Small Cap Mining: September Review

The times, they are a-changin

Good Evening Team.

It’s finally happening. Junior resource is back.

I’ve lost count of the number of stocks going on multi-bagging runs over August - all the more surprising given this is meant to be the ‘quiet’ month.

Investors in Wishbone Gold walked away with 20 bags if they had the stones to buy and hold. For reference, I stayed and remain out of this one - the Breccia pipe is exciting - but assays are where the cookie crumbles.

However, the wider point is that risk appetite is back.

It might have something to do with record gold price (now above $3,500) or silver hitting $40 and rising, or the Sino-US tensions bubbling over.

Aside from the US government starting to take equity positions in critical mining stocks, having finally realised that the free market cannot compete with Chinese market subsidies, the Communist country is going after yet another asset - the Nui Phao tungsten complex in northern Vietnam, in which two Chinese companies wish to take a stake.

I’ve been long TTT (tungsten, tin and titanium) for some time.

They’re only going higher.

GMET, RMR & SVML are my specific picks, though you could do worse than simply going long on these metals.

Interestingly, Geo Exploration & First Development Resources (having recently IPO’d) have both seen decent rises over the past few weeks.

The only other London-listed stock yet to move with Havieron-like tenure I’m aware of is Artemis Resources:

Its Paterson Central project covers some 605 square kilometres and 100% owned. It hosts high priority drill-ready targets within the Havieron ‘NW corridor’ include Apollo, Atlas and Enterprise which remain untested.

That’s a story to consider for those of you with the risk appetite - having recently raised, dilution risks are minimal and other licences at the company are equally prospective.

An article for another time perhaps.

In the US, the insanity continues. As anyone with a legal background would expect, most of Trump’s tariffs have been found to be illegal by a US appeals court. This will now likely head to the Supreme Court where they will again almost certainly be struck down.

Trump (assuming he’s still alive) can then blame the woke judiciary - half of whom he appointed and are about as far from the concept of ‘woke’ as is imaginable - and then move on to the next nonsense.

Just imagine being Apple’s Tim Cook.

You ship over planes full of iPhones to avoid the tariff deadline. Then you agree to move iPhone production from China to India to avoid 140% tariffs.

Then a month later, Trump threatens to impose a 25% tariff on iPhones not made in the US anyway.

Then immediately after you announce a $600 billion investment in the US to support Trump's trade plans, Trump puts a 50% tariff on India for buying Russian oil, which is exactly what China does.

LOL.

In other news, the Fed’s given up on its 2% inflation target:

I hope you own gold.

Regardless though, the bond market is nervous. Nervous of the US deficit crisis, the Japanese carry trade unwinding, and the UK’s spending problem.

If you thought we could shut down the global economy for two years and pay half the population to sit at home and do nothing with printed fiat, all with zero consequences, you were wrong.

The ever-increasing tax and spend across the developed world is the equivalent of paying the pandemic bill. And as increasing tax or reducing spending both seem politically toxic, it’s going to get messy.

In the UK, right now, the top story is channel migrants/asylum seekers.

This is another politically toxic mess but you only need to see what Australia eventually resorted to to know what will happen in the end.

Pushbacks, detention and removal to a third country. Whether this is done by the Conservatives, Labour or Reform is largely irrelevant. The cost and increasing sense of unfairness is close to crisis point.

Australia initially started offshore processing and detention in 2001 under the ‘Pacific Solution’ and then from 2012, where asylum seekers arriving by boat were transferred to offshore detention centres, rather than being processed in Australia.

In 2013, Operation Sovereign Borders began - with boats intercepted either pushed back, or occupants returned to their country of origin (or Indonesia with an agreement in place).

Australia also has UNHCR agreements to resettle refugees in third countries including Nauru and Papua New Guinea - and anyone arriving by boat remains unable to apply for a permanent visa.

Boat arrivals fell from 20,000 in 2012 to almost zero by 2015.

It’s worth noting that it took Australia a lot of hand-wringing before it got tough. I suspect that a similar model is where the UK will eventually go, regardless of ethics.

The underlying problem, of course, is that this singular issue, while important from the viewpoint of border security, is essentially tiny in terms of governing the country.

The Labour government (and being fair, the Tories in opposition) are now running what is the equivalent of a permanent election campaign against Nigel Farage, rather than working on the very real issues plaguing the general population.

There’s a very real sense of incompetence.

Right now, the yield on 30-year gilts stands at 5.6%, higher than it was during the 2008 GFC. This has increased the cost of servicing the interest on our national debt to more than £100 billion a year, close to 10% of the UK’s budget.

And despite the massive tax increases last year (remember, Reeves said very clearly last November ‘I’m not coming back with more borrowing or tax rises…we won’t have to do a budget like this ever again'), borrowing hit £155 billion over the past 12 months - around £5,500 for every household.

Don’t worry though, our saviours are here.

The two you need to keep an eye on are Reeves’ junior, Pensions Minister Torsten Bell, & Starmer’s new Personal Economic Adviser, Minouche Shafik.

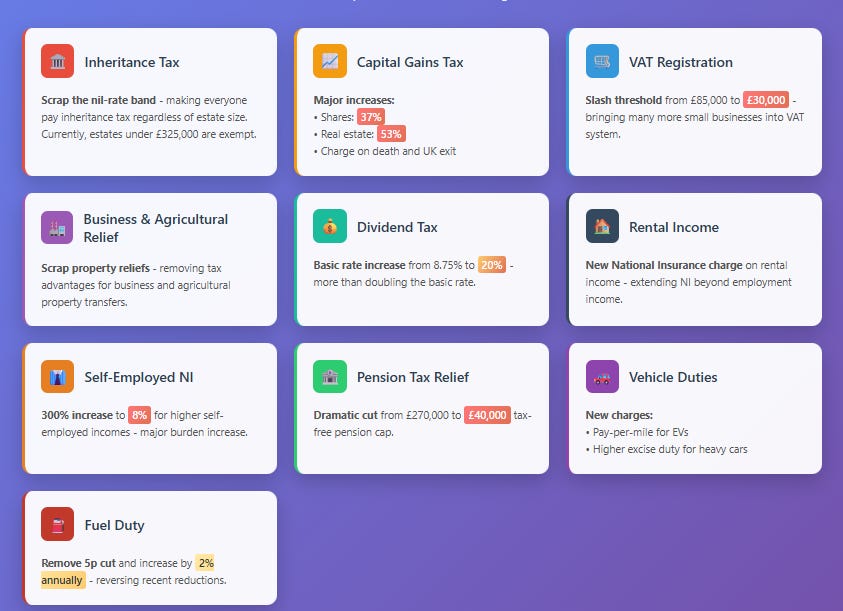

Both were previously senior members of the Resolution Foundation, which recently proposed the following idiotic tax changes:

For context, in 2023, Shafik co-chaired a Resolution Foundation inquiry which called for the abolition of inheritance tax relief on farms and bringing pension pots within a dead person’s estate.

Both measures were enacted by Reeves in her first budget.

This is an individual who believes that:

‘The idea that you are successful because you are smart & hardworking is pernicious & wrong.’

As a reminder, personal life experience is not a substitute for hard data.

Last year, she resigned as President of Columbia University after widespread criticism of the treatment of Jewish students during anti-Israel protests at its New York campus.

This suggests she’s not quite as smart as she thinks she is.

She was also (among other roles) once a deputy governor of the International Monetary Fund.

Ahem.

Anyway, the kite-flying has begun.

National Insurance on landlord rental income, separate reports that the VAT threshold could be moved significantly up or down, new taxes on ‘unearned wealth’ including land taxes and potentially even CGT on primary domestic dwellings…

…and potentially another tax raid on the banks, which saw all the big four FTSE 100 institutions sink lower last week.

We have a new £50 billion ‘black hole‘ to pay and the government hasn’t yet seemed to have learnt the lesson that tax rises will just make it worse.

Sigh.

It’s the same across the developed world.

If you think it’s bad here, consider France. Its debt has hit €3.3trillion, or £2.9trillion and Finance Minister Eric Lombard has just warned they may have to go cap in hand to the International Monetary Fund for a bailout.

Macron is trying to push through the equivalent of £38 billion of tax hikes and spending cuts through the National Assembly - sound familiar?

Anyway, the basic point is that real, hard precious assets will continue to appreciate against collapsing fiat currencies, while critical minerals will become ever more valuable as the Sino-US war for global metals dominance heats up.

Which brings us nicely back around to junior resource.

The Golden Trio

Greatland Resources’ unaudited FY25 results came out with no surprises (thank god).

In AUD:

Revenue from customer contracts of $961.3 million at an average achieved gold price of $4,785 per ounce

Net cash flow from operating activities of $601.1 million

Segment earnings before interest, tax, depreciation and amortisation of $526.7 million

Net profit before tax of $441.9 million reflecting high margin production from Telfer

Net profit after tax of $337.3 million

Cash was $574.7 million at the end of June, with zero debt and full exposure with decent hedging to the current gold/copper pricing.

The real prize would be developing Havieron without debt, which I estimate would require perhaps another 10 months of gold at this gold pricing level.

On this, the assumption remains that gold will continue to rocket should a global recession come down the track. You need to be careful with this assumption - investors and institutions will sell their most liquid assets first.

This fiat crisis is novel and we are in uncharted waters.

On another note, I’d also comment that GGP is quietly acquiring more exploratory tenure. There are implications for nearby explorers with adjacent tenure, but as I’d rather not cause a spike with name drops, those interested can do their own research easily enough.

The big question for September is whether Greatland enjoys ASX 200 inclusion. If it doesn’t quite get in this time around, it will next time - so for a long term investor it matters little.

However, as I have said before, funds usually start accumulating stock around one to two weeks before the effective date of the rebalance.

And the rebalance typically becomes effective after the third Friday of the month, which is 19 September 2025 this quarter.

So if GGP gets in, expect volume to rise significantly between 15-19 September.

Of course, everyone knows this and will try to get a quick profit, so this may all be priced in - but the uncertainty over inclusion means it may not be.

But I would assume this could be a very good month. Putting aside the recent mis-step, consider just how much money is being made at Telfer - and it’s not even the real prize.

One other thing - Macquarie & Arrowstreet - that’s not a good look and this may well come back to bite you.

Sovereign Metals finalised its mining fleet design for Kasiya this month, and also delivered exceptional test pit rehabilitation for its first year.

This was always going to be a slow quarter for Sovereign as investors wait for the DFS to land in Q4 (though I’ve yet to see any DFS deliver exactly on time).

As we know, when the DFS lands, investor and technical committee partner Rio Tinto has 180 days to decide whether to take over operatorship of Kasiya - which would basically guarantee a buyout.

However, there is a spanner in the works.

Rio Tinto’s new CEO Simon Trott has a new strategy - dividing the major into three core business units to focus on its most profitable assets: iron ore, aluminium & lithium, and copper.

The titanium among other assets will be passed over to CCO Bold Baatar for review, with further updates to come.

Reuters recently reported that the FTSE 100 company was considering selling the titanium unit because of weak prices and low returns - with its division head Sinead Kaufman leaving Rio at the end of October after almost 30 years of service.

I will note three things here:

(a) Rio has previously tried to sell the titanium on several occasions but has never been able to secure a reasonable price.

(b) Kasiya’s extreme low cost and high value (largest rutile and second largest graphite deposit in the world - and cost competitive with China) might itself make the division worth saving. If not sold off, it becomes a divisional priority.

(c) SVML has the operational expertise to build the mine themselves - which is the preferred route of supportive investor and all-around legend Rick Rule, and almost certainly has a long line of prospective suitors lined around the block.

If there’s a dip, I’m buying it.

Amaroq I covered in depth this month - but think it’s worth repeating that the reduced gold production guidance this year is not an operational problem but a conscious choice to increase long-term production at its flagship processing plant at Nalunaq.

The share price performance this year has in a sense been disappointing (down circa 40% compared to GGP’s 100%+ rise, though slightly up still over the past year) but it also represents an exceptional opportunity.

I note the comments on its head of exploration selling down his shareholding - but this was due to an immediate need for capital to cover an inheritance tax bill after a bereavement.

Could this have been managed better optically? Yes, and there’s no getting away from that.

However, I’d argue that James has given nothing less than 100% to the company for years and deserves some sympathy. We have all had to sell assets when we didn’t want to.

A particularly frustrating and damaging aspect of IHT is that the liability is generally immediate - perhaps the government could do something useful and look into this?

But anyway, as a fundamental investor - and especially given the recent raise at a significant premium to today’s share price, which has enabled the faster gold optimisation - Amaroq is in a much better position that it was at the start of 2025.

And as the CEO told Bloomberg a couple of months ago, the US remains keen to get involved.

We all saw what happened to MP Materials.

In ytd terms, GGP is up 110%, SVML down 5% and AMRQ down 40%. So we’re still up 22%, but I would bet this return will be higher by year end.

The Explorers

Rome Resources popped into the 0.4s on Friday before settling back down with huge trades in the background after months of low volume.

During August, drill hole MADD030A returned 18 metres of mineralisation with a maximum grade of 2.4% tin, while MADD032 encountered a copper intercept measuring 13 metres with a maximum grade of 13% copper plus 9 metres of tin within a higher-grade, 13 metres wide zinc zone (though all measured by XRF).

Interestingly, these results indicate the presence of a strike-slip fault creating a potential duplication of the principal mineralisation zone to the east of the main zone drilled to date.

The significant copper intercepts are expected to add to the growing polymetallic resource at Mont Agoma in connection with the ongoing work associated with the Company's maiden mineral resource estimate - and assays for a six further drill hole samples are expected to be reported shortly - and added into the MRE.

This MRE is coming, and could be much better than expected.

With IRH recently taking a large stake in Alphamin, you might expect them to consider funding Rome’s next tranche of exploration given the same exploratory/team Chairman that discovered Alphamin’s Bisie are currently at Rome - and Alphamin seems not great at its own exploration.

Watch this space.

Arc Minerals saw a significant legal update over August - noting that:

‘a judge at the Zambian High Court in Lusaka has concluded that the Consent Judgment obtained in March 2022 closed the court record and that the Court has no jurisdiction to entertain further applications.’

This lends ‘strong support to the Company's defenses in the various spurious and vexatious claims brought by a former director.’

For historical context, Zamex has filed a writ of fieri facias ex parte (attempting to seize up to $650,000 in alleged damages without Arc being present in court).

The claim was based on an alleged default of the March 2022 Settlement Agreement, which had already been formalised into a Consent Judgment, giving it full legal force.

Arc is taking practical steps to enforce the practical effect of the High Court judge's conclusion - and it’s worth noting that its lawyers believe that ‘impropriety is evident in both the documentation submitted in support of the Writ, as well as the process followed.’

A synonym of impropriety is fraud.

I’m confident that the Writ will be declared invalid, and have it on good authority that Anglo American’s lawyers are synchronised with Arc’s.

I also have it from an excellent source unrelated to Arc & Anglo that another FTSE 100 major (not Anglo American) which was seriously considering an investment in Zambia has cited this case as a reason why they are hesitant to invest. If the country wants western investment to continue, this sort of nonsense needs to stop.

The JV with Anglo remains in good standing and we await news.

I would note though that any RNS on drilling or legal issues resolved will see a sharp recovery.

The dealmakers

Asiamet announced Peter Oliver as a non-Board Project Director for the BKM Stage 1 Copper Project this month - he’s worked in senior roles with BHP, Vena Energy, UPC Renewables, SMEC International, and PT Bukit Makmur, and prior to joining was Operations Manager for BUMA's infrastructure division.

The company has also started limestone resource drilling at the Rinjen prospect, approximately 12km north of BKM.

These things make the project even more attractive.

As before, with Grant Samuel on board, an asset/company sale is a case of when, not if. Ideally by year-end.

Alien Metals I covered recently, but I think in the excitement of the world class silver grades at Elizabeth Hill, investors are missing that Maiolo remains on the case to secure a JV for the Hancock iron ore DSO project.

Macro Metals recently released an ASX cleansing notice that looks very interesting:

Though we can’t know for certain whether this relates to Hancock, we do know that multiple parties are being spoken to.

That JV lands, and we’re going to keep going. I’d also note that the PGMs at Munni Munni represent a third potential Joint Venture.

Watch this space.

Guardian Metals saw parent Power Metal sell its remaining c25 million shares (14.75%) to an investment fund managed by Duquesne Family Office LLC.

Duquense is controlled by Stanley Drunkenmiller.

Stanley was US Treasury Secretary Scott Bessent's boss for many, many years.

Short of Buffett, you could not ask for a better name.

When the UK had a Bank Holiday, the US OTC was open and we ran to a new record high as US demand for shares was met with empty broker hands across the pond, creating an equity liquidity squeeze.

GMET also become a member of the Defense Industrial Base Consortium (DIBC) and the Cornerstone Program in August after being awarded its initial grant funding for Pilot Mountain.

In any other month, this would be incredible news. Both have a primary directive to maintain secure critical mineral supply chains and extraction.

With China’s move in Thailand, a direct US equity stake in the company could well be in the works.

For context, a new Department of Defense (DoD) open contract for tungsten ores and concentrates just opened up, and one of the three proposed locations is just down the road from Pilot Mountain, as recently announced:

'1,715 metric tons of tungsten ores and concentrates for addition into the National Defense Stockpile'

Now consider the PM DoD grant announcement: 'The United States has not mined tungsten in nearly a decade. A domestic source of this essential metal will add much needed resiliency to both commercial and defense supply chains.'

For reference, the National Defense Stockpile was established under the Strategic and Critical Materials Stock Piling Act 1939 and mandates that the US hold reserves of strategic raw materials that are not refined.

This is because ores and concentrates can be stored longer without degradation, whereas refined metals (especially powders) can be more reactive or prone to degradation over time.

Also, unrefined forms preserves versatility as production can be tailored to current needs dependent on which forms get withdrawn from external supply chain.

And at Tempiute, we have truck ready ore stockpiles.

The DoD gives GMET a grant and then very soon after publicly asks for ore…

EnergyPathways had a poor month - with the stock now back to where it was a year ago before the excitement started.

Key quote:

‘The NSTA has informed the Company that it considers it not appropriate to award a Gas Storage Licence based on EnergyPathways' application submitted on 16 August 2024 due to, amongst other things, changed circumstances.’

The share price responded as might be expected, but it’s only half-time.

EPP has submitted a section 35 planning request for immediate approval to DESNZ and the Secretary of State, and is also considering ‘resubmitting the application to the NSTA on a different basis.’

It’s hard to know what these changed circumstances are, though it is worth noting that an S35 can be approved rapidly.

It’s likely that we have no further information on why the licence was denied because the company is furiously working behind the scenes on sensitive work designed to get this decision changed.

And it’s certainly possible that the delay between application and denial is because the NSTA feels unclear on whether they *should* be the ones to approve it given rapidly changing government priorities.

In my own correspondence with various agencies, I did get a sense of classic public sectorism. If this is the case, it’s not a licence denial but a passing of the buck.

One thing to note is that getting a Section 35 approved is not that unlikely given the investment case (and multiple named Tier 1 partners) - and the process from application to judgment usually lasts just 28 days.

As we had the rejection RNS on 14 August, we should have a response by Friday 11 September - and an RNS the Monday after.

As the licence has not been approved, it’ll either be good news or the status quo.

Blencowe Resources signed a non-binding offtake agreement for its natural fine flake concentrate from Orom-Cross with Perpetuus Advanced Materials earlier this month.

This offtaker was going to be acquired by China back in 2022, but the UK government ordered a national security review into the deal, and it was dropped immediately.

This might tell you something about who wants this graphite.

BRES has now completed all major infrastructure workstreams within the DFS, with Executive Chairman Cameron Pearce noting that:

‘Our DFS is progressing well, and we look forward to showcasing something special. We anticipate being able to update the market on a completion date in the near future…With DFS, assays, JORC and further offtake developments all ahead, we believe Orom-Cross is on the cusp of a major value inflection.’

Eyes on.

Bezant acquired a processing plant for Hope & Gorob - to be used on the copper and gold once it has already been dry ore sorted.

This is the longest lead item in the mine plan and accelerates production by at least 2 years, whilst eliminating a significant capital cost.

The company notes that ‘Discussions are advancing on multiple options available for the financing package to develop the Hope and Gorob Project. The discussions range between debt or equity or a combination thereof, prepaid finance is also being considered as an addition or substitute within the package.’

Executive Chairman Colin Bird enthuses that ‘The agreement to acquire the NLZM plant is a pivotal move in developing our Hope and Gorob resource…We are now advancing all underlying key contracts to signing and intend to commence production as soon as physically and practicably possible.’

I have covered the potential return here in depth at length, several times - once financing is agreed, we will shortly go into production and many years of Bird’s work will pay off.

Power Metal now has maybe £20 million in pure cash after selling its remaining stake in GMET - alongside shareholdings in recent IPO First Development Resources, First Class Metals, exposure to a circa £16 million upside JV with ACAM to drill in the Athabasca, plans for Power Arabia…

…and other smaller projects.

The stock is finally responding to the overwhelming fundamental investment case, but I’m prepared to wait as long as it takes.

I would note that Sean very clearly has a plan for this capital. When revealed, it may re-rate sharply.

On uranium, it’s worth noting that Sweden now plans to lift its ban on uranium mining on 1 January 2026 - it’s worth hunting for explorers in the country before anyone else notices.

And in the Athabasca in Canada where the POWER/ACAM JV operates, there’s a small equine company out there with some tech that could be genuinely game-changing.

I won’t name it as the stock remains illiquid, but keep your eyes peeled.

Year-to-date, ARS +22%, UFO +200%, GMET +179%, BRES +27%, BZT +169%, POW +20%.

Not too shabby.

EPP was added in March, down -55%.

Excluding EPP as a binary risk play, we’re up 103% across the dealmakers so far - and circa 80% when EPP is included.

I think though that Asiamet’s asset sale, Blencowe’s DFS & Power’s plans could push this overall return higher.

And EPP could yet deliver.

Jubilee & African Pioneer

Jubilee saw 97.38% of voters vote for its proposed sale of the South African Chrome and PGM Operations on 28 August.

I’ve written at length on this deal recently, so have little else to say other than that it remains sorely undervalued, and perhaps that online discontent does not reflect the near unanimous result.

But in the end analysis, this is Leon’s decision, and the overall judgement on his tenure will be based on whether Zambia becomes a success.

My bet is it will be.

African Pioneer also holds a similar licence to Bezant - Ongombo - but has not enjoyed a similar rise.

I think it will.

AFP also has a copper exploration JV with FQM, which just decided not to sell off its stakes in major copper producing mines Kansanshi and Sentinel.

Who was key to discovering these?

Hang on.

Anyway, HH has officiated the commissioning of the S3 Expansion at Kansanshi - and with FQM doubling down on Zambia, AFP’s JV with the major has become all the more valuable.

With a market cap under £3 million, it’s not hard to accumulate a meaningful % position if all goes to plan - we know someone who has already.

The Helium Pick

Helix Exploration almost shot into the 30s over August before coming back a little - though remains up 40% year-to-date.

There’s not much to say here.

Inez is being flow-tested.

Production is planned for later this year.

$4 million in revenue per well, get five wells producing to start with, use the revenue to keep expanding Rudyard to 20 wells - and also re-enter Ingomar.

No concerns, it’s just a mildly boring phase as they commission the production facility. As ever, I expect it will take slightly longer than expected.

I’ve never seen production start on time (there’s always some obscure part that needs replacing/optimising etc) but would be happy to see it.

Upon production, it gets very exciting, very quickly.

The Moonshot

Emmerson remains around that 2p mark and up circa 160% year-to-date.

It’s interesting to see shareholder efforts to garner UK ambassadorial support, but I suspect our government has enough on its plate.

Morocco appointed Professor Zachary Douglas as arbitrator this month - the bad news is that his track record is generally in favour of the state, including dissenting opinion where necessary.

To be honest though, I’m not sure what else you might expect. States will always appoint arbitrators who might favour their viewpoint.

The tribunal’s president is where it gets dicey.

But if the ‘Boys’ are backing Emmerson, I’ll still take that gamble any day of the week (having taken out my initial stake as noted previously).

Final comments

Last month, I told you I had no monthly pick and was going to enjoy August.

While the workload did not go quite according to plan, I’m glad for the additional rest.

This month, I have two picks.

The first is Defence Holdings. I covered the company this month and interviewed their rock star CTO. I realised mid-interview that these people are of the calibre I usually see only at blue chip companies.

There’s a reason for this.

My second pick is Rockfire.

ACAM’s backing is key, but so is the Molaoi zinc-lead-silver-germanium project, which I expect may be recognised as metal independence critical shortly.

Have a great month - children are back to school soon and my sanity remains mostly intact.

Stay strong junior resource investors.

The good days are back.