This Market Weakness is NOT Unexpected

It's all Japan.

Good Afternoon Team.

Six months ago, I wrote what was my last warning on bonds for a while.

I laid out, in plain English, exactly what was coming - Japan’s loss of yield curve control, the unwinding of the global carry trade and the inevitable repricing of sovereign debt risk.

I told you the medicine wasn’t going to taste good.

And here we are.

The Thesis Is Playing Out

Let me be blunt: analysts and commentators expressing shock at current market weakness are either being disingenuous or weren’t paying attention.

This wasn’t unpredictable.

It was entirely foreseeable, and it was being ignored.

In May, Japan’s 30-year government bonds hit 3.1%. I called it a structural breakdown.

Today? They’re at 3.3%.

The 40-year? Up from 3.6% to 3.7%.

The 10-Year Yield has jumped to its highest level since the run-up to the Global Financial Crisis.

But more importantly, the entire dynamic I warned about is now in motion.

Prime Minister Takaichi has just unveiled a ¥17.7 trillion stimulus package - the largest since the pandemic. And instead of the textbook response where growth expectations push yields lower, Japan’s bond market is in open revolt.

This is the loss of confidence I warned about.

Remember when I said Japan’s issues weren’t Japan-specific? That they represented a broader crisis in sovereign debt credibility?

Now financial outlets are explicitly comparing this to the 2022 UK gilt crisis under Liz Truss - the one that nearly broke the British bond market and ended her Prime Minister run in just 49 days.

Deutsche Bank’s global head of currency research is warning of ‘unruly capital flight.’

Portfolio managers are describing it as ‘the same conversation the market has been having about the UK for essentially the same reasons.’

One fund manager told Reuters: ‘I can’t find any reason to buy JGBs now.’

This is what a crisis of confidence looks like.

The Capital Repatriation Is Happening

In May, I explained how rising Japanese yields would trigger a global chain reaction - Japanese institutions would pull capital from US Treasuries and European bonds to reinvest at home.

That withdrawal is now underway.

Japanese life insurers have been net sellers of super-long bonds for three consecutive months - the longest selling streak since 2004. Foreign buying has slowed sharply. FX-hedged returns on US Treasuries are negative for Japanese investors.

The maths is simple: why hold US debt at a guaranteed loss when you can earn 3.3% at home?

And remember - Japan holds more US Treasuries than any other foreign nation. Their withdrawal leaves a hole that US domestic investors are struggling to fill, precisely as the US needs to refinance $7-9 trillion in maturing debt.

Here’s something else: the yen has fallen 6% in seven weeks even as the US-Japan interest rate differential has narrowed.

That’s not normal. That relationship is usually tight and predictable.

The breakdown suggests either a ‘Sell Japan’ narrative taking hold, or - more worryingly - that the traditional relationships investors rely on are no longer stable.

When correlations that held for decades suddenly break, it’s a sign the system is repricing something fundamental.

Bitcoin and the Flight to... What Exactly?

Bitcoin has crashed from $126,000 to $80,000. Even gold has fallen back to $4,000 an ounce.

This is exactly what happens during a liquidity squeeze and deleveraging event. Everything gets sold to meet margin calls. Leverage that amplified gains on the way up now accelerates losses on the way down.

And the Bitcoin crash wasn’t driven by anything specific to crypto fundamentals. It was purely a function of how money moves during systemic stress.

When the carry trade unwinds, hedge funds close positions indiscriminately. Bitcoin, as one of the most liquid assets available, gets hit hard and fast.

The question is what happens next - whether Bitcoin eventually decouples as a monetary hedge when investors realize they’re choosing between government bonds of questionable value and scarce digital assets immune to central bank manipulation.

Gold already seems to have made that transition. Goldman maintains a $4,900 target by the end of 2026.

The question is whether Bitcoin follows.

The Institutional Exodus

In May, I showed you Bank of America data: a net 38% of institutional investors were underweight US equities - the lowest level since May 2023, and before that, since just before 2008.

I said the professionals would win versus retail, who were buying the dip with record enthusiasm.

Since then, stocks have continued to go up - purely on retail buying as institutions exit.

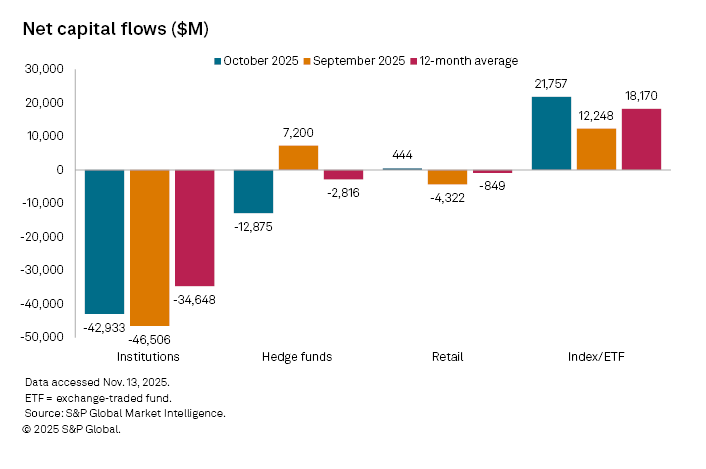

Institutional investors sold $42.93 billion of stocks in October, above the $34.65 billion sold on average over the past 12 months, according to S&P Global Market Intelligence data.

One side of this trade is going to be proven catastrophically wrong.

The Central Bank Response: Print More

And what’s the policy response to a bond market crisis driven by too much debt and too much stimulus?

More stimulus.

Japan: $110 billion package.

United States: considering $2,000 direct payments to citizens, ending quantitative tightening (restarting the money printer)

China: $1.4 trillion in economic support.

Canada: resumed quantitative easing.

The sheer scale of coordinated monetary intervention is staggering. And it creates a paradox where the very assets meant to be ‘safe havens’ - government bonds - face growing credibility questions.

If you keep printing money to solve a debt crisis, eventually people start questioning the value of the money you’re printing.

Bond traders are now shorting the entire Japanese yield curve, including the previously stable 5-10 year sector that had experienced less selling pressure.

Asset Management One’s CIO: ‘With fiscal and monetary policy risks now rippling across Japan’s bond markets, I’m short the entire curve.’

RBC BlueBay’s CIO: ‘We’re short Japanese debt, particularly in the 10-year sector. If there’s a sense that the idea of policy error is growing in Japan, we would be adding to the short.’

These are major institutional players positioning for a breakdown in market functioning.

This Shouldn’t Be Surprising

So when I see headlines expressing shock at market weakness, or talking about AI bubble fears, I have to ask: are you not paying attention?

The signs were there:

Record institutional underweight positioning in US equities

Buffett’s historic cash hoard

Japan’s yield curve control breaking down

The unsustainable maths of global debt refinancing

Rising long-term yields despite central bank intervention

This was all visible.

The playbook hasn’t changed from May. To stabilise bond markets, policymakers need to crush risk appetite. That means engineering a major equity selloff to trigger a flight to safety.

It’s not that they want a crash. It’s that they may have no choice. When inflation stays sticky, debt issuance stays high and bond buyers stay cautious, the only remaining lever is to break investor confidence in risk assets.

The forced deleveraging creates the panic that drives capital back into government bonds, bringing yields down and restoring order.

We may be in the early stages of exactly that process now.

The Uncomfortable Truth

Markets that are detached from fundamentals can stay detached longer than seems rational. I said that in May, and it’s still true.

But the fundamentals eventually matter. And when they do, the adjustment is violent precisely because the distortion was allowed to build for so long.

Japan’s bond market is screaming. The UK gilts are at multi-decade highs. US long-term yields are surging despite the Fed’s backdoor support operations.

And while the professionals are positioned defensively, retail is buying the dip.

What we’re seeing now is simply the bill coming due for decades of monetary experimentation, unlimited stimulus and the fantasy that sovereign bonds could remain risk-free assets in a world drowning in sovereign debt.

The good news is that once risk appetite is crushed, and bonds saved, the only answer they have is to turn the money printer back on.

The recovery will be as sharp as the fall.

Get ready for pandemic era streaks.

Ya know, in Monopoly money terms.

Charles, another exceptional article. Really appreciate your insight & willingness to share with people like me who don’t have the full comprehension. Thank you.

Sounds to me like it’s time to take some money out the market. The only problem I’ve got is that QE could/should push the market higher.

But hedge your bets - hold some cash has to be the sensible position…