $10,000 in 1933 money, and/or 10 years in prison.

Those who coughed up were paid $20.67 per ounce, and then a year later under the Gold Reserve Act, the government revalued gold from to $35/oz, devaluing the US dollar by about 40%.

History tends to rhyme - the UK had something mildly similar in the form of the Exchange Control Act 1939, which lasted until 1979…right around the time fiat got properly started.

After the 2008 Global Financial Crisis, Bitcoin was launched - perhaps in response to the broken financial system - and now we may have a war between the traditional and the digital for a new system.

I expect physical gold represented on a global blockchain, with the metal assigned NFTs for tracking…but I digress.

The key point to consider is that gold is still rising.

Newmont and Barrick’s CEOs are both gone - perhaps because a mega-merger is coming.

Jefferies is targeting $6,600.

Morgan Stanley CIO Mike Wilson has shattered the illusion of the 60/40 portfolio and officially recommended a 60/20/20 portfolio strategy, with a 20% allocation to gold.

This isn’t some lunatic with a keyboard like yours truly, he’s a big gun telling the world that the rules of Bretton Woods no longer matter.

Critical Chokepoints

In critical minerals, the news flow in recent weeks tells another clear story.

Metals are no longer a niche corner of the commodities market.

They’re becoming the foundation of global power.

Governments and corporations alike are scrambling to secure access, build reserves, and scale production. Commodity pricing will follow, and then so will share prices.

India is now considering a strategic reserve of critical minerals for emergency use including copper, lithium, rare earths and cobalt. Further sovereign reserves will continue to drain supply, and spot markets will tighten further.

Meanwhile, Germany has struck lithium. In Saxony-Anhalt, geologists uncovered 43 million tonnes of lithium carbonate equivalent - enough to underpin Europe’s dreams of sovereign electric vehicle production. This could reset the balance of power in EV supply chains, but developing the mine, financing processing and scaling downstream industries will take time.

The United States government - not satisfied with only MP Materials - is now in talks to take equity stakes in multiple critical mineral companies.

Washington is moving from rhetoric to ownership in a recognition that the free market cannot guarantee secure supply chains when China invests directly.

Perhaps too little, too late - but Greenland, Ukraine and the DRC will be beneficiaries if past rhetoric is anything to go by.

AMRQ anyone?

At the same time, copper - the backbone of electrification - faces a series of crippling supply shocks:

Ivanhoe Mines’ Kamoa-Kakula, Africa’s largest copper project, hit by seismic activity and flooding

Freeport-McMoRan’s Grasberg mine in Indonesia, responsible for ~3% of global copper supply, sidelined

Teck’s QB2 in Chile still struggling to ramp up

Codelco, the world’s top copper producer, hit by tragedy at El Teniente

Hudbay and MMG operations in Peru again rattled by social unrest

All these blows tighten a market already undersupplied, and which was already hit by tariffs shock — and that’s before demand from EVs and grid upgrades hits full stride.

Like the US, the wider G7 and European Union are now weighing price floors to stimulate rare earth production. That means coordinated market intervention - ensuring that miners earn enough to invest in new projects even when prices fall.

And finally, in a little reported item, China has centralised control of its mineral resources law under the Ministry of Natural Resources.

The message is clear:

Minerals are policy tools, and resource stocks are now defence stocks.

The US Bubble

September saw China ban Nvidia chip sales (it remains to be seen whether the Singapore loophole remains open).

If not, expect some pain.

But consider the infinite money glitch:

Step 1: Oracle announced it will spend $40 billion on Nvidia GPUs - about 400,000 GB200 AI accelerators - for a Texas data centre. Oracle isn’t using them itself; it will lease the capacity to OpenAI.

Step 2: Nvidia announces it’s investing $100 billion into OpenAI.

Step 3: OpenAI commits to spend $300 billion with Oracle for cloud compute — financed by…..Oracle.

And around we go: Oracle pays Nvidia → Nvidia invests in OpenAI → OpenAI pays Oracle → Oracle pays Nvidia → Nvidia invests in OpenAI.

If this looks familiar, it’s because we’ve seen the prototype with CoreWeave. Nvidia also signed a $6.3 billion deal with the company — but with a kicker:

Nvidia supplies GPUs to CoreWeave and books it as a sale.

If CoreWeave can’t place the capacity, Nvidia is contractually obligated to buy it back.

CoreWeave is guaranteed profits whether or not there’s real demand.

In accounting terms, this is just consignment with extra steps, except Nvidia treats it as revenue. Under normal rules, the SEC would question whether unsold GPUs should remain on Nvidia’s balance sheet.

But the regulator has bigger fish to fry right now.

But let’s consider: Oracle’s ‘$300 billion OpenAI commitment’ headline sent its stock up 36% in a single day — its best move since 1992. Google is up 25% in a month.

Is this growth or not?

The economy is circular by nature, but this seems incestuous.

Moving on.

The Golden Trio

Starting with Greatland Resources.

Last month, I noted that:

‘So if GGP gets in, expect volume to rise significantly between 15-19 September.

Of course, everyone knows this and will try to get a quick profit, so this may all be priced in - but the uncertainty over inclusion means it may not be.

But I would assume this could be a very good month. Putting aside the recent mis-step, consider just how much money is being made at Telfer - and it’s not even the real prize.’

Interestingly, the rise began the week after the inclusion, not the week before. This is uncommon, and feeds into the games narrative. But it’s still up >20% in the month and 175% year-to-date, with more to come.

I compared it recently to Genesis, and while I have long held a plan to sell at £4 a share…I may yet be convinced to hold for £5+.

Of course, you might be thinking this is because of the Havieron Feasibility Study or Decision to Mine. Or the tons of assays to come back from the drilling. Or the insane profit margins. Or the undervaluation compared to every one of its ASX peers.

No.

it’s because we should be in the £4+ region already, and the only reason why we’re not is a pack of shorters using every trick in the book to drive the stock lower.

Well you can’t fight the fundamental reality of $3,800 gold.

And I am not going to sell because it gives them what they want. They don’t want to cash in on the short - they want to get stock cheaply en masse.

They’re not having mine unless they pay for it.

And having given them the warning to get out last month, I want to watch these fuckers burn.

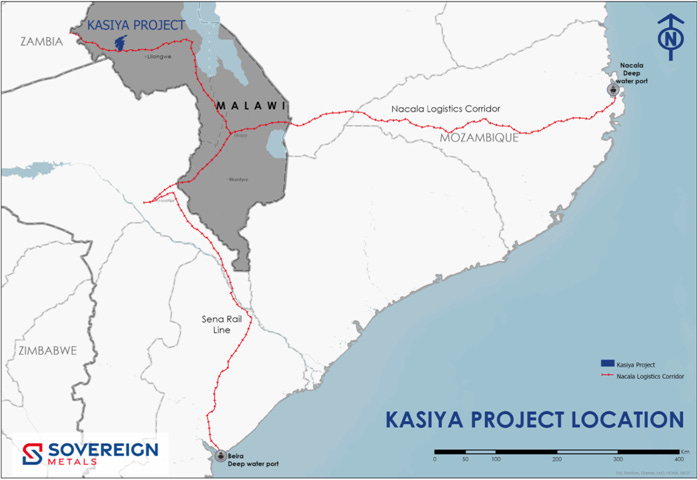

Sovereign Metals saw Japan launch its new Nacala Logistics Corridor development initiative in September - fresh off the back of Toho approving Kasiya’s premium rutile.

Japan has committed $7 billion in development funding, including $5.5 billion through a joint program with the African Development Bank.

As a reminder, the Nacala Corridor is already Kasiya’s preferred transport route, as it provides the lowest cost pathway from Kasiya to international markets via the deep water port.

Japan’s PM even noted in a keynote speech that the country was launching:

‘a new region-wide co-creation for common agenda initiative that promotes logistics in the Nacala Corridor, which contributes to strengthening mineral resource supply.’

There’s £26.7 million in the bank, a Mineral Resource Update that looks set to surprise to the upside - it’s already the largest rutile and second-largest graphite deposit in the world - and the recent raise was at 41.5p, a significant premium to the current share price.

The NPV could rocket if the new resource numbers rise significantly, and with billions to be spent on logistics already - this thing is betting built or sold soon.

Amaroq enjoyed a better month in September, rising back to the circa 70p mark.

Limited news this month, but this was to be expected. They’re getting the hard work in - optimisation of Nalunaq - and some serious drilling.

CFO Ellert Arnarson delivered a company presentation at the Mining Forum Americas in Colorado Springs (several other grandees were in attendance), but the big catalyst other than gold production is Nanoq.

Consider the pictures first:

Yes, it’s pretty.

But the rumours are that the cores are prettier.

Consider 2026: Cannacord is talking 36,000 ounces of production from Nalunaq in 2026. Times that by $4000 an ounce....

$144 million. A year.

The market cap is $430 million, give or take.

If you have access to Cannacord’s note today, the number’s being floated is a 2027 EBITDA forecast of $178 million.

This means more than enough money to fund all the additional exploration work at Nanoq, Black Angel and Kangerluarsuk, and Gardaq.

They’ve also increased their target by 9% to 120p.

8500m of drilling + additional exploration.

Massive raise at premium to the current share price, fully funded.

US equity involvement on the cards.

Even if there are fewer ounces, or a lower gold price next year, there’s no way this stock stays here.

With GGP up 175%, SVML down 6% and AMRQ down 32%, we’re averaging 46% up right now - I expect this to be even better by the end of Q4.

The Explorers

Rome Resources is appointing Stephane Mutombo Irung as a non-exec; a representative of Stanvic Mining SARL, which undertook a strategic investment in Rome towards the end of 2024.

This is good news - further funding for exploration may be forthcoming, especially post-MRE and with IRH likely also interested given their substantial investment in Alphamin next door.

I’ll keep banging this drum, but the Rome team discovered Alphamin’s Bisie.

In the meantime, assays from Mont Agoma have returned, including a newly identified eastern tin zone, which among other results saw MADD030A deliver:

23.1m at 0.42% Sn from 3m, including 0.45m at 1.56% from 8.6m, 12.2m at 0.75% Sn from 12.3m, including, 1.6m at 1.42% from 13.5m and 5.0m at 0.92% Sn from 19.5m including 1m at 1.67% from 22m

CEO Paul Barrett enthuses that:

‘These latest assay results underscore the high-value potential of Mont Agoma. The tin grades we are seeing are excellent…

…Our immediate focus is to finalise the maiden MRE with MSA for both Mont Agoma and Kalayi. This is expected to set the foundation for the next phase of the project - drilling out the new eastern tin zone, undertaking deeper drilling in the main Mont Agoma zone, and stepout drilling at the Kalayi tin project…

At the reporting date, a total of 5,143 metres have been drilled in this campaign…

…Tin, copper, zinc and silver are all heavily represented in the Mont Agoma discovery and are expected to form an integral part of the mineral resource going forward.’

It’ll be spicy.

Arc Minerals is going to see a resolution to the ongoing legal dispute in short order.

Like it or not, this is part and parcel of investing in a frontier. If you’re not constantly defending your licences, they’re probably not very good.

I won’t comment further at this juncture, but I will note that I said last month:

‘I also have it from an excellent source unrelated to Arc & Anglo that another FTSE 100 major (not Anglo American) which was seriously considering an investment in Zambia has cited this case as a reason why they are hesitant to invest. If the country wants western investment to continue, this sort of nonsense needs to stop.’

This week, HH is conducting a three day visit to the UK this week meeting with King Charles at Balmoral - and then events in London.

Coincidence?

I’ll let you decide.

As an aside, Midnight Sun - which is probably the closest comparator to Arc - is rocketing.

Sentiment can change at the drop of a hat.

Rome is down 10% year-to-date and Arc is now flat. However, given the spread on both stocks, there’s basically nothing in it.

I’ll bet both are winner by the end of the year. Three months to go!

The dealmakers

Asiamet looks increasingly positioned for a strategic transaction, with its flagship BKM copper project in Indonesia offering a rare combination of timing, jurisdictional fit and valuation disconnect.

The project is shovel ready, aligned with Indonesia’s downstream processing mandates, and capable of producing 10,000 tonnes of LME Grade A copper cathode annually — a strategic prize amid a global copper supply crunch.

Majority backer PT BUMA now controls 44.6% while heavyweight appointments including Grant Samuel as financial adviser and Peter Oliver as project director signal preparations for financing or M&A.

BKM’s conservative NPV multiples significantly exceeds Asiamet’s £30 million market cap, copper price upside is materially improving the economics, and local limestone drilling is further de-risking costs.

The key question is not whether a buyer or financier emerges, but which player moves first — and at what premium — before this undervaluation closes.

Stay tuned.

Alien had a frustrating month. We’re still sitting on solid paper gains year-to-date, but two factors brought us back from a recent high.

First, the next set of assays from West Coast Silver came back, with hole 25WCDD008 identifying further high-grade silver mineralisation zones including:

6 metres at 316g/t Ag from 44 metres; including

1.4 metres at 1,007g/t Ag from 45 metres

21 metres at 50g/t Ag from 20 metres

This is not the bonanza grades of the last RNS, which perhaps disappointed investors - but it’s worth noting that 316g/t is still much higher grade than most of the world’s silver mines.

And with silver racing ahead to $47 - this nuggety exploration may continue to deliver. Phase 2 (approximately 1,000m diamond, 2,000-3,000m air core) is coming, with drilling to start within the next few weeks.

Perhaps the bigger concern was Maiolo’s departure. My perception was that Chris was making steady progress on Hancock and the PGMs - so the question is one of whether him leaving is a setback, or whether possible partners have been lined up, with it up to new Executive Director Belinda Murray to execute.

I’ll be interviewing Belinda shortly, but for reference, she played a key role in overseeing the growth of BGC Contracting, a major Australian mining, civil construction and maintenance services company which employs more than 3,000 people.

Let’s see concrete action soon.

Guardian Metals, like several on this list, is now a defence stock.

We enjoyed another new record high in September, with the company starting its first ever diamond drilling programme targeting multiple brownfield exploration targets at co-flagship Tempiute - 19 drill targets are in play, and because the asset is so close to ALS in Reno, cores will be sent out every week or so and news flow will be strong.

Presumably the truck driver can wait a few minutes and then take it to the national stockpile next door.

We also saw some progress on Pilot North, with CEO Oliver Friesen noting that:

‘The combination of both the high tenor and consistency of the rock chip assay results-particularly in copper, silver, and tungsten-across much of the Project area is very encouraging and, in our view, underscores the potential importance of this developing opportunity for the Company.’

I tend to not comment on rock chips much, but there were some excellent grades in there.

The reason why the stock is moving though is its intention to list in the US properly.

They’ve engaged Davis Polk and Wardwell LLP (big guns, interestingly also in the crypto space, watch how this might play out) to make this happen, and with Stanley Druckenmiller a significant shareholder, appetite will be strong.

Raises have always been conducted fairly, so it’s possible that the stock is simply rising to meet the potential US listing price.

EnergyPathways is due a longer update in the near term, but for the sake of brevity…

We won.

Ed Miliband, UK Secretary of State for Energy Security and Net Zero, has - like the state authority of Shawshank - clearly read my letters and:

‘directed that the major elements of the Company’s flagship MESH project be treated as a development of national significance requiring development consent under the Planning Act 2008.

With the Secretary of State’s decision, the major elements of the MESH project will now follow the priority development authorisation processes under the Planning Act 2008, reserved for projects of national significance in energy and other sectors.’

Of course, you had the initial rocket before the herd moves on - but like ALRT and a few other select stories, the growth potential here for a longer term investor with a reasonable appetite for risk, is incredible.

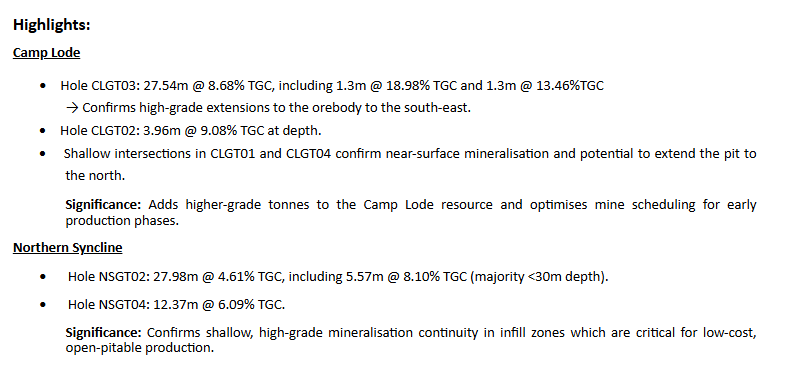

Blencowe I covered in depth a couple of weeks ago, but we were treated to further, excellent assays a few days ago including:

Executive Chairman Cameron Pearce enthused:

‘The results confirm high-grade extensions to both Camp Lode and Northern Syncline, while reinforcing the advantage of shallow, easily mined ore that underpins our low-cost production profile.

All this data will be fed directly into both our JORC Resource upgrade and the Definitive Feasibility Study, which is due for completion in Q4 2025. Increasing ore reserves at higher grades is a critical step and we expect this to not only enhance the mine plan but also translate into a considerable uplift to project economics and NPV…

…These milestones will showcase Orom-Cross as a standout global graphite project, provide the platform to move directly into financing discussions, and ultimately set the stage for a major value re-rating as we continue to de-risk.’

Sounds good to me!

Bezant is going to be a bonanza stock in 2026.

Bird noted this month that the company has:

‘now received full commissions from the Namibian Ministry of Mines to proceed with the development of the Hope and Gorob project…We are also, investigating ways to limit the timeline to production, which involves every aspect of the operation from mining to final concentrate production. We are in the processing of placing firm orders for key items of equipment…

…We are assessing a number of joint venture and third-party involvement in the Hope and Gorob project and will form a conclusion consistent with our finance requirements as and when appropriate.’

Having acquired the NLZM Processing Plant - which has undergone significant test-work and is ‘fit for purpose,’ the company plans to use the cashflow (I think around $50 million a year or more) to:

‘explore the mineralisation between Hope and Gorob and along the remaining 97km of prospective strike length with a view to develop a significant mining resource in excess of 500,000 tonnes of contained copper equivalent.’

There isn’t much more to say at this point. Secure financing in the region of $15 million, and we’re away.

Power Metal is causing me anger issues. This is a company with a uranium JV with ACAM worth up to £16 million, its market cap in cash, Block 8 exploration in Oman, GSA, almost half of FDR and whatever it turfs up - and just invested £3 million into Minestarters, a decentralised finance platform bringing tokenisation to mining exploration.

I can’t talk much about Minestarters due to work elsewhere, but what I will say is that in this space generically, imagine the benefits:

Access to new sources of capital from traditionally digital investors

24/7 liquidity and trading as assets on the blockchain

You can skip an IPO and simply host a private company on the blockchain. Blocks (crypto) would represent shares - when you buy and sell, a hash of the last block is encoded in the new one, so accurate ownership ledger.

You can implement smart contracts into the blockchain to create immutable records of things like royalties

Tokenised structure means borderless access - for example, hard to buy ASX/TSX stocks in the UK, blockchain solves this as worldwide

Potential for secondary markets in future cash flows (for example, if you want to finance a mine build, you can crowd source it and then pay dividends directly)

Trackable ESG compliance

Let’s say you’re an explorer and you want to raise £2 million. Instead of an IPO, you can publish a corporate presentation and then issue 20,000 new blocks each costing £100 on the blockchain.

Anyone can invest whatever they’re comfortable with. Once you hit the target, the blocks are confirmed, everyone gets their blocks (instead of shares), and the company has raised the capital, which represents ownership in the asset.

If you hit the jackpot, management agrees to sell the asset for £20 million.

However, more than 50% of block owners have to also agree for this to happen - so you can’t be undercut and a figure that makes sense to the majority will always be reached, or it never sells.

This democratises the finance, but comes with risks as ever as some may be unrealistic in what’s achievable.

One other positive is no listing/IPO/lawyer fees associated with being on AIM. The negative is zero regulation but there isn’t any enforcement anyway.

This could be an incredibly shrewd investment, but is also very complex.

Year-to-date, Asiamet is up 28%, Alien is up 68%, Guardian is up 292%, EnergyPathways having been added in March is up 17%, Blencowe is up 52%, Bezant is up 164%, and Power Metal is up 8%.

That’s an average return of 90% across the dealmakers at present.

Jubilee & African Pioneer

We’re waiting on Jubilee. Not much else to say here other than to repeat what I noted last month in August:

‘Over a 10 year horizon, the ambition is to exceed 50,000 tonnes per year and $500 million in revenue…

…and the market thinks this is worth $120 million at present.’

It’s well worth a read.

African Pioneer is all Ongombo. Bird noted in recent results that he is:

‘convinced that we can increase the open pit potential, whilst identifying further ore contiguous to the boundaries and infill the area between the central and east shoot. Ongombo has the benefit of mining and exploration permits and represents a viable near production mining potential for a 8,000 tonne of copper year project.’

While the plan is to acquire more assets, there is already 300,000 tonnes of contained copper - if Bezant secures financing, Ongombo will surely follow as both copper assets are in Namibia.

I’ll also note that Zambian Northwestern copper exploration partner FQM, to whom Bird sold what would later become their flagship in the 2000s - has launched a $1.25 billion expansion at Kansanshi.

Zambia has its risks, but so does everywhere else - as FQM has learnt to its cost.

These two have done less well, down 15% and 30% respectively. I’m unconcerned on both as long term investments and am slowly buying more as weakness continues.

Buying low and selling high is generally the correct way to do things.

The Helium Pick

Helix Exploration saw Inez #1 assayed at 1.2% helium with the balance being primarily nitrogen - which is excellent news.

Flow rates were established as commercial, with Absolute Open Flow estimated at 1,157 thousand cubic feet per day (Mcf/d) and a maximum surface pressure of the zone tested at 1,541 psi.

Further perforation in the upper Souris River formation to add to current flow rates is also planned…

But now the focus is squarely on production.

CEO Bo Sears notes that Rudyard is a ‘cornerstone helium project.’

The move upwards is going to come from re-rating to producer valuation from the current explorer valuation, where the market values the company on revenue/profit metrics rather than speculation.

Production is around the corner - perhaps in October - and in the next monthly review, I hope to say that we’re revenue generating.

Of course, this is also going to require an offtake partner.

It’s also worth remembering not only the exploration scale, but the oil and hydrogen signs at Helix’s assets. Anything from this corner will be pure upside as currently it’s valued on the helium only.

I think 40-50p before year-end is not unreasonable to hope for.

We’re up 60% year-to-date.

The Moonshot

As noted previously, I sold my initial stake in Emmerson earlier this year, so am now on a ‘free ride.’

Which is nice.

The stock has fallen slightly and is now up 121% year-to-date.

Some think the fall may be indicative of a settlement being drawn up that avoids a long legal dispute (but only paying pennies on the dollar).

Others argue that with the Formation of Tribunal, arbitrator appointments and negotiations, and the Strength of Claim announcement - there’s a long, bumpy road ahead, regardless of the legal virtues.

Whatever the case, it’s fallen on virtually no volume.

Basically, you either sell now or are in for the long haul (and yes, I know some shareholders have been here and underwater for some time).

I’m here to the end.

Closing Comments

In my last review, I made comments on a few monthly picks:

‘The only other London-listed stock yet to move with Havieron-like tenure I’m aware of is Artemis Resources:

Its Paterson Central project covers some 605 square kilometres and 100% owned. It hosts high priority drill-ready targets within the Havieron ‘NW corridor’ include Apollo, Atlas and Enterprise which remain untested.

That’s a story to consider for those of you with the risk appetite - having recently raised, dilution risks are minimal and other licences at the company are equally prospective…

Artemis is up 24% over the month. Enough said.

‘The first is Defence Holdings. I covered the company this month and interviewed their rock star CTO. I realised mid-interview that these people are of the calibre I usually see only at blue chip companies.

There’s a reason for this.

My second pick is Rockfire.

ACAM’s backing is key, but so is the Molaoi zinc-lead-silver-germanium project, which I expect may be recognised as metal independence critical shortly.’

Rockfire is up 16% from 0.18p to 0.21p - but we were at 0.32p at one point before it fell off.

I suspect there is a seller in the stock. When they’re gone, it will motor up again - especially as the Chair of the JORC committee has signed on alongside ACAM.

This will return to highs before too long.

Defence Holdings is up 550%.

I’ve had worse months.

Looking into October, I suspect ALRT will continue to rise though with ever increasing volatility as some take profits and the monkeys hunt for bananas.

Again, this is the ground floor of what could be the UK’s Palantir. There is absolutely nothing wrong with de-risking as some will be tempted to - but retaining some risk can pay off spectacuarly.

I also noted when commenting on Power Metal that:

‘in the Athabasca in Canada where the POWER/ACAM JV operates, there’s a small equine company out there with some tech that could be genuinely game-changing.

I won’t name it as the stock remains illiquid, but keep your eyes peeled.’

This was Stallion Uranium (STUD), up 40% for the month, and substantially more year-to-date. This is something special and worth keeping an eye on.

Its Haystack Intelligent Targeting makes use of cutting-edge AI tech to refine drill targeting across uranium - and is currently being deployed across its portfolio in the Athabasca.

This could well become a new mining standard.

Looking into next month, Sovereign Metals & Helix Exploration, both of which I already own, may be the winners.

SVML - we’re looking at the resource upgrade, DFS and possibly other bullish news as this game comes to its conclusion…

and Helix when first production demonstrates this is the first helium company to actually deliver on time.

That’s all from me.

Have a great month.

Thanks for sharing Charles! Always a great read.

Great update and review Charles. Its an A+ from me.