Blencowe Resources is almost there

Why Orom-Cross Is About to Get Gobbled Up

Good Afternoon Team.

An African graphite minnow has built the an obvious takeover target in the critical minerals space.

Let’s consider the set up.

When Management Basically Tells You They're For Sale

Let me paint you a picture.

You're running a small African mining company with a market cap of less than £20 million (but still far higher than when I first highlighted this).

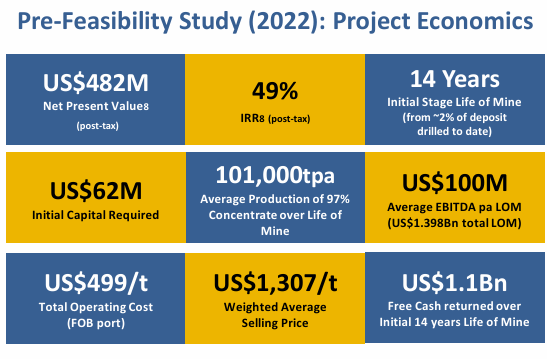

And your flagship project has an NPV of nearly half a billion dollars.

Which is almost certainly going to increase closer to a billion dollars in a few short weeks.

Welcome to Blencowe Resources, where every strategic decision in 2025 has been a masterclass in ‘how to prepare your company for acquisition without actually saying you're for sale.’

It's been so obvious that I'm surprised they haven't just put up a giant "WILL SELL FOR REASONABLE OFFER" sign outside their London offices.

The WaterBorne Capital Smoking Gun (Or: Why You Don't Hire Wedding Planners for a Casual Date)

This month, Blencowe announced they'd appointed WaterBorne Capital as their project finance advisor. Now, on the surface, this sounds perfectly reasonable. Companies need financing, advisors help with financing, everyone's happy.

Except WaterBorne Capital isn't your garden-variety corporate finance boutique. These are the guys who've structured deals for Peak Rare Earths, Two Rivers Platinum, and African Rainbow Minerals. They don't do small-scale mine financing for companies hoping to scrape together a few million quid.

They do major institutional transactions for companies that are either very big or about to become somebody else's problem.

It's like hiring Gordon Ramsay to make you a sandwich. Sure, he could do it, but there's probably a bigger plan in motion.

Brett Levick, WaterBorne's Managing Director, didn't exactly hide the game in his comments about Orom-Cross offering ‘a uniquely attractive profile for debt providers.’

This isn't the language you use when you're trying to convince retail investors to buy more shares. This is the language you use when you're preparing a pitch book for institutional buyers who think in terms of tens of millions - or more.

The mandate specifically mentions ‘sophisticated financial models,’ ‘dynamic cashflow forecasting,’ and ‘carefully structured debt and equity packages that meet international credit standards.’

In other words, they're building the kind of comprehensive financial package that serious acquirers demand before writing big cheques.

The DFS Timing

Here's where things get really interesting. Blencowe has structured their Definitive Feasibility Study for completion in Q4 2025, and they've been absolutely methodical about getting there.

And in interviews with management, early Q4 (next month, has been strongly indicated).

Major drilling program?

Done – 6,750 meters, the biggest in the company’s history.

Infrastructure assessment? Complete – power, roads, water, communications all sorted.

Geotechnical work? Finished – they know exactly how to dig the holes and where to put the waste.

Resource upgrade? Pending – but all the drilling suggests it's going to be substantially larger than the current 24.5 million tonnes at 6.0% TGC.

This isn't the behaviour of a company that's rushing to production. It’s systematically eliminating every possible objection a buyer might have.

It's like someone spent two years detailing their car, fixing every minor issue, and getting a comprehensive mechanical inspection before casually mentioning they might be open to offers.

The timing is also suspiciously perfect. Get a bit of cash in the bank from a placing. Complete the DFS in Q4 2025, spend Q1 2026 ‘evaluating options,’ and then announce a strategic transaction in Q2 2026.

The Geological Story

Let's talk about what Blencowe has actually found in the ground, because this is where things get impressive.

The current JORC resource of 24.5 million tonnes at 6.0% graphite is based on drilling just 2% of their license area. They've barely scratched the surface (no pun intended), and they've already got enough graphite to support a multi-decade mining operation.

The financials are here for the PFS - but remember, these are going to be substantially upgraded as soon as next month:

And here's the kicker: every single one of their recent deep holes has ended in mineralisation. All six deep holes at Beehive terminated in graphite at over 100 meters depth.

The Northern Syncline results are similar.

It’s confirmation that they're sitting on something potentially massive.

Independent geological consultants at Minrom have suggested Orom-Cross could host over two billion tonnes of graphite. With a B.

At current market prices, that's a geological province.

For any potential acquirer, this represents the holy grail of mining assets: a resource so large that you don't have to worry about running out of ore for the next century, with exploration upside that could justify multiple expansions.

The Infrastructure Side

Most African mining projects face the classic infrastructure challenge: great geology, but terrible logistics and massive capital requirements just to get the basics in place.

Orom-Cross has managed to avoid this entirely (honestly with a fair bit of luck, though most successful enterprises require this).

They've got two separate power substations providing access to Uganda's hydroelectric grid. The UK government is paying to upgrade the main road that passes right by their project. Water, communications and basic infrastructure are all available on-site.

This matters enormously from an acquisition perspective.

Low infrastructure capex means higher returns on invested capital. Reliable power means predictable operating costs. Good road access means simplified logistics and lower transport costs.

Put it all together, and you've got a project that can generate cash flow much faster and more predictably than most African mining operations.

For strategic buyers, this translates directly into NPV. Every million dollars saved on infrastructure is a million dollars that goes straight to the bottom line.

When you're evaluating acquisition targets, these advantages compound quickly.

The Government Backing Trifecta: Everybody Wants to Be Your Friend

The level of government support Blencowe has assembled is exceptional. It's like they accidentally became the poster child for critical minerals co-operation across three continents.

Three continents who tend to compete with each other.

The Americans have put up $5 million in grant funding through the DFC, with first right of refusal on full project financing.

This is the US government making a strategic bet on supply chain security in a post-China world. The fact that they're backing Orom-Cross specifically tells you everything you need to know about how Washington views this project's strategic importance.

The Europeans have made Orom-Cross the exclusive graphite supplier to their flagship SAFELOOP battery initiative, part of the €100 billion Horizon energy transition program.

European Union bureaucrats don't hand out exclusive supplier agreements to random African mining companies. They do it when they think you're strategically critical to their energy security.

The British are literally building roads for them. The UK government is sponsoring infrastructure upgrades that will provide direct access to the project site. You also don't get government-funded infrastructure unless someone in Whitehall thinks you're worth supporting long term.

Even Uganda is rolling out the red carpet, providing 21-year mining licenses and all necessary permits. The African Finance Corporation has signed a Letter of Intent expressing interest in debt and equity participation.

For any potential acquirer, this government backing provides something you simply cannot replicate: regulatory certainty, financing optionality and political protection across multiple jurisdictions.

The Commercial Choreography: Building Value Across Three Continents

While Blencowe has been systematically de-risking the technical side, they've also been building a commercial framework.

They've got Jilin lined up to take 15,000 tonnes per annum of large flake graphite, covering 66% of their initial production. That's the Asian market sorted, with premium pricing for high-quality material.

They've signed with Perpetuus Advanced Materials for 19,000 tonnes of fine flake concentrate over five years, tapping into western markets that pay over $1,200 per tonne compared to lower Asian pricing.

That's geographic diversification with margin enhancement - and for perspective, China was originally going to acquire this super-advanced off-taker before the takeover was blocked by the UK government on national security grounds.

They've established a 50-50 joint venture with Triessence for a graphite beneficiation facility that will produce 99.95% purified graphite for lithium-ion batteries, with life-of-mine offtake guaranteed.

That's vertical integration with value-add processing.

As noted above, they've secured exclusive supplier status to the EU's SAFELOOP initiative, positioning themselves as strategically critical to European battery supply chains.

Any acquirer gets immediate access to diversified markets, established customer relationships, and premium pricing across multiple product categories.

It's the kind of commercial framework that takes years to build and would be nearly impossible for a new entrant to replicate.

The Market Capitalisation

Let's talk about the elephant in the room: the valuation. Blencowe trades at a circa £19 million market capitalisation against a post-tax NPV of $482 million (soon to be closer to $1 billion in my view).

Even accounting for the usual skepticism around junior miner NPV calculations, this represents a valuation disconnect which is almost offensive to mathematics.

At £9 million for 24.5 million tonnes of resource, you're paying roughly 78p per tonne of graphite in the ground. Established graphite projects trade at £15-25 per tonne in-situ. Even if you assume Orom-Cross deserves a discount for being undeveloped, and for its jurisdiction, you'd expect something in the £5-10 per tonne range, implying a minimum fair value of £120 million.

The recent £1.12 million fundraise only reinforces the point. Management raised just enough money to complete the DFS and cover working capital for the foreseeable, but nowhere near enough to fund actual development.

This isn't the behaviour of a company preparing for independent development.

The fact that management exercised options at 6p – a premium to the 4.75p placing price – while raising minimal capital suggests they expect significant value realisation in the near term.

You don't exercise premium-priced options unless you're confident the share price is heading substantially higher, and you don't raise minimal capital unless you expect someone else to fund the next phase.

The Buyer Beauty Pageant: Who Gets the Prize?

So who's going to buy this thing? The beauty of Orom-Cross is that it ticks boxes for multiple categories of strategic acquirers.

Battery manufacturers like CATL, BYD, or even Tesla could view this as vertical integration insurance.

Securing captive graphite supply eliminates a major supply chain risk and provides cost certainty for battery production. Given the geopolitical tensions (and even bans) surrounding Chinese graphite exports, having a politically friendly alternative becomes strategically valuable.

Mining majors like BHP are under pressure to add critical minerals exposure to their portfolios.

Orom-Cross offers the scale and quality metrics that fit their investment criteria, plus the infrastructure advantages that minimise execution risk.

For companies that think in terms of multi-decade assets, the exploration upside is particularly compelling.

Chinese state-owned enterprises remain interested in African resource exposure, and the existing offtake relationships with Jilin provide a natural entry point.

Despite political tensions, Chinese companies still need graphite, and a producing asset in Uganda with established infrastructure offers attractive risk-adjusted returns.

Government-backed entities and sovereign wealth funds looking for strategic resource exposure would find the government backing across multiple jurisdictions particularly attractive. When both the US DFC and EU Horizon programs are backing the same project, it sends a strong signal about strategic importance.

Private equity infrastructure funds seeking stable cash flow generation in critical minerals would also be attracted to the combination of long term offtake agreements, low cost production profile and government support.

It's the kind of boring, predictable cash generation that infrastructure investors like to play with.

Why Everything Points to 2026

The beauty of the Blencowe setup is how all the catalysts align for a transaction window in the first half of 2026.

The DFS completes in Q4 2025, providing maximum technical certainty for buyers while maintaining seller optionality.

This timing coincides with peak market focus on supply chain security, including continued US support under the Trump administration and EU critical minerals strategy implementation.

The infrastructure convergence is equally compelling. Road upgrades will be substantially complete, power connections are already in place and port access logistics are fully mapped out.

Any acquirer can move quickly from transaction completion to production start-up.

And best of all? Market conditions also favour near-term action.

Critical minerals are experiencing sustained attention from institutional investors, China+1 strategies are driving premium valuations for alternative supply sources, and the battery market growth story continues to support structural graphite demand.

The Bottom Line

Every piece of evidence suggests Blencowe Resources has spent 2025 methodically preparing Orom-Cross for a strategic transaction.

From the appointment of specialized advisors to the systematic completion of technical workstreams, to the establishment of diversified offtake agreements and the securing of government backing across three continents, this reads like a textbook example of how to maximize strategic value before inviting offers.

For investors willing to bet that management knows what they're doing – and the evidence strongly suggests they do – Blencowe represents a compelling asymmetric risk opportunity.

The downside appears limited given the asset quality and government backing, while the upside scenarios suggest potential returns of as much as 5-10x current levels depending on transaction structure and buyer competition.

Watch this space.

w

Another brilliant and timely piece Charles!