The Bubble is Going to Burst in 2025

and it can't happen fast enough.

Good Morning Team.

Anyone for some Tulips?

‘There is nothing in this world which will so violently distort a man’s judgement more than the sight of his neighbor getting rich.’

It’s time. I have had a fantastic run in the large caps over 2024 (and particularly in Q4), but it’s time to admit that the music is going to stop.

The last time I wrote something like this was on 12 December 2021, shortly after which on 18 January 2022 I correctly called that the UK’s premier index would beat the S&P 500 in the year. I was right to assess that 2022 would be a poor year for the US, and I think I will be right again.

And then at the tail end of 2023, I covered a number of large cap ideas, which have returned circa 55% year-to-date if you invested in them all equally:

Gold

Dow Jones

Nvidia

Rolls-Royce

Coinbase

Anglo American

Marks & Spencer

3i Group

Disney

Centrica

AB Foods

Links for these predictions are all here:

https://www.ig.com/uk/trading-strategies/top-investments-to-watch-in-2024-231215

https://www.ig.com/uk/trading-strategies/are-these-the-top-stocks-to-watch-in

https://investingstrategy.co.uk/stock-tips/disney-shares-the-bull-case-for-2024-and-beyond/

This newsletter has no affiliation with IG Index.

But now I’m almost completely cashing out of the large caps. Because this has got ridiculous, and I know when to count my blessings, go to the pub, and wait for all of this to blow over.

Instead of stock picking large cap, blue chip stocks which may do well over 2025, I am instead going to be brave, and against the common wisdom of almost every investment bank out there, tell you that the market is going to crash next year.

Before we go any further, this is not advice. Simply a personal prediction.

The music might keep playing.

There are three things to bear in mind before we continue:

Individual businesses with a solid plan and a strong balance sheet should be relatively unaffected. I am staying invested in select small caps for the payday. For example, AI start-ups will continue to attract capital.

When the crash bottoms, this may be a very rare opportunity to buy a generational dip in everything from Bitcoin to Amazon. Markets have always recovered in the past, and while past performance is not a guarantee of future results, the S&P 500 has delivered an average of +10% a year since its modern inception in 1957.

Small caps may be hit initially, but then we will get pandemic style rises, and a healthier market where capital is redistributed more fairly to the smaller end

For the purpose of this article, I am going to define a ‘crash’ as a 20% drop in the S&P 500 from its closing price at the end of calendar 2024, to whenever it has lost 20% in 2025. Once it gets to this point, I will reassess. But I think it will fall further.

For context, the S&P 500 fell by 49.1% in the 2000 dot-com crash, by 56.8% from October 2007, and by 33.9% in the pandemic flash crash of 2020. The dot-com bear market lasted 31 months, the Global Financial Crisis 17 months, and the pandemic flash crash just one month - before the recovery got started.

So why the crash?

The first thing you need to understand about the market capitalisation of the largest US stocks - the ‘magnificent seven’ - is that when we say that Nvidia has a $3.3 trillion market capitalisation, and that shares are currently changing hands for circa $130, it actually means that 1% of the shares that are traded each day change hands for $130.

Today, 1% of Nvidia is worth $33 billion, but 100% of Nvidia is not worth $3.3 trillion.

If you have significantly more sellers than buyers, and higher than usual volume, the market cap can tank in a matter of hours - and it’s not like there is suddenly trillions of dollars ready to flood into other sectors. It just never really existed in the first place.

What can happen is that capital that no longer wants to invest in Nvidia may go elsewhere.

But before we go too deep into stocks, let’s talk Bitcoin. Or more accurately MicroStrategy. Bitcoin is the ultimate Ponzi Scheme - it might go on for years or even decades, but one day someone’s going to be left without a chair.

And MicroStrategy is going to crash long before Bitcoin collapses.

Let’s consider what CEO Michael Saylor is telling you:

Buying BTC now is like buying Manhattan 300 years ago.

Every day is a good day to buy Bitcoin.

The US government should sell all of its gold and buy Bitcoin.

And a direct quote: ‘Soon every billionaire will buy a billion dollars of Bitcoin and the supply shock will be so great that we will stop measuring BTC in terms of fiat.’

Only a small cap investor can recognise this for the ramping bullshit that it is.

We exist in a market where FartCoin has an $844 million market capitalisation. It has a higher market cap than silver’s annual production. Just get that in your head and roll it around for a while.

The thing is, Bitcoin has a circulating supply of 19.79 million coins at present (data from coinmarketcap).

I’ve just got the data from today - 3.21% of the volume of BTC out there was traded in the last 24 hours, and this is a ‘slow’ day. This means that every month 100% of BTC in existence is being traded. This does not include the many BTC in inactive wallets - this is full on meme trading activity.

It’s musical chairs based on a Trump-Musk sentiment rally and it’s going to tank. Earlier traders are not HODLing. This is not a store of value like gold. It’s the perfect sentiment trade, because sentiment is all it is.

And if you think this can’t happen, it already sank several times before. Consider the dot-com crash: hundreds of companies ‘worth’ $1.7 trillion literally went out of business effectively overnight.

The problem for MicroStrategy enthusiasts is simple.

Saylor buys says he will sell stock to buy Bitcoin. He buys Bitcoin. Bitcoin price rises. MicroStrategy stock rises. Saylor says he will sell stock to buy Bitcoin....

That's how you get a mcap 3x its portfolio 'value.'

It’s nonsense.

The company is simply preying on newer investors, pumping the stock, and driving BTC to new highs so it can raise funds and acquire more. This is 100% legal by the way - but if BTC goes through another long winter when Saylor owes the capital….

Then it’s toast.

The dollar cost average MicroStrategy is now looking at is in the region of $61,000 per Bitcoin.

Two years ago, one BTC was worth less than $17,000. The idea that it can’t crash to this level again is naive.

At some point, the trading premium will collapse, the conversion prices on the newly issued notes will feel too optimistic, and MicroStrategy shares will sink sharply during the BTC dip.

Yes, MSTR may be buying circa 100,000 BTC a month, and yes ETFs are also starting to buy in. And yes, there will only ever be 21 million BTC. But the coin is a store of sentiment, not a store of value.

Here’s a clue: El Salvador is widely seen as a BTC paradise - shops are required to accept it as currency, but only 7.5% of its citizens used BTC in 2024.

MicroStrategy getting into the NASDAQ 100 is a failure of corporate governance. There is meant to be a level of fiduciary responsibility - the company is not a proxy to BTC because it trades at a massive fuck off premium to the only ‘real’ asset on its balance sheet.

Joining QQQ will see around half a percent of the ETF’s AUM go into MicroStrategy, which will then issue more CLNs to get more BTC….

But this can only end one way.

Now let’s look at the magnificent seven.

Tesla’s valuation compared to peers is insane.

Of course, you can argue this is really a tech stock, or that it isn’t just a car company given the Powerwalls and Optimus robot, or may benefit from possible US tariffs, or is an extension of the Elon Musk brand….

but the valuation is a joke.

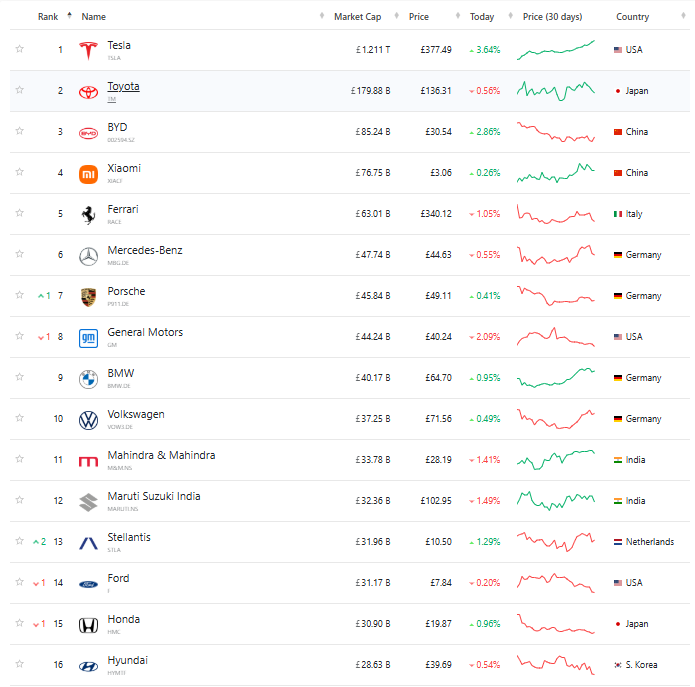

Consider the market caps in GBP:

Tesla is ‘worth’ more than every other competitor combined. One might imagine it has cornered the auto market, especially in its home turf of the US, but no.

Tesla sold 1.81 million vehicles in 2023, and in Q2 2024, its majority control of the US EV market fell below 50% for the first time. Yes, Elon Musk has won a victory as the $7,500 EV tax credit will be scrapped (it hurts Tesla, but hurts the competition far more than the market leader), but time is running out.

Here’s the context: JATO Dynamics puts the global total of all cars sold in 2023 at 78.32 million.

This means that Tesla sold 2.3% of all cars last year, but has a market cap 4x that of Toyota, which sold 10.6 million vehicles representing 13.5% of the global total - roughly 6-7x that of Tesla.

In financial terms, if you prefer, Tesla generated total revenue of $96.8 billion. The year before, it was $81.5 billion.

Toyota generated 37.2 trillion Yen ($238 billion) in revenue in 2023. Ford generated $176.2 billion in revenue and sold 4.4 billion vehicles.

These are the hard facts. Tesla has a price-to-equity ratio of 132. It’s madness.

This stock is trading on nothing by hype - and will course correct.

But it’s not just a car company Charles, it’s a magic robot company…

Wake up. Every robotics company in the world is worth less than $100 billion.

How about Apple? It’s trading at 10x sales, the highest valuation level in its corporate history. It sports a price-to-earnings ratio of 42. It has a $3.8 trillion market cap.

And fundamentally, it simply does not deserve this growth. iPhones account for half of all revenue, and fiscal 2024 saw sales grow by….wait for it….

1%.

The last real iPhone update was the iPhone X, back in 2017. Everything since has been a nothingburger. The Vision Pro? They’ve sold about three of them - and two of them were brough back for a refund. This was the first real new product launch since the Apple Watch, over a decade ago.

And the fuckers at the top know it.

Look at the insider selling. The FT notes that insider selling is at record levels, with six times more sellers than buyers.

Nvidia? Insiders have sold $1.85 billion in 2024, including pre-determined sales from CEO Jensen Huang.

Amazon? Bezos has sold $12.5 billion in stock in 2024, the most ever in one year.

Meta? Zuckerberg has sold $2.4 billion in 2024, even as the company hits record highs.

You know who’s buying? Retail, at record volumes. US off-exchange trading (proxy for retail investor participation) as a percentage of total market volume hit 57% in December. That’s a 15 percentage point rise. It’s double the pre-pandemic level.

And the two stocks seeing the most retail investment? MicroStrategy and Tesla.

But it’s not just the biggest guns.

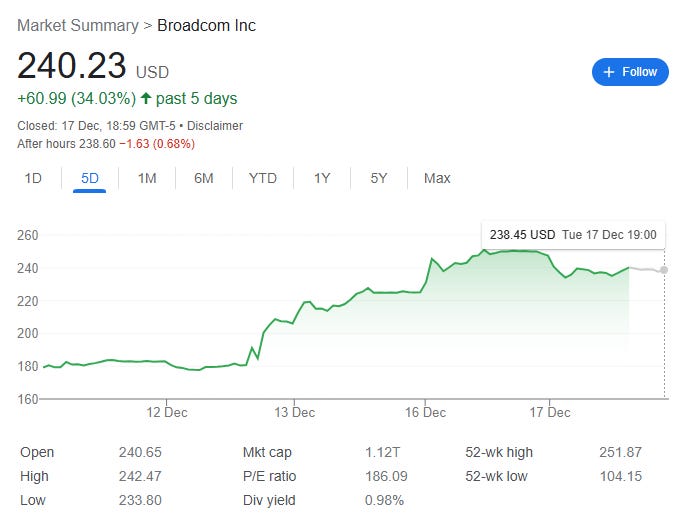

Look at Broadcom. It’s a trillion dollar company. This is not a functioning market:

And what about Palantir?

I love The Lord of the Rings as much as the next man, but this is a company with an annual revenue of circa $2.8 billion and a market cap of $169 billion. It’s profit margin is less than 20%. I’m not sure current investors have hundreds of years to make their money back, but here we are.

Let’s consider the wider S&P 500.

The S&P 500 is now on track for its second consecutive annual gain of more than 24%. This last happened in 1998 - you guessed it, right before the dot-com bubble burst.

The top 10 stocks in the index are ‘worth’ around $21 trillion, and have increased by $5 trillion since August. They are worth more than all the stocks in the UK, German, Canadian, Indian and Japanese stock markets combined. They account for 40% of the S&P 500, and this proportion keeps rising.

Total US stock market caps combined are worth circa $60 trillion - roughly double all Asian and European stock markets together.

And over the past two years, the S&P 500 has returned 60% to investors…

….but earnings are up just 5%.

The AI bubble is not delivering fundamentals just yet.

And the index has a forward price-to-earnings ratio of around 22x - significantly above the 16x average, and coming within touching distance of the 25x recorded before the dot-com crash of 1999.

Then we have the commercial real estate crisis. S&P Intelligence indicates that more than $2 trillion of commercial real estate mortgages will mature over the next two years, with the average interest rate on these loans taken out in 2020/21 at only 4.3%.

These will need to be refinanced at an interest rate roughly double that. If you think the subprime mortgage bullshit of 2008 was a problem, wait for this chicken to come home to roost.

Make up whatever narrative you want, but it’s going to implode.

And then there’s China.

10 year Chinese bonds currently yield 1.75% - 30 year bonds are just above this level. Alibaba, China’s Amazon, currently holds more than 40% of its market cap in cash.

Don’t even get me started on the TikTok ban in the US, or the escalating tit-for-tat exports bans.

And then the wider world

Germany’s government has collapsed.

France’s government has collapsed.

Canada’s government is collapsing.

And there’s another war being started every five minutes.

Just look at how quickly stocks have risen with Trump’s election victory - this is all euphoria and hype. Everything is rocketing, all at the same time. And all too quickly.

Everyone is an investing genius - and everyone not in yet is being dragged in by their friends. It’s the dot-com bubble with an AI overcoat.

And I think it’s going to crash.

Thank you for your insights Charles, you unpack this in a way that is more cutting than WSJ or the FT. Reading in hindsight sure provides an added layer of clarity on future investing moves.

Happy New Year Charles! Quick question on JLP. Why JLP and not GDP? GDP has consistently delivered higher ROA, ROCE and ROE. Plus is expanding into Brazil (derisking + growth plan). Plus has earmarked divis for next year having got through its capex cycle. Also on a p/e of 2.

Would be interested to hear your thoughts.