Small Cap Mining: June Review

it's all coming together?

Good Morning Team.

As we close the book on May, it’s time to sit back, lie back in your lawn chair - crack open a beer or three - and get reading.

Let’s start, as usual, with the macro front.

Sydney Sweeney is promoting soap manufactured from her bath water, and Only Fans is planning to sell itself for $8 billion.

I think these twin facts alone prove that rates are possibly not high enough.

But already, I digress.

Once again, it’s all Trump.

His pesky tariff strategy is built on increasingly shaky legal ground.

The US Court of International Trade recently blocked his administration's latest IEEPA-based tariff order, setting off a cascade of potential legal delays - yes they’ve been unblocked for now…

…but we now have a White House where major legislation is stalled, tariff policy will be stuck in courts and Congress for years, Trump will fixate on tactical escalation with China (including Visa bans and export controls) - and the best we can hope for is that the Democrats take back some control in the 2026 midterms and put him back in his box.

It’s worth noting that Goldman Sachs and others think that while IEEPA-based tariffs may be stalled, Trump has several fallback options:

Section 122 of the Trade Act of 1974 — Allows temporary tariffs (up to 15%) for 150 days without any formal process, citing threats to the US balance of payments.

Section 301 — Enables tariffs after trade investigations - slower but permanent.

Section 232 — Allows sectoral tariffs (eg, on semiconductors, pharma) under national security pretext.

Section 338 — Rarely used tool that imposes up to 50% tariffs on discriminatory nations without investigation.

The likely path forward? Trump reissues a 10–15% across-the-board tariff under Sec 122 if needed, buying time to initiate Sec 301 probes. The market, oddly, sees this as business as usual.

It’s literally gone numb.

In 2018, a surprise tariff announcement could shave 3–5% off the S&P 500 in a day. Last week? The largest drop in US imports in history (April 2025: −19.8%) barely registers. Volatility remains subdued, and valuations high.

But this calm belies real disruption. While Wall Street clings to short-term earnings momentum, the structural risks are growing deeper.

Let’s consider the market posterchild.

Nvidia reported record Q1 revenue of $43 billion. But a closer look at geography reveals red flags:

$9 billion routed through Singapore

$5.5 billion from China and Hong Kong

Combined: $14.5 billion, or ~34% of all Q1 revenue

Nvidia claims that 99% of Singapore sales are to US-based customers, meaning they should technically count as ‘domestic’ under accounting rules. But here’s what’s really happening:

US resellers (Supermicro/SMCI) purchase chips from Nvidia.

These purchases are invoiced through Singapore or Malaysia.

The chips are resold to Chinese clients.

End result? Nvidia books the sale as a US transaction via Singapore, circumventing export control optics while continuing to feed China’s data centres.

This has prompted Nvidia’s longest-ever disclaimer in their 10-Q, defensively outlining their geographic revenue structure.

Come on Jensen. This is legal arbitrage disguised as customer diversity - and will come to bite them soon.

Huang notes that ‘The question is not whether China will have AI. It already does. The question is whether one of the world's largest AI markets will run on American platforms. Shielding Chinese chipmakers from U.S. competition only strengthens them abroad. Weakens America’s position. Export restrictions have spurred China’s innovation and scale. The AI race is not just about chips. It’s about which stack the world runs on. The U.S. has based its policy on the assumption that China cannot make AI chips. That assumption was always questionable, and now it's clearly wrong.’

Basically this is a plea to Trump not to stop chip exports to China properly. But he’s not confident Trump is listening - so the CEO is selling $800 million of his own Nvidia stock.

In the latest escalation, the Trump administration recently announced the revocation of visas for Chinese students, particularly those in tech fields or with alleged Communist Party ties.

Combined with export bans on chip software, design tools, and jet engine technologies - alongside Trump’s recent whining about China breaking a trade deal that doesn’t exist yet - it serves as a reminder that the market can crash just as fast as it’s recovered.

We are not out of the woods. Add in the increased steel and aluminium tariffs (to some 50%) and you start to wonder where we could go next.

And you can bet your bottom dollar that when China and the US spat again, it will be over rare earths (or lack of supply thereof). Remember, rare earths are in dollar terms only a tiny percentage of GDP which belies just how ridiculous the valuation gap between tech and metals has become.

And don’t get me started on bonds. Japan can pretend they’re going to cut borrowing, but bottom line they have too many old people and no immigration.

It’s not going to happen - they’ve bought a reprieve not a pardon.

And they’re also not playing ball on tariffs.

Dimon knows what’s coming - and has publicly warned that a ‘crack in the bond market’ is in our future - and further, that Powell is right not to cut rates yet (despite the orange one begging him to in person).

He’s ‘quite prepared’ for rates to hit 5% - which means he’s ready for the 10 year note yield to hit 5%.

JP Morgan’s top man also warns that the US should be ‘stockpiling guns, bullets, tanks, planes, drones, rare earths.’

Not Bitcoin. Real, hard assets.

Consider: ‘China is a potential adversary, they’re doing a lot of things well, they have a lot of problems...But what I really worry about is us. Can we get our own act together, our own values, our own capability, our own management.. we have to get our act together and we have to do it very quickly.’

‘Trump’s agenda would push U.S. allies toward China.’

And apparently, regulators are going to - straight up - panic.

He might as well be embodying 21st century philosopher Taylor Swift, ‘Boys only want love if it's torture. Don't say I didn't, say I didn't warn ya!’

Because if bonds yields are rising while USD is falling, then we are in big trouble.

In the UK, Labour is borrowing £20 billion per month at objectively terrifying levels of interest, and instead of sorting this out, Starmer is busy marking Reform’s maths.

Between the possible forced investment of UK pension funds into shit private companies incapable of attracting investment independently (read a stealth tax where you get lower returns so the government can reduce its own borrowing costs) - and Capital Gains Tax falls as a result of non-dom changes, and that truly awful interview where he claimed to know what hard work is because his Dad did, I’m actually starting to feel sorry for the man.

Which politically means he’s toast. So’s Kemi by the way.

I’m sure that sympathy will disappear when Reeves starts reducing pension tax relief.

God knows what a Reform government will do to gilts, but I reckon we might find out in the not too distant future.

The Golden Trio

There’s a new Golden Trio for Harry Potter fans, but I’ll stick to my OGs.

This month, Sovereign Metals entered a MoU to secure grid power for Kasiya with the Electricity Supply Corporation of Malawi, setting out a strategic development workplan to supply 60MW of hydropower for steady-state operations, through connection to the Nkhoma Substation.

The company also noted that Malawi’s national grid power is expected to be significantly improved by the World Bank's recent approval of a $350 million grant to support the Mpatamanga Hydropower Storage Project, which will hugely increase Malawi's installed capacity by 2030.

This storage project has been co-developed by the Government of Malawi and the International Finance Corporation (part of the World Bank Group) and includes Tier 1 owners EDF, British International Investment, Norfund and TotalEnergies.

Access to sufficient energy (despite Kasiya’s overall low energy needs) was perhaps the final major piece of the puzzle to sort before the publication of the DFS in Q4.

There is a spanner in the works of course - Rio Tinto’s CEO Jakob Stausholm is amicably splitting with the company - reportedly over disagreements regarding board priorities focused on controlling costs, rather than expansion

As Kasiya is a genuine Tier 1 asset, I still think the most likely outcome is that Rio buys it. However, the chances of this happening before the DFS have now shrunk, simply because major purchasing decisions will be down to the new CEO - who will take time to be appointed and get up to speed with the company’s position.

As a reminder, when the DFS is published, Rio has 180 days to decide whether to take operatorship - if they do, a buyout becomes inevitable.

But for now, I expect SVML will be concentrating on gaining accreditation from the major titanium houses - to help focus minds, to ensure they have alternative financing waiting in the wings if needed, and to guarantee that Rio is aware they have competition for the asset.

And as for the share price? Someone bought £832k this month (and then looks at those massive trades today) - these likely went through over a period of weeks, but those scaled out of the placing may be quietly buying more at this lower price anyway.

Greatland Gold (Resources) is getting closer to its ASX listing. Long-time readers will know that I’m very bullish on what happens to GGP when this happens - on an ASX peer comparison basis, the stock is still very undervalued and I expect we will see 20p+ in the near future.

This isn’t an entirely subjective opinion - all you need to do is compare the market capitalisations, current gold production, AISC and ounces in ground to others in the same Aussie space.

It’s not rocket science.

But in the run up, there are a few interesting factoids to digest.

First was watching multiple directors and senior employees let go of nearly 500 million options at 6.64p per share - at the current share price of 14p and an intrinsic value of 7.36p per option, that’s letting go of £36.8 million at face value.

And they’re reinvesting 50% of the 6.64p payout back into GGP.

This is both unheard of and an impressive display of confidence - because while charity exists - the only reason they would do this to secure the ASX listing is if they believe it will make them even more money.

Yep.

Speaking of the ASX listing, Shaun - employing the wiles of the wiliest fox, one perhaps who has been appointed Professor of Cunning at Oxford University - has set up an entity to oversee the orderly transition of Newmont shares to the bookbuild, one in which Shaun is the sole shareholder.

Sorry chaps, no market maker shenanigans allowed here.

It was no secret that Newmont wanted out, so it’s good to see this being managed well.

One final note - today’s RetailBook offer advises that the issue price will be determined at the close of the bookbuilding process. I expect it to be oversubscribed (current shareholders get priority) - but also to be at a small discount.

Maybe not, but is is standard procedure - so while not advice, if you are thinking of adding, you may get a few more shares for your money this way.

Priority for existing shareholders is a hint at this.

Or maybe not :)

Finally, Amaroq Minerals enjoyed an action-packed month. Q1 2025 results saw the Greenland frontier company advise that it’s now reaching mining rates of up to 220t/d of ore, which is being stockpiled.

It’s also in the final stages of agreeing mining KPIs with contractor Thyssen, to support feeding the plant with enough ore to allow it to reach the hoped-for 300t/day by the end of the year.

And then it’s printing money. For perspective, as AMRQ continues to test each component, throughput rates are steadily improving - and next it’s commissioning and calibrating Phase One.

Remember, the company also recently saw a 51% increased Mineral Resource, including a maiden indicated resource for Nalunaq.

On the financial side, there’s group liquidity of $23.4 million as at 31 March 2025, consisting of cash balances of $16.7 million, and an undrawn revolving credit facility of $23.7 million, less trade payables of $17 million.

This should be sufficient capital given the record gold price (thanks Donald) and low oil price (thanks OPEC) - with energy perhaps as much as 50% of AISC for Nalunaq given the mine’s geographical siting.

But if capital is ever needed, they only raise it properly.

On the critical minerals front, the Gardaq JV (conducted with the same chaps backing Power Metals’ uranium campaign, Guardian’s tungsten and Andrada’s tin among others) saw extensive geological reconnaissance, mapping of previously unexplored terrain, geochemical sampling - and most importantly given that all discoveries ever made thus far have required a drill bit - 5,524 metres of core drilling across three high-priority projects.

Gardaq now holds the majority of the licenses across a prospective belt that hosts South Greenland’s first copper porphyry system at Target West. Three new licence applications across Greenland have also been submitted, targeting copper, gold, and rare/critical earth elements.

James Gilbertson, VP Exploration notes that ‘key highlights include the discovery of new porphyry and epithermal systems, confirmation of a cobalt-rich nickel-copper target at Stendalen, and strong early results at Ukaleq — all reinforcing South Greenland’s untapped potential…With new drill data, geophysics, and assay results in hand, Amaroq is well positioned to prioritise 2025 follow-up programmes — including potential further drilling at Stendalen and Ukaleq.’

A deep dive into the company’s exploration is overdue and I am working on this.

Perhaps most critically, Amaroq Minerals has also announced the formation of a new joint venture company, Suliaq A/S, with UK-based JLE Group to provide essential services and assets to Greenland’s mining sector. JLE will initially invest £4 million for a 10% stake in Suliaq, with the option to increase its total investment to £12 million, while Amaroq retains 90% ownership and Suliaq operates independently.

CEO Eldur Olafsson enthuses that ‘With exploration spend in the region increasing dramatically over the past five years, and with the growing interest in Greenland’s emerging mining, energy and infrastructure sectors, Amaroq is uniquely placed to facilitate the provision of essential services within this growth market. With the support of a JV partner of the calibre of JLE, I am confident that we will be able to significantly de-risk activities and create substantial value, not just for our own shareholders but also for Greenland and its people.’

Amaroq is at the forefront of this new frontier. If the gold production gets to nameplate by the end of the year, then the company has the power to explore the entire island for minerals with capital no other party has.

There is a bigger picture here.

It seems someone knows this - as the company was filing the technical report for Nalunaq on SEDAR+, the price on the Canadian exchange more than doubled.

Amaroq later noted it was ‘unaware of any material change in the Company’s operations that would account for the recent increase in market activity.’

But someone’s keen.

SVML shares are down 16%, GGP up 125% and AMRQ down 15% year-to-date, for a total positive return of circa 31% year-to-date.

The Explorers

When covering African explorers like Rome Resources & Arc Minerals it often feels like only one is ever doing well - while the other is struggling with sentiment.

A few short weeks ago, M23 rebels had overrun Rome’s neighbour - Alphamin - the stock had sunk to as low as 0.14p and sentiment had all but collapsed.

As I noted throughout, the world was not going to tolerate Bisie going offline (especially with the chaos/human disaster in Myanmar), so it was only a matter of time before Rome would be back at site - which they now are.

Once again though, this is the danger of operating in the DRC. You have probably the best and largest mineralisation anywhere in the world - but one of the most difficult jurisdictions politically.

If you are going to invest in a DRC play, you need a political powerhouse - and Rome has this in the form of Klaus.

The company plans to soon release its maiden MRE (CIM guidelines) in an NI 43-101 Technical Report, which will include an assessment of the prospects for eventual economic extraction.

With three rigs finally drilling deep at Mont Agoma - the zonation model being of copper and zinc dominant near surface and tin strengthening at depth - we shall soon see if the high grade tin we’ve spent all this time waiting for is present.

It’s the same team that found Bisie. I’m cautiously optimistic.

For Arc, we are feeling what happens when you hand control of your primary asset to a major in exchange for a shedload of cash to explore it.

The rainy season is over. Anglo American is committed to spend $21 million - realistically - by the end of calendar 2026. And the vast majority of this capital is going to be in the form of drilling.

In the unlikely event they walk away, ARCM gets this in cash and drills themselves.

In the most recent RNS, Arc noted that targeting options for 2025 include Fwiji and Nyambwezu that have not been previously tested - and the new Cheyeza prospect. This is going to require more than one rig.

Anglo is exploring like a major, because it is. They have the time horizon and budget to slowly zero in on high grade targets. It's lower risk but slower. A junior going it alone will go down the higher risk route of trying to find the higher grades faster because they lack the resources to do it properly.

Chair Nick von Schirnding noted he looks ‘forward to reporting back to shareholders over the coming months in respect of our various drilling plans as the rainy season comes to an end.’

This has been widely misinterpreted - this means that the Chair is hoping to report back on drilling in the near future, not have us waiting months for plans to materialise.

These are some of the best copper exploration licences in the world, and unlike Rio Tinto, Anglo is 100% focused, and committed to copper.

On a side note, it’s interesting to see ARCM note that ‘depending on the timing of the proposed acquisition of the Chingola Project and associated scope of work, (we) will either commence drilling in Botswana or progress its work programme at Chingola.’

To my mind, this suggests that ARCM plans to sell the Botswana asset to MMG and use the proceeds to explore Chingola. We know Chingola was fiercely contested - and others may be happy to share in the expense.

It’s clear the company was expecting to announce news at Proactive last month, and then pulled out.

Junior explorers should not be the core of anyone’s portfolio, as there is always inherent risk. But these two have some of the best prospects out there - and when there’s share price weakness, then often, fortune favours the brave.

The Dealmakers

Asiamet. I covered the stock in detail a couple of weeks ago, but the core message?

The BKM copper project is no longer a speculative dream — it’s fully de-risked, shovel-ready, and staring down two inevitable outcomes in 2025: get financed or get bought out.

With the Optimised Feasibility Study complete, a fresh ore reserve update, and the ITE report in hand, the project is technically validated, economically attractive, and politically aligned with Indonesia’s strategic goals.

Backed by $1.192 billion in life-of-mine revenue, a modest $178M capex, and a £26M market cap, the upside is obvious.

Asiamet has stripped the project to its most financeable, cash-generating core — and now the clock is ticking. The decision point is approaching, and I can’t wait to cross this one off the list permanently.

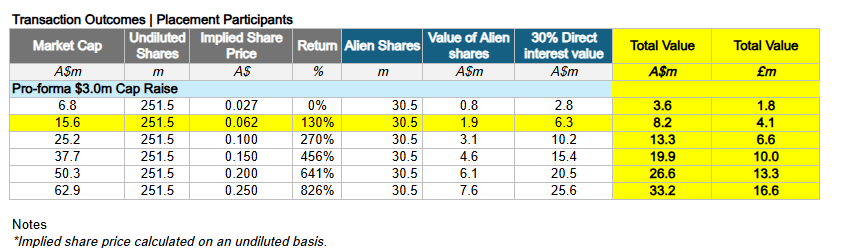

Alien.

JV partner West Coast Silver has recorded multiple portable XRF surface sampling results at Elizabeth Hill, up to a stunning 920g/t. These high-grade readings have come circa 300m to the north and 150m to the south of the known Elizabeth Hill mineralisation envelope, and correlate with the location of the Munni Munni Fault system.

Drilling is now underway, with the first hole of a 1,500 metre inaugural diamond drilling programme ongoing.

The implied value to Alien is very strong:

And Alien also got another grant: up to A$25,000 from the Western Australian Government to co-fund an extensive ground gravity survey over the most geologically prospective areas at Pinderi.

Yes, it’s a piddly amount, but the political support is welcome.

Of course, the real value will always be Hancock.

The good news is that we have two new exploration leases, E47/5157 and E47/5158, granted with no Native Title objections. These are adjacent to the existing Mining and Exploration Leases at Hancock Project and expand the Company's exploration area by more than 50% from 41 square kilometres to 63 square kilometres.

Rock chip sampling and an assay programme is the plan.

But we’ve had another fundraise. On one hand, there comes a point where the company simply has to deliver external financing for this asset - and on the other - this additional £1 million was raised at the bid, and the stock is above the placing price.

I believe Christopher Maiolo will get it done.

But goodwill only runs so far.

Blencowe? Again, just covered this - but as a tl;dr, BRES has received another $500,000 from the Development Finance Corporation, bringing total grant support to $4 million.

The company is nearing completion of its DFS for the world-class Orom-Cross graphite project, with recent drilling confirming further strong resource potential and low-cost extraction.

Despite earlier funding delays, Blencowe has progressed exploration, secured infrastructure, and begun commercial engagement with offtake partners - positioning itself for major project-level financing and a potential near-term re-rating.

Bezant? Again, covered days ago, but in securing key regulatory clearance for its flagship Hope & Gorob copper project in Namibia, and extending its loan facility to improve financial stability, we’re well on our way.

Also, its stake in the Mankayan project via IDM - now merging with ASX-listed Blackstone Minerals -provides BZT with a valuable £5.4 million equity position, potentially usable to support project financing.

I was informed by several readers that this merger has been pushed back by a few weeks compared to the timeline of my original article - but is still very much on.

Energy Pathways? I intend to do conduct a thorough technical review of the project over the next few weeks so will save that for later - but it’s great to see the CEO chew out the government.

It’s clear that private funding for MESH has already been secured (at multiples to the current share price, though I’m sure this is least in our priorities :)).

Remember, in the Telegraph Ben advised ‘We don’t want any public money. We just want permission to get on with it.’

It’s also clear that this private capital (a) will not wait forever as opportunity time cost is a very real thing, that (b) they can't deploy the capital unless the government gives EPP licenses for the energy storage and (c) the government is dragging its heels, possibly due to incompetence or perhaps the complete inability to make an actual decision.

The government recently published an open letter saying they want more energy storage (as part of the net zero strategy) and Ben fired one back effectively calling them out for being the reason why it's not happening as quick as they would like.

In a world where we pay £300,000 per bat building a special tunnel for HS2, close down coal mines only to ship coal from Japan to keep the steelworks’ lights on - and even charge a 78% tax on North Sea production (while banning further exploration/exploitation), it’s hard to expect any real joined-up thinking.

But we do need a signature Ed, so sort it out.

Then, Guardian Metals. Another stock that requires a refreshed deep dive - which I will pen this summer as the traditionally quieter period arrives - but a couple of comments on the geotechnical update for Pilot Mountain:

Multiple geotechnical holes means that the mineralising system at Desert Scheelite extends beyond what was already known. And the visual mineralisation at Garnet Zone probably means there’s even more potential.

But the key is grant funding.

Trump is desperate, literally, to reshore critical minerals to prevent China from keeping his balls in a vice. Executive Order after Executive Order keep coming - and it helps that tungsten pricing is reaching record highs as China decides to keep tightening its grip.

You need this stuff to have a functioning military.

I’ll stick my neck out here: the first tranche of grant funding lands in June.

Finally, Power Metal Resources. My only comment for this month is that when the CEO and other management spend their own money on shares, it generally means they expect the stock to rise.

It’s got millions in the bank, and a massive fully-externally- funded uranium campaign in the world’s No1 uranium address about to kick off.

Patience.

Jubilee & African Pioneer

The re-rate for Jubilee is all Roan. On the one hand, we can all breathe a sigh of relief as JLP has now successfully technically validated the concentrator - with the ability to process previously overlooked shallow transitional copper ore, achieving copper yields of around 65%.

This not only validates its proprietary processing capabilities but also unlocks value from what other operators considered waste (the proven chrome model).

The company has also secured long-term feedstock - and promised that production from Roan and Munkoyo is projected to increase steadily to 500–550tpm Cu units by October 2025.

We’ve also seen some decent monetisation of non-core assets worth $12.3 million and commenced a $6.75 million trade of 10 million tonnes from its Large Waste Project - avoiding dilution.

On the other hand, the delayed restart has affected output - and getting Roan to full capacity is going to take more time. Like many small caps, it’s an elongated waiting game, but with copper racing ahead and South African operations running smoothly, then as long as Leon can deliver this new timeline, the 2025 re-rate stands.

On the technicals, we need an interview - and I’m trying to secure one asap.

African Pioneer is imho now positioning for a breakout as it transitions from an explorer to a near-term copper-gold producer, driven by accelerated development at its Ongombo Project in Namibia, where it has secured key permits, advanced infrastructure planning, and is evaluating toll processing to fast-track production.

At the same time, its strategic alliance with First Quantum in Zambia is gaining momentum, with drilling highlighting early signs of Congo-style mineralisation, ahead of potentially high-impact assay results and a maiden resource definition.

Yes, this stock has disappointed from a share price view - but it’s illiquid. A fats move back up is viable.

Helium Pick

My top helium pick for this year - Helix Exploration - fell below 12p in mid-April, but has since recovered to above 20p and is now up circa 15% year-to-date.

This is what comes of doubling down on your convictions when your stock is on the floor.

I floated the potential numbers when the stock was around this bottom - and they’re very, very good.

In May, we saw Linda #1 deliver flow rates of some 3,850 thousand cubic feet per day of raw gas at 40/64" choke, which is some 40% above the flow rates reported at Darwin. High grade helium was assayed at 1.2% - with most of the rest of the gas being hydrogen.

The company notes that Linda can generate pre-tax cashflow of $4 million a year in line with projections. Theirs (but also mine).

CEO Bo Sears enthuses that Rudyard is ‘not only productive - it's scalable. With exceptional flow rates, a large structural footprint, and strong early gas quality, we now have a foundation to build a long-life domestic helium supply project.’

Production this summer.

Summer starts tomorrow.

If Weil #1 results (due imminently - I hate that word too) are up to scratch, then the march to 25p+ seems inevitable.

The Moonshot

Emmerson is back up to 2p, a gain of around 170% year-to-date. Again, there’s a chance here to de-risk, and there is no shame whatsoever in taking some profits off the table when it comes to litigation plays.

At the start of May, the company submitted a request for arbitration to the International Centre for Settlement of Investment Disputes, an arm of the World Bank, with regard to various breaches by Morocco of the agreement between the UK and Morocco for the Promotion and Protection of Investments, which entered into force on 14 February 2002.

As a reminder, Emmerson is claiming full compensation over the Khemisset Potash Project which it has internally valued at $2.2 billion - with all legal costs and much of the G&A funded by the $11.2 million litigation facility already in place.

Boies Schiller Flexner (the big guns) is now working on the formation of the arbitral tribunal and preparing a formal Memorial submission.

This is the first formal step in the arbitration process - the evidentiary hearing where it gets juicy is two years away.

This means you will have plenty of opportunity to trade the stock - but if you think their case is sound (I do), then waiting for the payday feels like a winner.

Final Thoughts

The only stock I picked up on for May as a special was Afentra - ‘No sweat there, it’ll sort itself out.’

I interviewed CEO Paul McDade at the start of the month and the stock has now risen to 45p (up >20% in the month). With oil showing signs of recovery and the fundamentals all in place, I expect it will rise to 50p soon, but I’m glad to have played a small part in highlighting both the short term trade and substantial long-term opportunity to a wider audience.

As a short term pick for June, I’m going with Coinsilium. The crypto treasury story is only just getting started - and it seems likely (to me at least) that at least some of the profits from Smarter Web will flow into Coinsilium as investors hedge their bets on which UK stocks will win the war.

FWIW, capital will also continue to trickle down to others as the gap between NAV and mcap increases too much to be sustainable for each company that comes along - and investors continue to reduce their risk exposure.

But as a trade, it’s in my view a decent shot. I can also guess which ‘leading UK small cap fund manager’ Jerry has put on the register, and they’re the type to hold for ‘digital’ gold.

Speaking of trades, consider Mirriad Advertising. It’s a scalp trade.

Get in.

Get out.

There may be a chance for longer-term profits now, but the volatility there is a quick profit dream - just be up front about it if that’s your plan.

As a final thought, MET1’s successful campaign to sort out its share price has attracted the attention of a myriad of other companies. You will know the names - make your profit (I am) but as ever, pigs get fat - and hogs get slaughtered.

Have a fantastic month - and remember to enjoy the sun!

On Jubilee, they received an offer to acquire the PGM and Chrome business. It's disappointing the board is even entertaining the idea given;

1. $25 million EBITDA in FY24 and on track to hit $30 million in FY25.

2. NAV of $120 million.

3. Monetisation of excess PGMs (7 kOz) and more still to realise.

4. Chrome production still to reach installed capacity of 2.1 million tons.

5. PGM basket price up with supply deficits deepening during a period when the auto sector is recovering and platinum is gaining favor as an investment asset.

6. Modest net debt ~ $10 to 20 million.

Yes they need the cash to fully realise the copper strategy ($12 million per mine, 2 mines) but they will have $16 million from selling resources in the next 12 months.