*all dollar amounts in USD unless otherwise stated*

Good Afternoon Team.

While Maiolo continues work on our Hancock JV (and possibly a Munni Munni PGM deal), our Elizabeth Hill partner has just delivered some impressive news.

Before we consider the grades, a refresher on Elizabeth:

Historic producer – One of Australia’s most impressive historical silver mines, located in the Pilbara, WA.

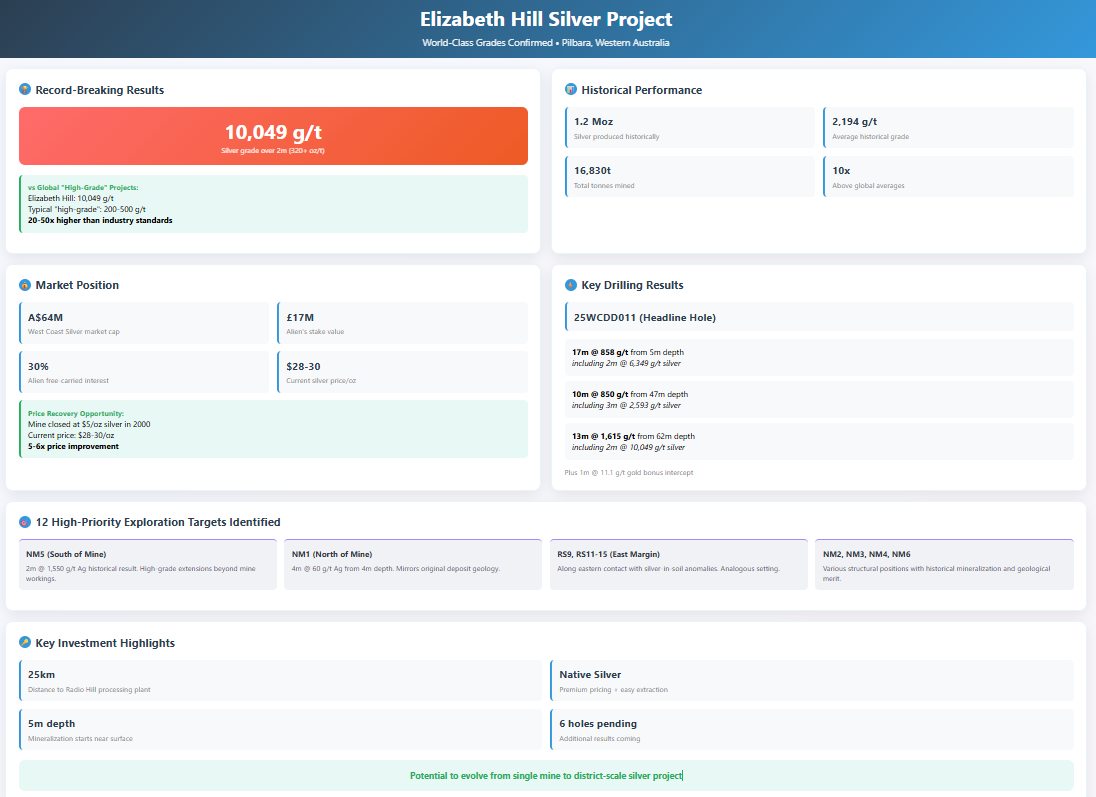

Exceptional grades – Produced 1.2 Moz silver from 16,830 tonnes at an average grade of 2,194 g/t (70.5 oz/t), nearly 10x global averages.

Efficient operations – High grades allowed simple gravity separation and low cost processing, driving strong margins.

Premature closure – Shut in 2000 due to silver prices (~$5/oz) and JV disputes, not resource depletion.

Untapped potential – Significant mineralisation remains with limited modern drilling and geophysics.

Strategic location – Tier 1 jurisdiction with nearby Radio Hill facility (~25 km), offering existing processing infrastructure and reduced capex needs.

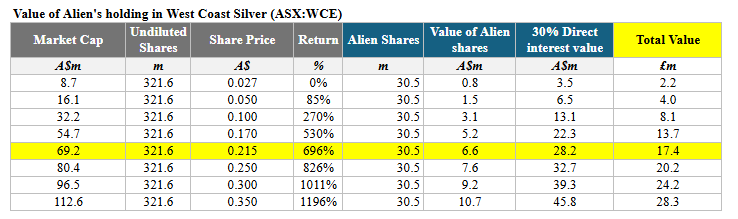

The project is now operated by West Coast Silver (ASX: WCE), with Alien holding a 30% free-carried interest through to a decision to mine, and at the point of the JV, a 10% shareholding (though this is subject to standard dilution).

This structure means Alien shareholders maintain significant exposure to any success at Elizabeth Hill without contributing to exploration costs:

West Coast has now risen to an A$64 million market capitalisation, so Alien’s value in the assets is now worth circa £17 million.

However, even after the rise, the market cap only covers the WCE value - and assigns zero enterprise value to Hancock.

So we’re only just getting started.

World Class Grades Confirmed

Put simply:

West Coast’s maiden diamond drilling program has delivered results that stand among the highest grade silver intercepts reported globally in recent years.

The standout drill hole, 25WCDD011, returned multiple exceptional intercepts that confirm the continuation of the deposit's grade profile:

The headline result of 2m @ 10,049 g/t silver from just 63 metres depth represents one of the highest-grade silver intercepts reported by any publicly listed company in 2025.

To provide global context, most silver projects considered ‘high-grade’ typically report intercepts in the range of 200-500 g/t silver.

Results exceeding 1,000 g/t are rare, while anything approaching 10,000 g/t is exceptionally uncommon.

There’s a ‘B’ word here that many like to use, but it feels a little redundant.

25WCDD011 delivered:

17m @ 858 g/t silver from 5m depth, including 2m @ 6,349 g/t silver

10m @ 850 g/t silver from 47m depth, including 3m @ 2,593 g/t silver

13m @ 1,615 g/t silver from 62m depth, including the 2m @ 10,049 g/t silver zone

These results demonstrate not just exceptional peak grades but also substantial widths of high-grade mineralisation.

The fact that significant mineralisation begins at just 5 metres and continues through multiple zones to at least 75 metres suggests a solid, near surface deposit ideal for low-cost mining operations - such as low strip ratio open pit mining or simple underground access.

But it’s not just the grade.

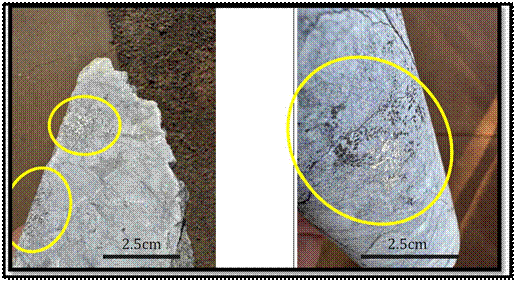

Native silver has been observed in the drill core.

Native silver - found in nuggets like the Karratha Queen (from the previously operating EH mine) comes with a substantial price premium, and because it is in its elemental form, is incredibly easy to extract.

West Coast is also investigating the viability of simple gravity separation to recover the free silver (a processing approach that mirrors the historical operations).

And the project is just 25km from the Radio Hill processing plant (owned by a sister company - incestuous deals can be a good thing here).

Ergo, you’re looking at low capex through Radio Hill, low opex due to the native/exceptional grade silver, and premium pricing.

The financials for any potential mine will look very good.

Better yet, the hole also intersected significant gold mineralisation, including 1m @ 11.1 g/t gold from 51m. While gold is not the primary target, it could provide valuable byproduct credits to any future mining operation.

When compared to other silver projects globally, Elizabeth Hill's grades are genuinely exceptional.

Major silver producers like Hecla Mining's Lucky Friday mine in Idaho typically operate at grades around 400-500 g/t silver, while Coeur Mining's Palmarejo mine in Mexico averages approximately 200-300 g/t silver.

Even renowned high grade silver deposits like those in the Potosí district of Bolivia, famous for centuries of silver production, rarely achieve the consistent ultra-high grades being demonstrated at Elizabeth Hill.

The recent drilling results validate the historical production data and suggest that the grade characteristics of Elizabeth Hill remain intact in unexplored areas around the historic mine.

Drill hole 25WCDD012 also returned high-grade, low-depth silver intercepts, including 6m @ 317 g/t silver from 10m depth (including 1m @ 1,455 g/t silver) and 14m @ 162 g/t silver from 18m depth.

Importantly, assay results for a further six holes from the inaugural 12-hole (1,183m) diamond program remain outstanding and will come in over the coming weeks.

New Exploration Targets at Elizabeth Hill

Just before the drilling results, West Coast reported back initial findings from its comprehensive targeting study, led by independent consultants ERM (formerly CSA Global):

It defined 12 high-priority near mine targets for extensions and repetitions of the EH silver mineralisation.

The study integrated drill holes, geochemistry, rock chips, trench data, and reprocessed geophysics (mag, radiometrics & gravity).

Findings confirm that the intersection of the Munni Munni Fault with the granite–ultramafic contact controls the high-grade silver mineralisation (the same setting as the historic Elizabeth Hill Mine).

New targets were ranked against five factors:

Proximity to key structural features (north-trending faults, flexures).

Proximity to granite/ultramafic contacts.

Coherent silver-in-soil anomalies with multi-element support (Copper & Zinc).

Evidence of gossans or float samples with elevated silver.

Underexplored zones due to poor historical drilling or transported cover.

Key Near-Mine Targets

NM5 (South of Mine) – Along Munni Munni Fault at granite/ultramafic contact.

Historical highlights include:

1m @ 250 g/t Ag (AG43, 118m).

2m @ 1,550 g/t Ag (AMEHRC012, 108m).

Indicates high-grade extensions beyond mine workings.

NM1 (North of Mine) – 100m north along the same fault.

Historical highlights include:

4m @ 60 g/t Ag from 4m depth (granite host).

Supported by high grade float and rock chip results.

Geological setting mirrors original deposit.

RS9, RS11–15 (East Margin) – Along eastern Munni Munni ultramafic contact, coincident with silver-in-soil anomalies and fault structures.

Analogous to Elizabeth Hill structural/host setting.

NM3 (West of Mine) – 2m @ 74 g/t Ag from 48m (granite host).

NM4 (Within Mine) – Mineralisation observed at granite–ultramafic lower contact, suggesting deeper extensions.

NM2 & NM6 – NM2 linked to historical gossan, while NM6 is located at a structural dilatational jog, a setting often associated with strong mineralisation.

Overall, the study identified regional anomalies both north and south of the historic Elizabeth Hill mine, aligned with structures parallel to the Munni Munni Fault.

These findings suggest that Elizabeth Hill may form part of a much larger mineralised system. If the company is right, then we could on to a much bigger winner than previously thought.

The good news is that we now have eight new defined exploration targets, with further results pending from ongoing geochemistry programs.

The next phase of work will include trenching, aircore and RC drilling, and additional geophysics. And as newly completed geochemistry results are integrated with historical datasets, the target inventory is expected to expand further.

Elizabeth Hill now has the potential to evolve from a single historic mine into a district scale silver project.

With silver prices currently trading at $39 per ounce (it hit $40), compared to just $5 when the mine closed in 2000 - alongside low opex, low capex and premium native pricing - the economic case for renewed development is now compelling.

As reminder, there are very few pure-play silver explorers on the ASX.

If silver squeezes, this will keep going.

And that iron ore JV could land any day.

Good update Charles. This makes me think, not only should I increase my shareholding in Alien but also invest directly in West Coast Silver on the ASX through my broker.