Small Caps: February Review

It's Only Been a Month!

Good Morning Team.

Sometimes, it’s hard to know where to start.

In 2026, the US administration captured Venezuelan President Nicolás Maduro and annexed the country’s oil rights (though the majors have made pretty clear they have no interest in processing it without political guarantees).

Trump also engaged in his annual January gambit for Greenland, which ended as it always does with the TACO trade.

Imploding NATO was never going to happen, though the natural result will be both the Europeans and the Americans funneling more capital into the island in an attempt to bring it closer to their own spheres of interest.

Towards the end of the month, Trump turned his attention to Iran, and while the situation is still simmering, jitters over the Strait of Hormuz, which flare up on a regular basis, sent oil higher.

I’ve explained this in the past: Hormuz will stay open; it is in the interest of no major world power for it to be closed.

Now, while it might be a good idea for whoever’s in charge of Donald’s meds to remind him to take his Ritalin (and possibly double the dose), this was not a ‘2026’ summary.

It’s a January summary.

We’ve got 11 months to go.

Of course, this macro sent paper precious metals pricing to the moon - and then Trump nominated Kevin Warsh to replace JPOW as Fed Reserve Chair.

This matters because the market had at one point been certain the man would be Kevin Hassett, the National Economic Council director.

When news broke, gold and silver collapsed.

Gold crashed from $5,600 to around $4,700. Silver fell from $121 to $77 — a 40% drop in less than 18 hours before recovering to close down around 30%.

The entire precious metals complex lost trillions and trillions of dollars in market value over 36 hours.

For investors who’d watched precious metals grind higher for months on expectations of Fed dovishness and mounting concerns about dollar stability, the selloff felt brutal.

But short-term price action and long-term fundamentals are not the same thing. While COMEX was crashing, something else was happening in the physical markets.

The same ounce of silver that now trades at $80 in New York is $111 in Shanghai. $93 in India. $120 in Japan. And $106 in Kuwait.

That’s a 40% spread between New York and Shanghai — the largest sustained divergence in precious metals history.

The arbitrage is obvious: buy COMEX at $80, ship to Shanghai, sell at $111, pocket $29 per ounce.

Except nobody can do it.

And that fact still tells you everything you need to know about what’s really happening.

Warsh is a fascinating character in the Fed’s history — equal parts Wall Street insider and central banking iconoclast. He served as a Fed Governor from 2006 to 2011, right through the teeth of the financial crisis.

And during that period, he built a reputation as a hawk’s hawk.

While Bernanke was pioneering quantitative easing and slashing rates to zero, Warsh was often the dissenting voice, warning about the long-term consequences of ultra-loose monetary policy. He wasn’t necessarily wrong; many of his concerns about asset bubbles, moral hazard and the Fed’s expanding role proved prescient.

But he was definitely on the restrictive side of the monetary policy spectrum.

Fast forward to 2026, and Warsh has been making the rounds arguing for lower rates. He’s criticised Powell’s hesitancy to cut, called for ‘regime change’ at the Fed, and positioned himself as the candidate who understands that rates need to come down.

Trump loves this narrative — he’s repeatedly called Powell ‘stupid’ for not cutting faster.

But the markets are NOT buying Warsh’s story. Turns out, there is no greater zeal in a convert.

When Warsh’s nomination was confirmed, the market essentially said:

‘We remember the real Kevin Warsh.’

And the real Kevin Warsh, in its assessment, is someone who will talk dovish to get the job but revert to hawkish instincts the moment inflation flares up or financial stability concerns emerge.

But let’s quickly consider the mechanics of the selloff.

First, there’s the interest rate dynamic. When interest rates are low — especially when real rates (nominal rates minus inflation) are negative — gold becomes incredibly attractive. You’re not giving up much yield to own it, and it protects against currency debasement and inflation.

But when rates rise, or when markets expect rates to stay elevated for longer, the opportunity cost of holding gold increases. This is especially true if inflation is under control, which removes gold’s primary value proposition.

Warsh’s confirmation signalled to markets that the Fed might not be as accommodating as hoped. Even if cuts continue in the near term, the terminal rate — the level where cuts eventually stop —could be higher under Warsh than under a true dove like Hassett.

And perhaps more importantly, if inflation resurges (quite possible given Trump’s tariff policies and fiscal spending plans), Warsh is seen as someone who will prioritise price stability over growth.

Second, the dollar surged. Expectations of higher rates attract foreign capital to dollar-denominated assets, strengthening the greenback.

Since gold is priced in dollars, a stronger dollar makes it more expensive for international buyers and reduces its appeal as a currency hedge. The relationship isn’t perfectly inverse, but it’s close enough that dollar strength is almost always bad news for gold in the short term.

Third, the uncertainty premium evaporated. One underappreciated driver of precious metals prices is pure uncertainty. When investors don’t know what’s coming — geopolitically, economically or monetarily — they buy gold as insurance.

The Warsh nomination, whatever its implications, removed one major source of uncertainty. Markets now know who will lead the Fed. That clarity, paradoxically, reduces safe-haven demand.

Finally, technical factors amplified the move. Gold had rallied hard into the nomination news. Leveraged speculators were heavily long. When the selloff started, it triggered stop-losses and margin calls, creating a self-reinforcing cascade.

In precious metals markets, which are relatively illiquid compared to major equity indices, these technical moves can be sharp.

But if you want to see what a genuine market fracture looks like —what happens when the paper-physical divergence reaches its logical conclusion — don’t look at gold.

Look at silver.

Silver has been exhibiting the same dynamics as gold, but on steroids.

Right now, COMEX has 108.7 million ounces of registered silver — metal available for delivery against futures contracts.

Paper claims against those ounces? 1.586 billion ounces.

That’s fourteen owners for every ounce that exists.

In the first week of January alone, 33.45 million ounces were physically pulled from COMEX vaults. That’s 26% of registered inventory gone in seven days.

And then came 30 January.

COMEX silver crashed >30% to $77 — the worst single day since 1980. Forced liquidation as margin requirements obliterated leveraged longs.

The same day, Shanghai Futures Exchange settled at 29,487 RMB per kilogram. An all-time high.

Two exchanges. Same metal. Opposite directions.

In December, silver was trading above $80 in Shanghai while COMEX paper contracts sat at $71-80. That was a $10-20 spread — already extraordinary.

Today? The spread is $31. Shanghai at $111, COMEX at $80.

The arbitrage should be simple: buy COMEX, ship East, pocket the difference minus $1-2 in shipping costs.

Except you can’t pull the metal out. When you try to take delivery at COMEX, you’re discovering there isn’t enough physical silver to move.

The one-month lease rate at 8% makes borrowing metal to cover the trade painful. And even if you could execute the trade, the metal is locked in vaults where registered inventories have fallen to multi-year lows.

Since September’s peak, COMEX silver inventories have dropped 117 million ounces — a 22% decline to just 415 million ounces, the lowest level since March 2025.

After the Warsh nomination, silver crashed in paper terms — COMEX futures getting hammered alongside gold as dollar strength and hawkish expectations crushed sentiment.

But Shanghai prices? Still trading at massive premiums to COMEX.

This is the smoking gun that something fundamental has broken.

In a functioning market, when New York crashes, Shanghai crashes too. Prices converge through arbitrage. The fact that Shanghai is holding 40% premium pricing while COMEX paper collapses tells you that Eastern buyers don’t believe Western paper prices are real.

Friday’s silver crash wasn’t primarily about Warsh or dollar strength. It was margin-induced liquidation at record prices while physical fundamentals continued to tighten.

CME raised silver margins to 11% on 28 January (after shifting to percentage-based calculations on 13 January). Traders who went long when margins were $25,000 suddenly had to post $66,000 when silver hit $120.

If you’re trading on leverage, which most futures traders are, you suddenly need massive amounts of additional cash in your account. If you don’t have it, you’re forced to liquidate. When enough traders hit that wall simultaneously, you get a cascade.

And then CME announced another margin hike for today:

Gold: +33%

Silver: +36%

Platinum: +25%

Palladium: +14%

This is desperation.

When exchanges raise margins this aggressively, this frequently, it signals that a major player is blowing up and they’re scrambling to protect clearing firms.

SHFE premiums exploded to 25% above US prices during the selloff. Physical holders are hoarding while overleveraged paper longs got blown out.

JPMorgan’s February delivery data shows them issuing 633 contracts at Friday’s $78.29 settlement — right at the bottom of the crash.

If JPM covered a large short book during the forced liquidation by buying from overleveraged specs at $78-90, they exited their shorts near the lows while physical holders in China and India refused to sell at any price.

This sets up a dangerous rebound dynamic with far less short interest to cap the next move.

This is the same dynamic that played out with gold in February 2024, when COMEX vaults were being stuffed with tons from London.

Except silver has a critical difference: industrial users can’t wait.

And on 1 January, Beijing reclassified silver as a strategic material. Only 44 companies are now licensed to export. They control 60-70% of global refined supply.

The gate is locked.

Early estimates suggest roughly 35 million ounces — about 25% of China’s 140 million ounce annual exports — will be restricted.

But the most telling signal came from Samsung.

One of the world’s largest semiconductor buyer stopped trusting COMEX entirely. They bypassed the exchange and locked a direct two-year exclusive offtake deal with a Canadian mine for 100% of output.

When the world’s largest semiconductor buyer secures silver straight from the ground, it tells us COMEX has a credibility problem.

Samsung’s move confirms what the Shanghai premiums are screaming: there are two silver markets now. Only one is real.

And it’s not just silver. Amazon signed a 2-year supply contract to directly source copper from a mine that will produce just 14,000 tonnes over 4 years. That’s not even enough to build one large data centre.

This has never been done before. We’ve entered a new era where access to physical resources matters more than money to buy those resources.

Let’s now talk about what just happened from a probability perspective.

Last Tuesday, Japanese 30-year debt recorded a ‘6-sigma’ session — a price move so extreme it should occur once in 500 million observations.

Two days later, silver did even better: 5-sigma on the rally up to $121, then 6-sigma on the crash down to $77. In a single session.

Gold right now? Up 23% in less than a month before the crash. Another near-6-sigma event.

That’s three 6-sigma events in one week across different asset classes.

To put this in perspective: previous 6-sigma events include the October 1987 crash, the March 2020 pandemic crash, the Swiss franc surge in January 2015, and WTI oil turning negative in April 2020.

We’ve never had three such events occur within one week of each other.

6-sigma events are almost never triggered by simple macro headlines. They almost always come from market structure problems —excessive leverage, concentrated positions, margin calls, collateral issues and forced buying or selling.

When you see extreme statistical events days apart in completely different markets — Japanese government bonds (the bedrock of global funding markets), silver (industrial and monetary metal), and gold (ultimate monetary metal) — you’re not looking at isolated incidents.

You’re looking at internal strains in the system’s mechanics.

According to CFTC data before the crash, commercial traders — the big institutions, bullion banks and market makers — were net short approximately 275 million ounces of silver. That’s almost 10% of global annual production.

In normal markets, commercials provide liquidity. They hedge. Prices mean-revert.

But what happens when physical supply is tight, delivery demands are spiking, and Shanghai is paying premiums over your short position?

You get squeezed.

Every silver squeeze in history has ended the same way: commercials get caught short, scramble to cover, prices spike until someone changes the rules.

In 2011, when silver spiked to $49, COMEX raised margins five times in nine days. Margins went from 4% (allowing 25x leverage) to 10% (allowing 10x leverage). The leverage collapse triggered forced liquidation, and silver crashed from $49 to $26 in weeks.

The playbook worked because the squeeze was driven by leveraged speculators.

Today? Margins are already at six times leverage. We’re already tighter than the worst point of 2011. More hikes won’t trigger a 2011-style cascade because the leverage has already been flushed from the system.

So what does the post-Warsh crash actually mean for silver?

In the short term, it’s given commercials breathing room. Dollar strength and hawkish Fed expectations crushed paper prices, allowing some short covering without triggering delivery demands.

But the fundamental problem hasn’t changed at all.

The physical shortage is real. It’s not been resolved by Kevin Warsh’s nomination.

What changed is sentiment. Western paper markets repriced on macro expectations.

But Eastern physical markets? They’re saying the macro narrative doesn’t matter if you can’t actually get metal.

There are only a few ways this resolves:

Scenario 1: Supply Response - New mines open, recycling ramps up, industrial users find substitutes. This takes years, not months. Recycling silver from electronics isn’t economical even at $80. Solar panels have 20-year lifecycles. You want more mined silver? You need more copper mining, which takes years to bring online.

Scenario 2: Demand Destruction - Prices go high enough that industrial users stop buying. Solar manufacturing becomes unprofitable above $100-150/oz. But if that happens, solar panel prices rise, adoption slows, and we’re back to fossil fuels — which have their own supply constraints after years of underinvestment. The entire energy transition reprices.

Scenario 3: COMEX Goes Nuclear - Force cash settlement, eliminate physical delivery, effectively admit that COMEX is a paper market disconnected from reality. This destroys COMEX’s credibility as the global pricing benchmark. Shanghai becomes the real price. Western futures become irrelevant.

Scenario 4: Paper Reprices to Physical - The Shanghai premium doesn’t fade. It expands. Eventually, Western markets capitulate and COMEX prices catch up to physical reality. This could happen overnight during a short squeeze or gradually as the divergence becomes undeniable.

History is pretty clear about which scenario usually wins: paper eventually reprices to physical reality, not the other way around.

But if you believe Warsh will return to his hawkish roots, the Fed is less likely to provide the kind of monetary accommodation that precious metals bulls are counting on. Quantitative tightening might restart. Rate cuts might be shallow and short-lived.

And if the Trump administration’s policies prove inflationary —tariffs raising import costs, fiscal stimulus overheating the economy, immigration restrictions creating labor shortages — Warsh might actually have to raise rates again.

In that scenario, precious metals face sustained headwinds. Real rates stay positive. The dollar stays strong. And the ‘Fed put’ —the market’s belief that the central bank will always rescue asset prices — becomes less reliable.

There’s also a psychological element. Warsh’s appointment suggests that despite Trump’s rhetoric about wanting low rates, he’s willing to nominate someone with genuine anti-inflation credentials.

That implies a degree of policy seriousness that markets weren’t necessarily expecting. It’s not the full capitulation to political pressure under Hassett that would genuinely undermine Fed independence (which would, ironically, be bullish for gold as a dollar hedge).

But short-term price action is one thing. Long-term fundamentals are another. And the long-term fundamentals for precious metals haven’t changed at all.

While retail investors panic-sold on the Warsh crash, institutional voices are saying something very different.

JPMorgan sees gold potentially surging toward $8,000. Their analysis suggests that if private investors increase gold allocations from 3% to 4.6% of portfolios, prices could reach $8,000-$8,500 per ounce. Gold recently hit $5,600 amid safe-haven demand, central bank buying, and a shift away from long-term bonds.

Rick Rule put the current volatility in context:

‘In the 1970s, the gold price fell three times by 30% or more. From 1971-1975, gold increased 6x, from $35 to $200. In 1975, gold fell from $200 to $100. Everyone shaken out at $100 missed the move to $850 by 1980.’

His advice: ‘You have to prepare yourself financially and psychologically for 20-50% pullbacks. You need to know your portfolio well enough that you have the conviction where price declines are opportunities instead of risks.’

And fundamentally, the United States is drowning in debt.

The federal debt now exceeds $38.6 trillion. The debt-to-GDP ratio is above 120%, levels previously seen only during World War II.

And unlike the post-WWII period, when debt was inflated away through strong economic growth and mild financial repression, today’s economy is growing tepidly while debt continues to accelerate.

Annual interest payments on the federal debt now exceed $1 trillion— more than the defense budget, more than Medicare, more than anything except Social Security. And this is with rates that, by historical standards, are only moderately elevated.

The Congressional Budget Office projects that under current law, federal debt will reach 166% of GDP by 2054. But current law is a fiction — it assumes no new spending programs, no wars, no recessions requiring fiscal stimulus, and no major healthcare or Social Security reforms. In reality, debt will almost certainly grow faster.

This creates what economists politely call a ‘fiscal sustainability challenge’ and what everyone else should recognise as a sovereign debt crisis.

The Impossible Trinity

The United States faces three increasingly incompatible objectives:

Maintaining the dollar’s global reserve status (which requires confidence in US fiscal stability)

Servicing the debt at current levels (which requires low interest rates)

Controlling inflation (which requires high interest rates)

You can achieve two of these three. You cannot achieve all three simultaneously.

If the Fed keeps rates high to control inflation, debt service costs explode, requiring either massive spending cuts (politically impossible), massive tax increases (economically damaging and politically unpopular), or debt monetisation (printing money to pay bills, which destroys currency value).

If the Fed cuts rates to make debt serviceable, inflation risks resurging, especially with Trump’s tariff policies and fiscal expansion plans. Inflation is already a hidden form of default — it reduces the real value of debt, but it also destroys purchasing power and undermines confidence in the currency.

And if confidence in US fiscal stability erodes, the dollar’s reserve status comes into question. Foreign central banks hold dollars because they trust the US will honour its obligations.

If that trust wavers (if holding US Treasuries starts to look like holding Turkish lira or Argentine pesos) demand for dollars collapses, triggering a currency crisis that makes current inflation look quaint.

There’s a concept in monetary economics called ‘fiscal dominance’ —the point at which government debt becomes so large that fiscal policy (taxing and spending decisions) constrains monetary policy (interest rate decisions).

The United States is approaching this threshold.

Kevin Warsh might want to be tough on inflation. He might intellectually believe in sound money and Fed independence. But when Treasury auctions start failing because international buyers balk at yields, or when interest costs consume 30% of the federal budget, or when a recession hits and unemployment spikes while the government lacks fiscal space to respond, the Fed’s hand will be forced.

At that point, there are only two options: accept a deflationary debt collapse (think 1930s-style depression), or print money to prevent it.

History suggests which path he will choose.

While US fiscal dynamics are concerning, they’re not unique.

Japan’s debt-to-GDP ratio exceeds 260%. Many European countries are above 100%. China is facing a demographic implosion and a property sector collapse that will require massive government intervention.

The developed world, collectively, has made promises it cannot keep— in pensions, healthcare and social programs — without either dramatically raising taxes, slashing benefits or inflating away obligations.

This is a structural driver for precious metals that transcends any single Fed chair’s philosophy.

Central banks understand this dynamic, which is why they’ve been accumulating gold at the fastest pace in decades.

And speaking of dollar dominance being questioned: Chinese President Xi Jinping recently called for the Yuan to become a global reserve currency.

China has been systematically working to internationalise the yuan, establish bilateral trade agreements that bypass the dollar, and build alternative payment systems to SWIFT.

The reclassification of silver as a strategic material fits into this broader framework. So does China’s record gold accumulation by its central bank.

Meanwhile, tension is exploding in the Strait of Hormuz. Iran has launched military drills in the world’s most critical oil chokepoint. The US has issued warnings that this is a massive escalation and any miscalculation could trigger full-scale conflict.

When 20-30% of global oil flows through a single strait, and that strait becomes a potential conflict zone, energy prices become unpredictable. If oil spikes, inflation follows. If inflation spikes, the Fed’s hands are tied — they either accommodate it (dollar negative, metals positive) or fight it (recession risk, crisis metals positive).

Geopolitical instability doesn’t create linear outcomes, and as I said at the start, Hormux will remain open. But even a tiny chance it closes, and the risk premium rises.

Here’s how to think about positioning (not advice, as ever):

For traders: The Warsh selloff might have further to run. Markets often overshoot in both directions. If you’re trading on short-term momentum, there’s no shame in stepping aside and waiting for clearer signals. Watch for stabilisation, for the dollar to peak, for real rates to start declining again. For silver specifically, watch the Shanghai premium — if it widens while COMEX falls, that’s your signal that physical reality is diverging further from paper fiction.

For investors: If your time horizon is measured in years, not weeks, this is noise. The structural case for precious metals —unsustainable debt, fiscal dominance, monetary instability, geopolitical fragmentation and genuine physical shortages — hasn’t changed at all. Dollar-cost averaging into weakness is rarely a bad strategy for assets with genuine fundamental support. The silver situation suggests that physical metal (not paper ETFs or futures) might be particularly important if you believe the fractional reserve system is genuinely breaking.

For sceptics: If you think gold is just a pet rock and fiat currencies will reign supreme forever, nothing I’ve written will convince you otherwise. But ask yourself: do you really believe the US can run trillion-dollar deficits indefinitely without consequences? Do you believe interest costs can triple without forcing policy changes? Do you believe emerging powers will happily finance American consumption forever? And do you believe COMEX can conjure 275 million ounces of silver to cover commercial shorts when industrial users are hoarding and Shanghai is paying premiums?

If the answer to any of those is no, you should probably own some gold. And maybe some silver too.

The Shanghai premium persisting through the Warsh crash is a powerful signal. If you’re accumulating precious metals for long-term wealth preservation, the case for physical ownership (or at minimum, allocated storage with full title) has never been stronger.

Paper claims on metal only work if the paper can actually be converted to physical when you need it. The silver market is demonstrating, in real-time, that this assumption might be dangerously optimistic.

Here’s the final twist: Kevin Warsh might actually end up being good for gold, just not in the way bulls initially hoped.

But first, let’s talk about what actually happened with the Warsh nomination — because the narrative isn’t as simple as ‘hawkish Fed chair = bad for metals.’

Trump positioned Warsh as an independent inflation hawk who will pursue tighter monetary policy than Powell. That’s the public narrative.

But look closer at what Warsh has actually been saying.

Three months ago on Fox Business, Warsh stated:

‘It was the President’s policies that brought inflation down, not the Fed’s keeping interest rates high.’

Warsh believes the Fed was too late to hike in 2022 and too late to cut now. He’ll likely deliver aggressive cuts initially, but he isn’t someone who will condone high inflation to keep rates down and deliver growth at all costs.

Stan Druckenmiller — Warsh’s partner in Duchesne Capital and legendary for his ‘go big and go for the jugular’ mentality — said this about Warsh:

‘The branding of Kevin as someone who’s always hawkish is not correct. I’m really excited about the partnership between him and Bessent. Having an accord between the Treasury Secretary and Fed Chair is ideal.’

This is my view: Trump falsely positioned Warsh as a hawk.

That way, when Warsh does exactly what Trump wants him to do — cut rates aggressively —the markets will assume rate cuts are economically justified.

Trump said explicitly:

‘Kevin Warsh will cut rates without any pressure.’

Warsh believes that the AI boom and innovation revolution will create long-term disinflation, which will bring sharply lower rates. He has also stated repeatedly that economic growth does not cause inflation.

And make no mistake. Treasury Secretary Scott Bessent is behind this appointment.

Why Warsh?

Credibility.

The goal is to restore the Fed’s legitimacy, which has been shattered over the last 15 years. Since 2008, the Fed became the market’s guardian angel — injecting liquidity the moment things got scary, protecting asset prices.

Warsh is the biggest critic of this model. His view is simple: if a market cannot correct, it’s not a market.

Appointing him sends a massive signal that the Fed is returning to its core mandate: inflation control, banking stability and no more automatic market bailouts.

But Trump thinks in terms of power. He wants technological domination and reindustrialiSation. He needs low rates to finance it.

The likely outcome isn’t war between the Fed and Trump. It’s informal coordination.

But there’s a red line: if inflation rips higher, Warsh will have to choose between institutional credibility and political loyalty.

December PPI inflation came in at 3.0%, above expectations of 2.7%. Core PPI inflation unexpectedly rose to 3.3%, above expectations of 2.9%—the highest level since July 2025.

Month-over-month, PPI was 0.5% versus expectations of 0.2%. Core PPI was 0.7% versus expectations of 0.2%.

This is the data environment Warsh will inherit. If he genuinely believes the Fed was too late to hike in 2022, and if inflation continues running above target, his historical hawkish instincts could resurface regardless of Trump’s preferences.

The market’s initial reaction — selling precious metals on hawkish expectations — might not be entirely wrong about Warsh’s potential policy path, even if it’s wrong about the timeline.

If Warsh genuinely tries to maintain hawkish policies in the face of unsustainable debt dynamics, one of two things happens:

Scenario 1: He succeeds in keeping rates high and inflation low. But this causes a debt crisis or severe recession, forcing a policy U-turn. Markets lose faith in the Fed’s ability to maintain tight policy, which is ultimately bullish for gold as a hedge against policy failure.

Scenario 2: He fails to maintain hawkish policies because political pressure, economic weakness, or fiscal reality forces accommodation. This vindicates the thesis that fiscal dominance has already arrived, which is extremely bullish for gold as a hedge against monetary debasement.

In other words, Warsh either proves that sound money is still possible (but at the cost of severe economic pain that still benefits gold), or he proves that sound money is impossible given current debt levels (which is even better for gold).

The only scenario where gold loses long-term is if Warsh threads an impossibly narrow needle: keeping inflation low, growth stable, markets calm and debt sustainable, all while maintaining Fed independence and dollar credibility.

That’s a lot of needles.

Markets are forward-looking mechanisms, but they’re also manic-depressive entities prone to overreaction.

The precious metals selloff on the Warsh nomination is a classic example of markets pricing in near-term policy expectations while ignoring structural realities.

Yes, Warsh might be less dovish than hoped. Yes, rate cuts might be shallower or shorter-lived.

And yes, the dollar might keep up the charade for a while longer.

But none of this addresses the fundamental problems:

The United States has a debt trajectory that is mathematically unsustainable at any plausible combination of growth rates, interest rates and primary budget balances.

And the physical precious metals markets are experiencing a fractional reserve breakdown that paper price crashes cannot resolve.

At some point, something will break. Either inflation surges as the Fed accommodates fiscal excess, or deflation crushes the economy as the Fed tries to maintain orthodoxy, or the dollar’s reserve status erodes as foreign creditors lose confidence, or the paper markets admit they cannot deliver physical metal.

In every one of those scenarios, precious metals matter.

Stock Rundown

Okay, now the macro’s out of the way, let’s have a look at our 2026 picks.

Conviction Plays

Amaroq - the Nanoq video was awesome, and Minturn’s 69.5% iron grades across 9km of strike was also good news. Gilberton noted that

‘Greenland has the geological ingredients to host truly elephant-scale mineral systems. The identification of what appears to be a Kiruna-style IOCG project, underpinned by extensive iron oxide alteration and very high iron grades at surface, represents a significant strategic step for Amaroq.’

But it’s as ever the macro which pushed up the share price - both rising gold and Trumpian madness. I am convinced now that hundreds of millions of dollars and euros are going to enter the mining industry on the island, and when it does, only Amaroq will be capable of using this capital.

The are the only ones with the expertise.

Eldur even told CNBC that discussions were underway about potential American involvement in Amaroq’s operations, including long-term metal purchase agreements, infrastructure assistance and access to credit.

This is a long-term game.

Sovereign Metals - the discovery of heavy rare earths at Kasiya adds yet another string to the bow, and also explains why the IFC (World Bank) was so keen to get involved.

In the company’s own words:

‘Preliminary analysis confirms Kasiya monazite to contain exceptionally elevated levels of heavy rare earth elements Dysprosium - Terbium (DyTb) and Yttrium, materially exceeding those of the five largest producers globally, which account for 70% of the world’s rare earth production.’

The MRE upgrade and World Bank -standard DFS are both scheduled for this quarter.

Then the clock starts ticking and a buyout for the world’s largest rutile resource lands before the year is out.

GreenX - Singapore has dismissed Poland’s application to set aside the ECT award.

The judgment will matter enormously in regards to the BIT award in England as well - Singaporean and English law are very close in nature.

Basically, that’s it. Poland’s lost.

GreenX will return slightly more than its market cap to investors in due course (Poland can keep trying but this is over, barring a significant black swan).

The company did (perhaps opportunistically, but at a good price), raise A$13.6 million later in the month, with a very tight book of solid institutional investors.

Remember, Tannenberg which in my view may well become a Tier 1 copper resource, is currently being ascribed zero enterprise value by the market.

This will change.

Buyout Plays

Helix - We’re waiting for production. It’s coming, along with offtakes. While I didn’t think it would take quite this long (did they mean an Australian summer?), we are at the finish.

Hold the line.

Asiamet - Norin has submitted all material needed for Chinese regulatory approval for KSK, and expects this to be confirmed by the end of February. Beutong, ARS says it is ‘committed to advancing the optimal pathway for Beutong and has resumed discussions with the relevant authorities.’

In other words, Beutong will be sold too. I expect a payout of circa 3p per share later this year (remember to keep your shares as well because the shell will likely be used.

Guardian - is prepping for its US listing. Given the movement on the OTC, US investors are desperate to get hold of shares before then (and UK investors aren’t selling them).

The longer-term story of tungsten pricing has proved correct - it just keeps going up. And whatever competitors might say, GMET is much further along the path to production at both assets.

With Warsh in the White House, and Stan the Man a material shareholder, something big may be coming down the line.

Those stockpiles aren’t going to stockpile themselves.

Blencowe - is advancing Orom-Cross. The company has secured a Letter of Intent with Italian processor Alkeemia for toll purification services, providing a non-Chinese processing route that can achieve 99.99% purity — the highest commercially recognised grade. It’s already an exclusive natural flake graphite supplier to the EU’s €100 billion SAFELOOP energy transition program.

Recent drilling results from two newly discovered deposits — Beehive and Iyan — demonstrate the scale and continuity, with multiple intercepts exceeding 90 metres at high grades (6-7% TGC). Both deposits show thick, near-surface mineralisation from surface to 30+ meters depth, with many holes ending in mineralisation, indicating significant depth potential.

Afentra - has announced a significant 400% increase in its 2C working interest contingent resources to 87.3 mmboe across Blocks 3/05, 3/05A and 3/24 in Angola.

This follows an independent audit by Sproule ERCE certifying 36.6 mmboe across existing discoveries including Bufalo Norte, Punja, Gazela and Caco, plus an internal assessment of the recently awarded Block 3/24 adding a further 37.0 mmboe.

The planned 2026-2027 programme includes up to two infill wells and three workovers in the Palanca field, targeting production uplift of up to 12,500 bopd gross and reserves exposure of approximately 120 mmbbo gross, with net capex of $34-39 million.

The company is also fast-tracking development of Block 3/24 discoveries with a target Final Investment Decision in Q4 2026.

Fundamental Plays

Power Metal - Tati is getting there, but the real story is share buybacks. Retail interest remains low but the NAV compared to the market cap remains ridiculous, so continued buybacks are justified - and the share price will simply grind higher.

African Pioneer - raised £1.8 million at 0.9p. A placing came to nobody’s surprise, but this is good news as it sets the stock up for a BZT-style rise for Ongombo in 2026. The parallels are obvious.

Jubilee Metals - received the second cash installment of $10 million from the sale of the SA assets. The market is now finally starting to reflect its new financial reality, but we await material news out of Zambia to push it higher.

Produce & Expand:

Xtract Resources - We need NEWS. That’s it really. Waiting to see what’s cooking.

Switch Metals - is advancing the Issia tantalum project with approximately 40% of bulk samples processed through the pilot wash plant, keeping the maiden mineral resource estimate on track for this quarter.

This district-scale project spans 1,015 km² and is strategically positioned to address global supply concerns, as 60-70% of tantalum currently comes from the DRC and Rwanda.

Switch has also announced a significant lithium discovery at Issia, named ‘Kabore,’ found during pitting work near a tantalum-rich area. Grab samples returned lithium oxide grades between 1.00% and 2.58%, while the same location revealed high-grade coltan occurrences (82% tantalum), demonstrating the pegmatites’ dual potential for critical metals.

This will rise.

Alien Metals - a welcome management change and the Munni Munni transaction finalised. This remains fundamentally undervalued and will re-rate. Possibly needs an updated article, will try to get out this month.

Bezant - Ticking along. Needs news as well, though all seems fine at the coal face.

Arbitration Plays

Zenith - Article coming.

Exploration Games:

Rome Resources - has provided positive updates on Bisie North, reporting progress from its post-maiden resource drilling programme.

Two rigs are currently operating at the Mont Agoma and Kalayi prospects, with early results from Kalayi hole KBD019 showing encouraging tin mineralisation — a 6-metre zone averaging 1.6% tin within a broader 26-metre mineralised interval. At Mont Agoma, drilling continues to target deeper parts of the system where tin grades are expected to strengthen alongside the known near-surface copper mineralisation.

Initial metallurgical testing has delivered promising results for commercial recovery potential as well. Tin ore responded well to gravity pre-concentration, recovering 80% of tin into a concentrate grading over 10% from a head grade of just 0.6%. Copper results were similarly encouraging, with 96% copper recovery through gravity methods and 95.5% recovery via flotation at 9.5% grade.

Ajax Resources - raised another £1 million. You know what? Get liquidity while it;s there at decent terms. This will be a long-term winner.

Arc Minerals - Remy’s presentation brought some fire to the investment case. Good to see. Yes, the court cases continue to drag - but the copper is still there and isn’t going anywhere. Look at comparable copper explorers in that part of the world and you can see the attraction.

Botswana is looking promising and the recovery potential remains strong.

Moonshots

AFC Energy - I had a great chat with Nick, their head of strategy - and think the company is on strong hands. It’s now successfully completed the first build of its new LC30 30kW liquid-cooled fuel cell generator, which is now undergoing operational testing as we speak, and producing power to specification.

The company has exceeded its cost reduction target, achieving an approximately 85% decrease in manufacturing costs compared to the previous air-cooled model, surpassing the original 66% reduction goal, while delivering the unit on schedule and under budget.

The LC30 Generator offers substantial improvements including a 50% mass reduction, 45% smaller volume, up to 20% greater efficiency, 95% fewer components and an expanded operating temperature range from -20°C to +50°C, making it suitable for global deployment.

The design also accommodates scaling up to a 100kW fuel cell in the same chassis, positioning AFC Energy to pursue cost parity with diesel generators, convert pipeline opportunities into orders, and drive sustainable revenue growth.

Just keep plugging on.

Defence Holdings - appointed Jim Clover OBE, who served as Deputy Director of Cyber Operations within HM Government, to the board.

The company is now a heavy hitter in terms of personnel, but we need a contract, even if initially small in £ terms, to prove the commercial viability.

I don’t think anyone can complain about the volatility in the share price - we all know what small caps are about - but equally, ALRT has had enough time to build and deploy. Get some revenue and this flies back up. I remain a long-term believer.

Solvonis - has received a Notice of Allowance from the USPTO for compounds within its SVN-SDN-14 PTSD discovery programme, strengthening the intellectual property ahead of lead candidate selection expected in Q1 2026.

The patent covers novel serotonin, dopamine and noradrenaline modulators designed to support pro-social engagement and enhance psychological therapy effectiveness in PTSD patients.

The compounds address historical development challenges by incorporating predictable metabolic deactivation to improve pharmacokinetic control, dosing flexibility and safety margins while maintaining therapeutic activity. The USPTO examiner confirmed the novelty of the approach, finding no existing patents or publications disclosed the claimed compounds.

The company has also expanded its SVN-015 programme into depression following positive preclinical data showing antidepressant-like activity comparable to fluoxetine (Prozac) after 14-day dosing in validated rodent models.

SVN-015 is a novel Serotonin-Dopamine Reuptake Inhibitor designed to address symptoms poorly controlled by SSRIs, including anhedonia and reduced motivation, targeting a market of over 20 million adults with Major Depressive Disorder in the US alone.

The compound is being developed as a once-daily oral therapy for at-home use aligned with standard antidepressant treatment cycles, and has separately been selected for evaluation by the US National Institute on Drug Abuse for stimulant use disorders, providing independent validation of its pharmacological profile.

This remains an exceptional pharma play.

Immupharma - we need P140 commercialisation, but like a few others on this list, a general update as well. Remember, these are picks for 2026, not January. Deal-making takes time.

United Oil & Gas - the ship is on the move and made national Jamaican headlines. Get CoS to just 1 in 3 on Colibri, sign an earn-in on a $50 million drill, and watch the price rocket. Get it done!

Stallion Uranium - I did say uranium would be the best performing commodity of 2026. It’s good to see my theses work out.

Stallion is actively advancing its winter exploration program at the Coyote Target on its Moonlite Property in Saskatchewan’s Athabasca Basin, mobilising drilling equipment to test high-priority uranium targets identified through integrated geophysical surveys.

A recently completed ground electromagnetic survey identified nine discrete conductors, including six strong conductors exceeding 10 Siemens, which show structural complexity and offsets interpreted as favorable for uranium deposition. These conductors occur within a broader gravity-low anomaly, suggesting enhanced structural disruption that could indicate uranium mineralisation potential.

To further refine drill targets, Stallion is expanding its high-resolution ground gravity survey westward along the Coyote corridor to better define alteration-related density lows that remain open at the edges of previous survey coverage.

The company is also conducting an airborne VTEM survey over its Stone Island Target. These systematic exploration efforts aim to identify multiple uranium systems along the structural trend, similar to discoveries in the Patterson Lake corridor.

This will win big, trust me.

The Final Word

We have Halo coming to the market this quarter, and I think adding Aterian and Andrada to this list in Q2 may make a lot of sense.

I was previously thinking monthly changes but it will become too hard to track.

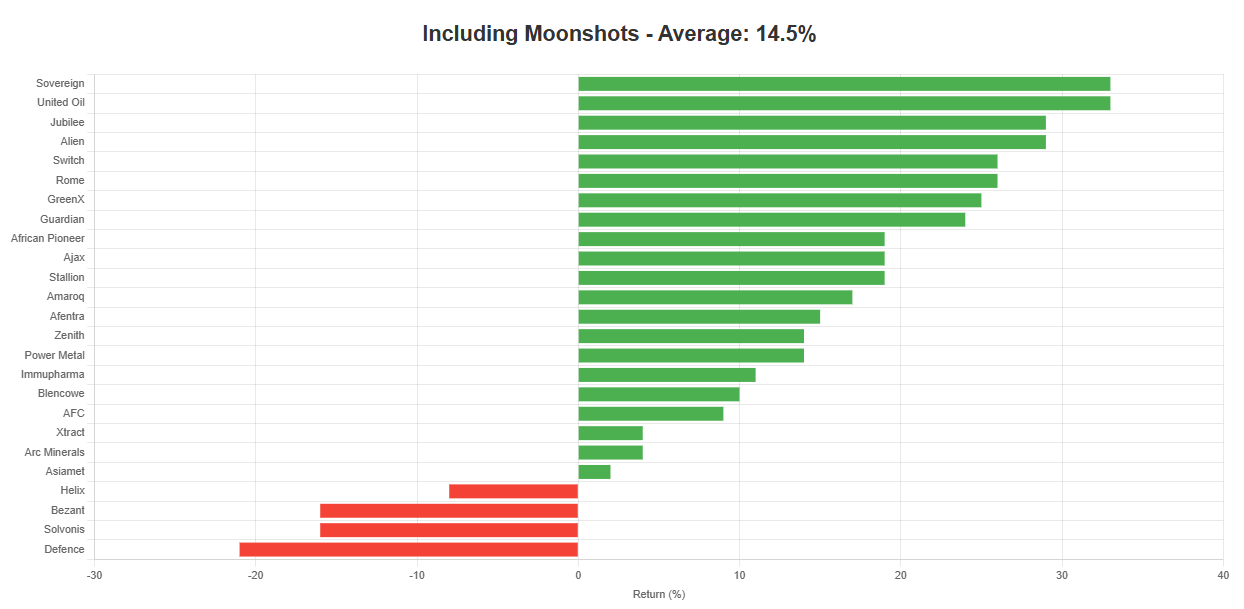

We’re looking at a 14.5% return across the month (Yahoo Finance data) - and 15.9% when you exclude the Moonshots - these are more volatile positions and is to be expected.

Possibly the takeaway here for Helix, Bezant and Defence is news. The market needs news like a plant needs oxygen.

You can have a great investment case but if you aren’t constantly telling the market new things, your share price will fall.

The good news is that when news lands, these three should all turn positive.

Solvonis is a head-scratcher. It should be continually rising and it’s not. The news flow is strong and the investment case solid - it’s looking very good value and I’ll be picking up a few shares on this discount over February.

Everyone else is behaving as expected - plenty of catalysts to come for everything on this list.

In terms of trading ideas - of the US stocks, Figma has fallen about 30% and Kraken’s up about 30% - the remainder are basically flat.

I’m staying in all positions and not selling nor buying.

The only thing I’d keep an eye on for February is Iran. The US has troop movement in the region and it remains a Sword of Damocles over the markets.

If this month has taught you anything, it should be the dangers of leverage and the importance of portfolio diversification and risk management.

Those who simply bought physical metals can wait for the price to rise back up. Those trading a 3x ETF on 5x leverage got burnt - and deserved it.

Otherwise, have a great month and I’ll see you back here very soon.

Amazing detail. Looking forward to having a subscription to reward your efforts.

Thanks for the great update….. you’ve made a really strong start to the year!!