Small Caps: April Review

It's not all fun & games.

Good Morning Team.

I thought I’d start by telling you about one of my three dogs. His name is Mushu (after the dragon/lizard? in Disney’s animated Mulan).

Mushu is six years old.

Mushu is, by all accounts, a lovely, kind animal. He’s great with children, gets on with the other dogs, and the cats, loves his walks and is basically everything you might want when providing pets for your family.

However.

Mushu is also insatiably greedy.

If you gave this dog unlimited kibble, he would gorge himself to death within a matter of hours. We have taken him to the vet specifically for this issue, and have been repeatedly told after many expensive tests that he is simply a gluttonous chonker.

This week, he managed to get into the kitchen bin and eat, well, everything he could get his grubby paws on. While in no immediate danger, the subsequent 48 hours were not pleasant for him or for me.

And despite my best efforts, he has continued this scavenging behaviour since we picked him up from my Aunt at eight weeks old, and shows no signs of stopping.

He has zero impulse control.

And yet, he’s smarter than Donald Trump, a man who also sports zero impulse control sparked by insatiable greed.

The only difference is that the dog has redeeming characteristics.

And better hair.

You see, the problem with a person with the same intelligence levels of a slightly-below-average-IQ Cavapoo, is that trying to apply logic or fundamental analysis to their decision-making is like trying to reason with a dumb animal that has vomited on the kitchen floor for the third time in the space of an hour.

It’s pointless.

Trump has no logical plan.

The silver lining is that the market is taking less notice of his mad Truth Social posts.

Result.

The big orange monkey has never picked up a history book (possibly because he’s illiterate), so isn’t able to comprehend that he’s started his own forever war in the Middle East. Historically, these have not gone well for the United States.

Iran has used their most powerful weapon in choking off the global economy by shutting the Strait, and the results - even if it were to open up tomorrow - are disastrous.

Add in the infrastructure damage already done and to be suffered, and we’re in deep shit.

Trump can either suffer a humiliating withdrawal, or attempt to organise some kind of ground invasion that involves capturing vast swathes of the Iranian coastline.

Because in a world of drones and mines, that’s what it’ll take to keep the Strait open by force. Having taken the near-nuclear option and closed the Strait, Iran now cannot back down.

Neither of these options are acceptable to his Ego, so he’s telling nations affected to ‘Go get your own oil.’ And threatening to pull out of NATO. And stop funding Ukraine.

What a dick.

The good news though is that I am certain the Strait will be open in the near future. The damage done by keeping it closed is cataclysmic to every economy. Nobody can survive this intact, and it is in nobody’s interest to keep it closed - including Iran.

But how it gets opened is another question altogether.

Others have done far more analysis than me so I won’t bore you with the details.

But a few things leapt out at me this week - Airgas has declared force majeure, cutting customer supply by up to 50%. Egypt has implemented electricity curbs and ordered shops to close early, South Korea is enforcing some driving restrictions, Thailand diesel prices are rising, Japan is seeing significant stock market falls, some flights are starting to be cancelled in Europe as we’re basically on the verge of running out of jet fuel…

Things aren’t broken yet, but the cracks are showing.

And Powell, the last remaining adult in the United States (who is also leaving us shortly) has as all but stated that the Federal Reserve’s tools have no meaningful effect on these shocks.

In other words: You cannot print oil.

Or bananas.

But I would also note that there are some extraordinary bargains in both the small cap and larger spaces for long-term investors seeking an entry - in particular within a SIPP with a multi-decade time horizon.

Just look at Microsoft. The stock is trading at its lowest forward P/E in a decade relative to the S&P 500, and those products are going precisely nowhere.

Likewise, if you’re riding high on oil futures - no shame in taking profits and de-risking. Oil might end up going to the moon, but there’s a difference between eating well and overeating.

As Mushu can attest.

One final note: the tax year is ending very shortly. Among other things, ISA allowances operate on a use-it-or-lose it basis, missing tax deadlines comes with penalties, and making use of your SIPP if you’re in the insane >£100k tax trap can be incredibly tax efficient.

Many readers here spend an extraordinary amount of time attempting to time the market, but ensuring you use your allowances (and in particular, the ISA, whose combination of flexibility, accessibility and tax advantages are essentially unmatched anywhere in the world), is equally if not more important.

For some, this is a case of taking a few days to understand your own financial position. For others, it’s an email chain with your accountant, and for a few, it’s a one-on-one meeting with an IFA.

Which I am not.

In a world of mass redundancies, caused by a toxic cocktail of AI and a potential recession, you cannot afford not to invest, even if in boring, stable low-risk assets.

That is advice.

Oh yeah, also, lots of people plough capital into small caps on 6 April with their new allowances.

It often pays to wait a day or two.

Let’s dive in.

Small Caps Review

Here we go again.

As noted last month, the macro is driving these valuations more than the micro, so we do need to take a pinch of salt with the results here.

If the war ends tomorrow, the whole portfolio will rise.

That being said.

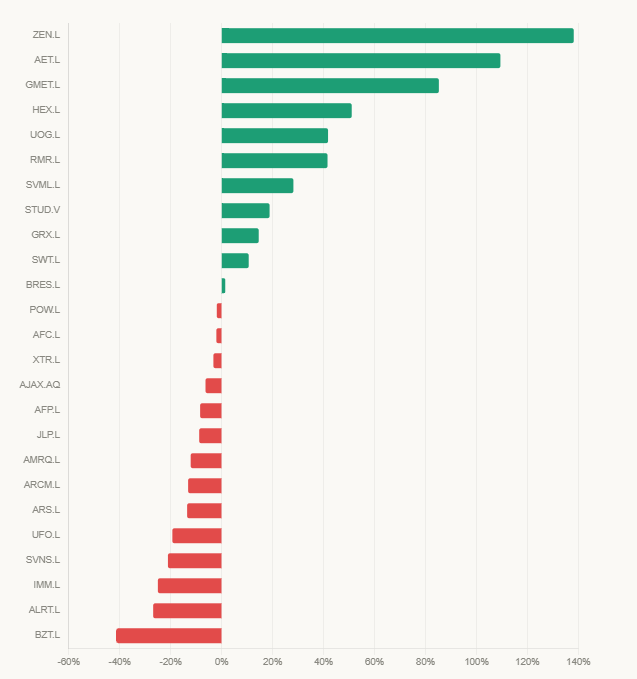

We’re still up +13.5% as a mean (as of yesterday close). For reference, the portfolio was up +25% as a mean at our last review a month ago.

This is a great result given the S&P 500 is down >6% and also a good reminder of why diversification matters. It’s also important to see the context here; the bottom has not fallen out of the market just yet. It’s entirely possible this fall is a blip in the year.

But it can be almost entirely laid at Donald’s feet. Last month we only had three stocks down - and now half the portfolio is in the red (though several only barely).

But consider that Solvonis, Immupharma and Defence Holdings are three of the four biggest losers - and that as moonshots, they could release one decent RNS tomorrow and could flip positive. Likewise, Arc could flip if the legal cases are resolved, and Asiamet on a conclusion of asset sales.

There’s a lot of red there that’s not in permanent market.

Anyway, let’s run them down.

Conviction Plays

Amaroq just published its full-year 2025 results. After years of development spending, the company generated $27 million in revenue from gold sales in 2025 — its first year of real production at Nalunaq.

It hit full-year guidance of 6,000–7,000 ounces, ending the year with 6,350 ounces produced, a solid debut for a mine that was still being commissioned through much of that period.

Nalunaq moved to a fully owner-operated model in October 2025, cutting out contractors and taking direct control of underground mining — a shift that management says immediately improved productivity.

Phase 2 of the mine, a flotation circuit that should push gold recoveries up to 90–95%, is on track to come online in Q2 2026.

That’s the unlock the market will be watching: once Phase 2 is running, full-year 2026 production guidance jumps to 25,000–35,000 ounces — roughly a five-fold increase on 2025.

Drilling at the Nanoq gold project confirmed high-grade hits at shallow depths, and the recently acquired Black Angel zinc-lead-silver mine has thrown up a bonus: potentially commercial levels of germanium and gallium, two critical minerals the US government

On the financial side, the company is doubling its revolving credit facility to $70 million and working to raise $20–35 million in equity for its logistics subsidiary, Suliaq, with Denmark’s state investment fund EIFO expressing preliminary interest.

The balance sheet tightened over Q4 2025 — cash fell from $55 million to $21.5 million — but with production ramping and the expanded facility incoming, management appears comfortable with the trajectory heading into 2026.

As I’ve said repeatedly for years now, the re-rate here comes in H2 2026.

In the words of Anika Noni Rose, we’re almost there.

Sovereign Metals

Two key pieces of news from Sovereign in March.

First, the resource upgrade. Measured and Indicated rutile resources at Kasiya have jumped 32% to 16.1 million tonnes of contained rutile — and the project has achieved a Measured Resource classification, the highest confidence tier under the JORC code.

That matters because IFC bankable feasibility studies usually require this level of resource confidence, and the first six years of planned mining operations are now underpinned by measured material. The total resource sits at 2.1 billion tonnes, cementing Kasiya’s position as the largest natural rutile deposit on the planet.

The DFS is the next big catalyst to watch - potentially this month.

Then there’s the Mitsui offtake MOU. The Japanese trading house has agreed a non-binding framework to purchase up to 70,000 tonnes per year of Kasiya rutile concentrate over an initial four-year period from first production.

Japan is the world’s second-largest titanium metal producer and the dominant supplier of titanium to the United States, and natural rutile is the critical feedstock for that entire supply chain.

With China controlling much of the global rutile market, Kasiya’s significance to Japan — and to Western supply chain resilience more broadly — is hard to overstate.

Sprott has taken some off the table - it’s worth noting if a Sprott investor wants to chicken out, sell and move on (possibly due to the Iran war) Sprott has to sell regardless what the fund managers think.

They will live to regret this.

GreenX managed to get Poland to slightly crack open their dusty wallet for a cheeky A$1.6 million payment to cover legal costs incurred in defending Poland’s failed ECT set-aside motion.

LOL.

The company is now preparing for enforcement activities of the ECT award. If Poland would just get that it’s game over, this could be so much easier.

This was taxpayer money effectively handed straight over to GreenX’s legal team for no benefit to either party whatsoever - and if I were a Polish citizen, I’d be a tad miffed.

Buyout Plays

Helix - the most important news is that they expanded their strategic footprint at Rudyard to nearly 8,000 acres through the acquisition of additional State of Montana mineral leases at public auction last month.

The acquisition extends the company's control over the core of the Rudyard Anticline, the structural heart of the proven helium accumulation.

There is a very real, very scary helium supply crisis and spot prices are going bananas. Even if Hormuz opens tomorrow, the infrastructure has been hit hard - and supply chains are going to need to be diversified in case it ever happens again.

Just read what’s already started:

Sign an offtake, get sales going. The numbers are excellent. Just do it!

The ball is very much in our court.

Asiamet. If it takes a lifetime, I will wait for you… No sweat. This stuff takes time and while the share price drifts lower, the BKM cheque will land sometime in 2026, so as long as that happens, it feels like free money.

Guardian has launched its US listing and now US money is flowing in. $60 million was raised in additional capital, which alone is more than enough to get Pilot Mountain up and running.

Of course, we will now likely see further significant government support.

There is no tungsten for sale anywhere in the world, and the US needs a lot of it. That’s literally the entire investment case and has been my thesis since GMET’s baby IPO. The situation has only worsened since.

I am sure we are all happy to welcome Jake Mather as Chief Financial Officer, a strong appointment for this new trajectory.

However, I would like to personally thank Ben Hodges (who is stepping down as CFO but remains as a non-exec); while Oliver rightly gets a lot of credit, the reason why the rise has been possible is because capital has been raised the right way every time.

Ben would have been instrumental in this, and I wish him every success going forward.

We shall see new highs soon.

Blencowe reported a maiden JORC resource for Iyan, a recently discovered deposit within the wider project. At 16.9 million tonnes grading 6.0% total graphitic carbon, it’s a decent addition — and pushed the total Orom-Cross resource up 66% to 43 million tonnes.

That’s a substantial jump for a single drilling programme, and the mineralisation remains open along strike and at depth, meaning the number could grow further.

We also saw early results from Beehive — the other new discovery being drilled up. Multiple intercepts of over 30 metres from surface, with standout holes hitting 10.78% and 9.46% TGC respectively.

Near-surface, thick, high-grade mineralisation is exactly what you want for a bulk-mineable open-pit operation, particularly one close to planned processing infrastructure.

Only 35 of 110 holes have reported so far, with further batches moving through independent verification — so more newsflow is coming.

This should help with those ongoing financing talks.

Afentra is getting bought out as expected.

£1.20 a share please.

Corcel will be next.

Fundamental Plays

Power Metal announced a $1.5 million strategic investment for a 4.6% stake in Greyridge Exploration, a Canadian company holding 25 exploration licences covering over 1,800 square kilometres in Saudi Arabia.

Alongside the investment, Power signed an MoU giving its subsidiary Power Arabia a framework to pursue joint ventures across Greyridge’s portfolio, targeting copper and gold in one of the world’s last largely untested geological frontiers.

Two weeks later, Power Metal turned its attention to Chile, committing $1 million for a 2.6% stake in Next Minerals, a copper developer with a mine-ready underground project in Antofagasta.

The Comahue mine has its permits in place, detailed engineering complete and a phase 1 resource of nearly 10 million tonnes at 0.81% copper — with a projected seven-year life of mine and $140 million in EBITDA. Power Metal invested alongside Swift Mining Services for a combined $3 million injection.

Then the company announced the start of maiden drilling at East Hawkrock in the Athabasca.

The 2,500 metre diamond core programme is targeting a 6km conductive corridor with radon signatures described as far above those seen at other major basin discoveries. It runs concurrently with a separate 2,100 metre drill programme at Badger Lake — uranium, copper, and gold across three continents in under a month.

There is just so much going on here, and the market refuses to recognise it.

This cannot last forever.

African Pioneer. No news. Can’t write something new if no news. Hold fire.

Jubilee Metals secured an additional parcel of high-grade copper ore at 1.65% copper for Roan, paying $1.8 million in shares rather than cash.

On the Large Waste Project, the seller also opted to take the next $2.6 million installment in shares, leaving $5.4 million outstanding on the acquisition.

Two joint venture partners are shortlisted to help upgrade and refine the 240 million tonne surface stockpile, with discussions expected to conclude within two months.

It’s possible the sell-off is these shares being sold. I hope not, but I am happily a buyer down here.

Drilling at the Molefe open-pit mine has returned strong results, with peak intercepts including 16 metres at 8.01% total copper from 18 metres depth — shallow, high-grade oxide mineralisation well-suited for processing at Sable.

Infill drilling confirmed grade continuity in line with the existing mine plan, while a new zone extending roughly 250 metres beyond the planned boundary was identified, with mineralisation still open to the east. Phase 2 drilling with partner Galileo is now underway to chase that extension.

The updated Molefe mine plan sets out how the company intends to scale up. Connecting Pits 2 and 3 into a single enlarged open pit — requiring around four months of development work and removal of 400,000 tonnes of overburden — will lift the quarterly mining rate from 15,000 tonnes to 60,000 tonnes of copper reef.

High-grade material heads straight to Sable for direct leaching while medium-grade ore will be upgraded on-site first. Phase 2 drilling of the eastern extension is the immediate priority, with first production from that area targeted within a year.

Could all be forgiven in the months ahead?

It may very well be.

Produce & Expand

Xtract Resources - antimony and copper production is coming but a news light month. To be fair, there’s little to update on during the build out.

Switch Metals has completed the resource washing programme at its Issia tantalum project in Côte d’Ivoire, on time and within budget.

Independent lab assays and geological modelling are running in parallel, with the first Mineral Resource Estimate due in the coming weeks.

The company plans to publish three incremental MREs in sequence — starting with eluvial and colluvial targets, then incorporating additional tantalum-rich material, and finally covering alluvial drainage targets — building out the resource picture in stages through the rest of 2026.

As a reminder, Issia sits within a 1,015 square kilometre land package in south-west Côte d’Ivoire along a pegmatite corridor with known tantalum and lithium mineralisation.

The first MRE is intended as a stepping stone toward technical and economic studies and eventually a mining licence application — a pathway the company says is also central to its early cash flow plans.

Tantalum prices are rising, and demand for conflict-free, ethically sourced supply is growing.

This will be a big winner in the years to come.

Alien Metals noted that JV partner West Coast Silver has started its planned 4,000 metre Reverse Circulation drilling program at Elizabeth Hill.

But other than this, little independent news is forthcoming. With the PGMs also being worked on by a JV partner, we need movement on the iron ore, or perhaps another asset to market.

Otherwise, we await out partners’ news announcements - let’s hope for some good results.

Bezant increased its stake in the Hope & Gorob copper-gold project from 70% to 90%, buying out a 20% interest from Namibian partner MKH for £1.1 million — half in shares, half in staged cash payments.

This is objectively very good news.

More good news: the mining licence covering the NLZM processing plant — acquired in December 2025 and intended to process pre-concentrate from Hope & Gorob — has been renewed for a full 10 years to 2036.

The plant is a critical piece of the production puzzle, sitting downstream of the mine site and handling final concentration before the copper-gold product goes to market.

Bezant also signed a five-year exclusive mining and logistics contract with Unitrans Namibia, covering drilling, blasting, loading, hauling and road maintenance at the mine site, as well as trucking of pre-concentrate to the NLZM plant.

The contract is extendable and forms a substantial portion of the project’s operating cost base. All parties are working toward commercial operations beginning in the second half of this year.

The recent development update also confirmed that timeline remains on track. Engineering design is 100% complete, 45% of work programs have already been awarded and long-lead equipment is being fabricated — with a cone crusher due on site very shortly.

Construction crews are active at both the mine site and the NLZM plant, where refurbishment has begun. On financing, the $7 million facility is in advanced documentation stages following completion of the lender’s due diligence.

Obviously, capital would need to be raised to bridge this long-awaited $7 million, and to pay for that extra 20% - but the £2 million raised was done at a steep discount and with warrants.

I was not happy with the terms secured and know others weren’t either. There’s no sugarcoating that - but we are where we are and production is slated for later in 2026. It’s possible that the discount was less in percentage terms when the placing was agreed.

The profit potential remains exceptional.

Arbitration Plays

Zenith saw its solar development pipeline independent valuation update come in at EUR54.7 million - nearly double the figure of December 2025.

More importantly, the arbitration battle with Tunisia rumbles on. Early in March, Tunisia missed the Swiss Federal Supreme Court’s deadline to respond to an annulment application filed by Zenith’s subsidiary Canadian North Africa Oil and Gas (CNAOG), submitting instead a jurisdictional challenge arguing the case belongs in Tunisian courts — a move that will surprise nobody who has followed this dispute.

CNAOG brought the annulment application in September 2025 after uncovering what it says were previously undisclosed connections between two members of the original arbitration tribunal — including its chair — and the Tunisian state, amounting to a serious conflict of interest.

The underlying claim relates to the alleged arbitrary termination of the SLK oil concession, with CNAOG seeking around $130 million in lost revenues and damages.

Tunisia’s latest manoeuvre is consistent with a pattern of deliberate delay tactics.

It won’t work.

Exploration Games

Rome Resources - THEY FOUND IT. Finally. Drilling at Kalayi confirmed high-grade mineralisation persisting at depth across multiple holes.

Standout intercepts included 10 metres at 1.3% tin from 220 metres in KBDD029, and a 1 metre hit at 6.6% tin within KBDD030 (though all indicative XRF results pending formal laboratory assay).

Nearly 2,700 metres of core has been recovered since drilling restarted at the end of 2025, with around 960 kilograms of samples dispatched to ALS Laboratories in Johannesburg.

Drillhole KBDD033 returned the widest tin-bearing intercept at Kalayi to date — 20 metres at 1.0% tin from 144 metres, including sub-intervals grading up to 2.1% tin, plus additional shallower hits.

Drilled beneath two earlier holes that had shown narrower high-grade intervals, KBDD033 suggests the mineralised zone may be widening and strengthening with depth — a geometry Rome Resources draws explicit comparison to Alphamin’s nearby Mpama South deposit, where tin zones are known to broaden downward.

A follow-up hole, KBDD034, is already underway beneath KBDD033 to test that thesis further.

The results are expected to feed into an updated Mineral Resource Estimate, which the company says could deliver a solid uplift on the existing figure.

This will come good now - the tin IS there and now it’s just a waiting game.

Ajax Resources executed a definitive option-to-purchase agreement for the Macacha copper-silver project in Salta Province, Argentina — formerly known as the Leon Project, renamed in honour of Argentine independence heroine Macacha Güemes.

The project carries a historical JORC (2004) resource of 6.6 million tonnes at 0.62% copper and 18 g/t silver covering only the near-surface oxide horizon, with the deeper sulphide zone entirely untested.

Around $25 million was spent on the project by previous owner Alexander Mining between 2005 and 2010, including a successful trial of open-pit extraction and heap-leach recovery that produced copper cathode on site. Ajax intends to drill the sulphide horizon and publish an updated JORC (2012) resource during the option period.

Days later, the company announced it had signed a definitive agreement to acquire the Pereira Velho gold project in Alagoas State, Brazil from an entity affiliated with Appian Capital — one of mining’s most respected private equity groups, with around $5 billion under management.

The total consideration is up to $2.1 million, structured largely around milestones, with the bulk payable in shares upon delivery of a 350,000 ounce JORC resource.

Appian’s in-house estimate already stands at around 110,000 ounces, with only roughly 10% of the project area explored. The nearby Serrote project, in the same region, was acquired by Appian for $30 million and sold in 2025 for approximately $420 million — a data point Ajax is understandably keen to highlight.

Appian is taking a disclosable shareholding in Ajax as part of the deal - which is itself perhaps a bigger deal.

Sandwiched between the two acquisitions, Ajax also revealed it has entered negotiations with two potential buyers for Eureka — one a large Chinese mining group with an established Argentine presence, the other a leading local investor in gold and base metals.

Ajax is seeking cash consideration plus a life-of-mine royalty. The company holds around £3.4 million in cash with no debt, and frames any proceeds from Eureka as fuel to accelerate Macacha, which it considers the more advanced near-term opportunity.

These announcements came at the start of the month, and there has been quiet since, which may open up a cheap entry point for anyone sitting on their hands.

Arc Minerals has kicked off a ground-based magnetic and induced polarisation survey over its Virgo licence in Botswana’s Kalahari Copper Belt, one of Africa’s most active copper exploration corridors.

The program covers 295 line kilometres of magnetic surveying at 50 metre spacing, followed immediately by 52.5 kilometres of IP surveying, with data acquisition and interpretation expected to wrap up by end of Q2.

The surveys are designed to map the contact between the D’kar and Ngwako Pan formations — the geological boundary that hosts every known copper deposit in this part of the belt, particularly where structural domes create favourable traps for copper and silver mineralisation.

The work builds on a more limited IP survey carried out over part of the same licence in 2024, which successfully identified and verified the formation contact before drilling commenced. Arc is now extending coverage across the full length of the hypothesised contact zone, with the ultimate aim of defining up to 15 kilometres of prospective target within the licence.

The Zambian legals continue in the background - we need a resolution.

Moonshots

AFC Energy is becoming H-Power. A name change was sorely needed, but what’s needed more is further material news to sustain the momentum. I remain convinced this is an exceptional opportunity and that the 10x returns are fully in play here.

Defence Holdings’ has its new CEO (I will interview when appropriate), with CTO Andy McCartney recently taking a lovely photo with Jade Leung, the Prime Minister’s AI Advisor.

Jade is hiring multiple people for her department.

There is no more important door to be pulled through.

You are being lead to water, horsey.

Take a drink.

Solvonis has been granted a US composition-of-matter patent covering a monoamine modulator compound series from its PTSD discovery programme, targeting the serotonin, dopamine and noradrenaline transporter systems.

Composition-of-matter protection is the most commercially valuable form of patent in drug development, protecting the underlying compounds themselves rather than just their application or manufacturing process — meaning it’s harder to design around and broader in scope than most alternatives.

The grant follows a USPTO patent allowance announced in January 2026, and sits alongside the recent selection of SVN-114 as the lead candidate from the programme.

PTSD affects more than 20 million people across the UK, US and major European markets, with very few approved pharmacological options — a gap that is attracting serious commercial attention.

Otsuka’s agreement to acquire Transcend Therapeutics for up to US$1.225 billion is the most recent signal of how much strategic appetite exists for next-generation PTSD treatments.

Solvonis frames this patent as part of a broader chemistry estate being built around the programme, with CSO Professor David Nutt noting that exploring multiple compound series is a deliberate strategy to preserve optionality for future optimisation and differentiated development pathways beyond SVN-114.

We are again in wait and see mode here, but I have no concerns.

Immupharma has received its first Combined Search and Examination Report on the UK patent application for P140.

The company intends to follow the UK filing with a Patent Cooperation Treaty application to seek protection across key commercial territories. Alongside the patent progress, a new study designed to stress-test P140's associated diagnostic test returned positive results, strengthening the statistical underpinning of the application.

The company was expected to commercialise this asset before requiring more funding, but clearly it’s taking longer than hoped. It’s now raised an additional £6.5 million, but in its latest RNS noted that:

‘P140 remains a core value driver for ImmuPharma. The Company continues to progress discussions with a number of potential partners, including under signed confidentiality agreements. The management team also attended the Bio-Europe Spring healthcare event in Lisbon this week, where a number of meetings were held in relation to P140. ImmuPharma remains focused on completing a value‑enhancing licensing deal in 2026.’

This would be genuinely transformative and the upside potential remains.

United Oil & Gas - piston coring results will come any day now and discussions with JV partners are ongoing.

I think enough’s been said here before.

This is a risk play. Fingers crossed.

Stallion Uranium has completed a helicopter-borne VTEM Plus airborne electromagnetic survey over the Stone Island target area of its Moonlite Project in the Southwestern Athabasca Basin across two grids totalling 676 line-kilometres.

Meanwhile, the company's maiden diamond drilling program at the Coyote Target is actively progressing with two rigs operating, though challenging conditions have been encountered, with all current holes intersecting massive alteration and significant structural influence from the underlying regional fault system.

This is fucking great news by the way, as it massively ups the chances of success (alteration = places uranium can get trapped).

There is a reason why US investors are buying.

This team don’t miss.

New Players

I’m adding in a few new picks for Q2 - Great Western Mining Corporation, Upland Resources, Arkle Resources, Critical Mineral Resources, Aterian, Fulcrum Metals & Delta Gold.

I am not going to go into detail on these today - you’ve had in-depth articles on each through Q1, which can be found in the archive, but I will do my best to keep these in the mix as we go forward.

There are two more companies soon to hit AIM I’m looking at currently; Serval Resources which has just raised £2.9 million and is moving from AQUIS, and Rift Helium, a new IPO which plans to hit the market shortly.

I think both could be winners; the people and assets are solid, and both are cashed up.

Looking at the bottom line…

Trump is an unpredictable dog. Use your tax allowances (the government takes enough as it is). And while nobody knows what will happen next with any real certainty, there’s a sweet spot between risk-taking and risk management to be found.

Let me know when you find it.

And eat your daily banana.

Til next time!

Thank you Charles. After a great start to the year, March has been a disaster, but lots of opportunities and discounted valuations at the start of the new tax year. I honestly thought Trump was posturing Jan/Feb and didn’t think for one minute he’d blindly go to war with Iran; not a statesman, a megalomaniac! For everyone’s sake, praying the war will be over soon. Great update from you and very much appreciated!

Thanks Charles, have a great Easter!