Small Cap Mining: August Review

Sometimes, you have to sweat for it.

Good Evening Team.

In London’s financial world, we have an unofficial gentleman’s understanding - to do precisely nothing over the second half of July and entirety of August, so that everyone can take a well-deserved break.

This year, the work slowdown has simply not happened. It might be Trump, it might be global chaos, or it could simply be that every major asset class from gold to stocks to bonds to Bitcoin are at multi-year, decade or even all-time highs…

and nobody knows when the music is going to stop.

I remain of the view that the global economy pretty much resembles one of the many BTC Treasury stocks - we’re at the high now, but it’s all paper gains and those gains could be given up at any time.

For reference, other than the constant wars, we’re witnessing a total breakdown of competent political leadership across the western hemisphere in multiple areas - but let’s start with the UK.

The Online Safety Act - initiated by the Tories, but passed by Labour - is political censorship. There is no other way to describe it. Any semi-capable seven year old can get around these internet blockers.

And when we have the likes of clown-in-chief Peter Kyle telling you that ‘verifying your age keeps a child safe,’ we can know with certainty that it’s all bullshit.

It’s bullshit.

Especially when Australia and the US are both introducing similar ID checks at the exact same time.

And is your data going to a trusted government server?

Of course not - it’s going to some dodgy third party who will 100% sell it on, and even in some magical world where they don’t, they’ll almost certainly get hacked.

It’s reasonable to hold the view that we have two tier justice in the UK. I’ll say that now before I’m censored for saying it.

When you have a government spy unit monitoring social media to crack down on citizens expressing discontent with immigration levels, or censoring political viewpoints, or locking someone up for a tweet but not for throwing bricks…

then people are going to be angry.

It’s a fact that many of the ‘asylum seekers’ in this country are abusing a system designed to help desperate people.

It’s a fact that taxes, housing costs and bills have never been so high, and public services so awful. And taxes are about to go up - again.

We could of course start with scrapping net zero. It’s not a coincidence that we have the highest energy prices in the developed world.

But at some point soon, the bond market is going to force some drastic changes because our rate of borrowing is patently unaffordable, and then, the widespread public anger is going to boil over.

We are borrowing £150 billion a year, of which £110 billion is simply to pay interest on past borrowing.

It’s like the government keeps logging onto ClearScore and paying a fee for another couple of years to balance transfer their credit card.

To get back to 1990s-era spending levels, we need to cut total government spending by about 35%.

And yet Reeves claims that she ‘has got the balance right on tax.’

She’s either a moron, out of her depth, or mathematically challenged. Perhaps all three.

The maths is not going to change. We are not going to get the magic growth wanted, mostly because all our wealthy job creators are exiting via Heathrow.

Sorry, only after the entire airport went down.

Coinbase were not allowed to run their ad on TV depicting the UK as a shithole because, very clearly, the message hits too close to home.

Want to be a civil service intern? Sorry, from next year you can only apply if your parents were ‘working class’ when you were 14 years old.

These people are thick as mince, and the country has had enough.

In the US, the walls are closing in. You might think, WOW, look at all that tariff income! But that’s just tax, on American companies, paid for by American consumers.

I won’t bother covering the current tariff rates as they change dependent on Trump’s mood.

But job cuts rose by 140% year-over-year in July.

Year-to-date, US-based employers have announced 806,383 job cuts, the highest total for any January–July period since 2020 (the pandemic crash).

The US public sector led the increase with 292,294 job cuts year-to-date, but the technology and retail sectors followed, with 89,251 and 80,487 job cuts respectively.

The real economy is crashing - and those employee reductions in the tech sector are not AI savings, they’re AI cuts.

The worst thing is that you can’t even rely on the data - June jobs were revised down by 133,000, from 147,000 to just 14,000. And May was revised down by 125,000 from 144,000 to 19,000.

258,000 US jobs just disappeared from the data across two months, overnight.

The person in charge of this data collation was fired by Trump (whether for political or competency reasons we will never know) but what’s clear is that the cracks are showing.

However, as much as I find Trump distasteful, it was deeply cathartic to watch him verbally abuse Starmer in person.

And you know what? I finally figured out who our PM reminds me of. He’s Dolores Umbridge from Harry Potter.

‘I must not tell lies’ carves Harry into his own bloodied hand, another scar which will stay with him forever.

‘I will have order’ demands Starmer, our toadlike leader.

What a wanker.

Hang on, we don’t know his internet search history. That’s for the peasants.

Next they’ll try to push digital IDs, without which you will not be able to use the internet. Watch it happen. And as an FYI on VPNs - they record your every activity. Also, you can’t really ban them. They’re how the internet works.

I’m sure our overlords will try though.

The conspiracy theorist in me questions why the Kids Online Safety Act in the US, the EU's Digital Services Act and an Australian equivalent are all being pushed at the same time.

We’re banning Spotify for 17-year-olds apparently, but the Aussies are trying to prevent 15-year-olds from using YouTube.

These authoritarian nutjobs can all fuck off.

I digress.

What you need to recognise in the US is that (a) AI is a bubble and (b) the paper gains are weak.

Trump was able to torch those gains earlier this year, and could well do so again. The valuations are all based on hopium - over the past month or so Bank of America analysis shows that institutional investors have sold $10 billion in equities.

On the other hand, corporations bought back $1.2 billion of their own stock, while retail and hedge funds purchased $1.4 billion and $500 million, respectively.

Retail investors have now been net buyers for the vast majority of the year, while institutions remain net sellers.

Someone is wrong, and will pay the price.

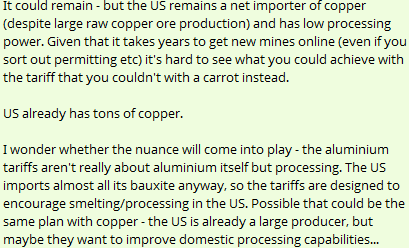

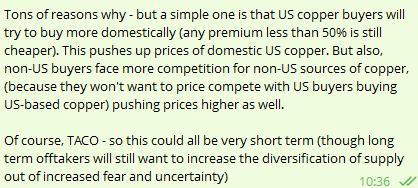

Just consider what happened in the copper market in July.

On 8 July, copper futures enjoyed their biggest one day rise - some 13% - in over 40 years due to Trump’s 50% tariffs.

As I noted in the Telegram Group when asked what would happen next:

These tariffs were always going to be rolled back and then concentrated on processing - and this is exactly what has happened: tariffs will apply to ‘semi-finished’ copper products but not refined input materials.

And we see the steepest copper price drop in decades.

Quel surprise!

Interestingly though, even after this drop, copper should now start to rise back to new highs - for reasons noted in the blurb above.

Meanwhile, no country in the world can get a grip of their spending, so gold is continuing to go up.

And then there’s the critical minerals angle - this war is only going to heat up. After gallium, germanium, antimony, graphite and tungsten, the next metal China will hit with export controls will be titanium.

I reckon you can guess which stock I’m backing when this happens, but I can’t see why other analysts can’t recognise a very obvious pattern playing out, and position accordingly.

Tungsten pricing remains well behind the antimony curve as well, so more gains will come from that quarter.

My only other comment would be on the institutions predicting the metal pricing.

Goldman Sachs told clients to go long on copper a day before the price crash.

Jefferies estimated that Newmont would generate $664 million in free cash flow this quarter - they generated $1.7 billion.

These people are either lying to you to make money, or are really bad at their jobs.

Without any further ado, as I could chat about this stuff forever, let’s review:

The golden trio

Greatland Resources (formerly Gold) hit a stumbling block this month. We’re still up >100% year-to-date but management have learnt an expensive lesson in what ASX investors prioritise and care about compared to us here in London.

I think you could tell from the call - whether anger, frustration or bewilderment - the team were simply not expecting that reaction.

And to be fair, chopping a third off the market cap was, in my view, an overreaction, but the stock has recovered a little already.

For perspective, the company has gone from nothing to $575 million in the bank this year, and produced 180koz Au equivalent ounces. There are millions of ounces in the ground for the taking, and the long term trajectory is still fine.

The bottom line though is that initial production will be 11% lower in FY26 than forecast in the ASX IPO prospectus - mostly due to risk weighting lower grade gold in stockpile and lower mining rates in some open pit areas.

The sell-off thereafter is likely a combination of manipulation to let the right people buy cheaply, and anger that guidance was changed so quickly after the ASX listing.

It’s understandable some will be miffed, and the ASX regulator will be asking questions, given how quickly guidance changed.

CEO Shaun Day is presenting on Tuesday at Diggers & Dealers - and the pressure is on.

He does have one man in his corner though: Barrenjoey’s Daniel Morgan notes that the ‘Telfer ore is not the main game for the Greatland investment thesis’ - it’s Havieron and its low cost, long life opportunity.

The good news is that the Havieron feasibility study is still scheduled for Q4. And no, the aquifers should not be a problem - these are common in AUS mining.

Better, you also have six drill rigs turning at quarter end and 27,840 metres drilled in the June quarter. The largest drilling program in Telfer's operating history is planned, with 240,000 metres total drilling planned (+145% vs FY21-25 average) across eight drill rigs.

The general consensus is that more, higher grade, gold is there to be found.

And all this exploration and optimisation will be self-funded by Telfer profits.

A quick shout out here to Power Metal spin-off First Development Resources - they’ve IPO’d and got a drill contractor ready to sink into the first of three magnetic bullseye targets at Wallal, with similar signatures to Havieron.

High risk, high reward - but I have a few (fully accepting the risks of pure exploration).

Back to GGP - bottom line for me is that the stock was briefly on sale, has recovered somewhat, and should come back to record highs and further as time goes on.

The investment case may become particularly compelling if a global recession does come around, causing oil to crash - while gold continues to new record highs as the money printing continues.

I guess we’ll see.

Also - assuming GGP still gets into the ASX 200, funds usually start accumulating stock around one to two weeks before the effective date of the rebalance.

The rebalance usually becomes effective after the third Friday of the month, which is 19 September 2025 this quarter.

So expect some serious volume between 15-19 September.

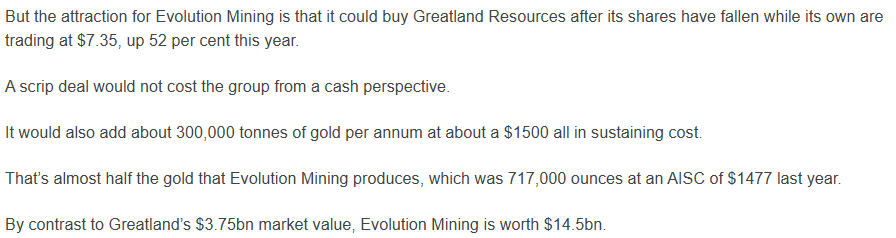

And consider the Evolution buyout angle. The Australian (reputable as they come) is reporting some are pressing the larger company to make an offer on the weakness:

This says it all really, but I would also note that GGP is additionally undervalued compared to its other ASX peers on most metrics as well.

I still think £4 a share is realistic and will continue to hold until this target is achieved.

Sovereign Metals has delivered yet another series of decent updates through July, reinforcing its current position as a future global critical minerals leader.

The DFS comes in Q4 and then the buyout games begin.

The good news is that the DFS-level geotechnical investigations have successfully concluded - over 400 individual tests were conducted across all planned infrastructure zones, including the mine site, tailings storage facility and raw water dam.

Preliminary findings confirm consistent regional stratigraphy and favourable subsurface conditions, supporting cost-effective foundation designs.

This again de-risks Kasiya’s infrastructure delivery - and again, this work was undertaken with oversight from the Sovereign–Rio Tinto Technical Committee, bringing world-class technical governance to the process.

Sovereign also signed a non-binding Memorandum of Understanding with ESCOM, Malawi’s national electricity supplier, to establish a long-term power supply framework. This agreement is a foundational step towards future definitive power agreements and comes just weeks after the World Bank approved a $350 million grant to support the development of Malawi’s Mpatamanga Hydropower Project.

The World Bank also categorised Kasiya as low/medium risk this July - and expects mining to become:

'the largest export sector and a significant source of revenues within the next decade' for Malawi…

…'There are some bright spots in the economy that can drive growth over the medium term, especially through mega-projects in the energy and mining sectors. Critical decisions will need to be made in the coming months to ensure that these projects continue to advance and that the country can make the most of these opportunities.'

Well, if they want to co-fund it, they know where we are.

Meanwhile, Sovereign’s graphite business case has received a major boost. The US Commerce Department has imposed 93.5% preliminary anti-dumping duties on Chinese graphite imports, fundamentally redrawing the supply landscape for battery manufacturers.

With total effective tariffs now as high as 160%, ex-Chinese supply is becoming a necessity.

Kasiya is uniquely positioned to benefit as the world’s largest and lowest-cost ex-China graphite deposit, with an industry-leading incremental production cost of just $241 per tonne.

Sovereign’s titanium value proposition is also attracting global attention. Japanese titanium metal specialist Toho Titanium — a key supplier to aerospace and industrial OEMs — recently confirmed that Kasiya’s natural rutile meets its standards.

This external validation not only de-risks future offtake agreements but places Sovereign firmly on the radar of Tier 1 industrial buyers.

We’re going to get more offtake agreements very soon. It’ll be the Japanese.

Remember - if you want to sell something, you need to make it desirable. In mining, that means doing everything you would to get into production regardless of any offers waiting in the wings.

SVML is down slightly this year but is very well cashed up from the raise at a significant premium to the current share price - and volume is very low. Few are selling; few are buying.

This will change.

Amaroq seems to have found its floor and is down around 25% year-to-date (more or less, it fluctuates).

Like Sovereign, the stock is well-backed by large institutions, and well capitalised for activity after a recent raise - again at a premium to the current share price.

Amaroq’s big news is the launch of its most extensive exploration campaign to date for 2025, focused on expanding its gold resource base and investigating new mineral opportunities across Greenland.

At the flagship Nalunaq gold mine, drilling has now started with plans for up to 3,500 metres of surface drilling - and near-continuous underground drilling, aiming to expand the resource within the Mountain and Target blocks.

Meanwhile, at Nanoq (an analogous gold system within the same Nanortalik belt) AMRQ is conducting around 5,000 metres of core drilling, targeting a maiden Mineral Resource Estimate.

Nanoq could very well end up being a larger beast.

In addition to its gold strategy, Amaroq is advancing exploration for copper, nickel, and rare earth elements across what remains the largest exploration portfolio in Greenland.

Reconnaissance and sampling are underway within the South Greenland Copper Belt, with the potential for scout drilling depending on initial results.

At Stendalen, geological mapping will refine nickel targets for drilling in 2026, while REE exploration has ramped up across the Gardar Igneous Province, with newly awarded licences allowing for the assessment of both known and unexplored targets.

Looking further ahead, Amaroq has also started conducting groundwork for future campaigns.

At the West Greenland Hub (home to the historic Black Angel mine and the nearby Kangerluarsuk project) initial reviews and site visits have been completed to assess the redevelopment potential, with a major exploration campaign planned for 2026.

Similarly, a reconnaissance visit is planned for the Minturn IOCG project in the northwest, pending licence approval.

There’s so much news to come that ALS have installed a lab on site:

If that’s not a vote of confidence, nothing is.

And remember, the CEO has made clear the US is keen on getting involved at a very high level - see Bloomberg.

The rumour saw the stock shoot up earlier this year. The fact, when it comes, will do the same.

This is the optimisation year for the gold - but assuming all is well, then by this time next year we will be up to 450tpd, fully optimised and with masses of assays coming through on a regular basis.

As a three, we’re still up decently on GGP, SVML and AMRQ as a package and I remain confident they will deliver a positive return over 2025.

The Explorers

Rome Resources continues to keep grinding. In recent results, the company highlighted the 3,443m of core recovered to the end of 2024 - and a further 1,587m of core recovered to 30 June 2025.

Operating conditions have ‘essentially returned to normal’ and a peace, if fragile, seems to be in place as expected.

I expect that August will be another waiting month.

While the latest drilling has further defined the scale of tin mineralisation at Kalayi and highlighted the copper and tin potential at Mont Agoma, the company now requires a few weeks to fully analyse and interpret what these results reveal about the broader polymetallic system at Bise North — including its copper, tin, zinc, and silver mineralisation.

Ergo, all assays were completed in July, and the Maiden Resource Estimate will come in September.

I suspect this explains the dip below 0.3p - traders selling now and will come back towards the end of August.

The long-term potential for an asset sale to an IRH-backed Alphamin, given that Rome’s management and exploration team found Alphamin’s core Bisie deposit, is immense.

With the standard caveats.

Arc Minerals - frustrating. As active Zambian court cases are ongoing, I think it’s inappropriate for me to comment, other than to say that I believe this will be resolved in Arc and Anglo American’s favour.

Once the cases are dealt with, I will cover the result in depth - but clearly, if the court cases are resolved as expected and drilling starts with the major, the recovery could be sharp.

I will say though that as with most African jurisdictions, dealing with political and legal risk is part and parcel of the investment case.

Both explorers are down year-to-date but have been up at points, and both on low volumes.

The Dealmakers

Asiamet appointed Grant Samuel to lead the strategic investor engagement process for BKM on 18 July.

This is strong evidence that an asset or even entire company sale is coming. GS are M&A experts (see countless documents and deals produced including the Newcrest valuation of assets last year).

Project financing/asset sale discussions are ongoing:

‘The Company has now commenced a structured programme of engagement with interested parties.’

Limestone and flowsheet optimisation work continues, and to me, it’s all the standard nonsense of pretending to be planning to go into production to secure the best asset price at sale.

And the sale RNS will come out of left field.

Normally the timeline might be 6-12 months, but a lot of the larger due diligence items have already been taken care of - so a sale this calendar year and certainly by this time next year, is happening.

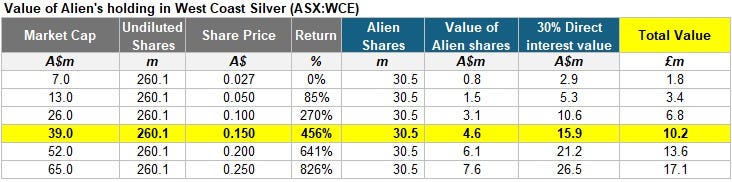

Alien has at times been worth less this month in market capitalisation terms than its value in West Coast Silver.

This is not surprising when considering initial assays, including from drill hole 25WCDD001, the first drill hole completed from the 2025 program:

21 metres at 1,047g/t Ag from 10 metres including:

8 metres at 2,632 g/t Ag from 22 metres including:

1 metre at 15,071 g/t Ag from 27 metres

You can’t ask for much better than that, though the next set of assays have a lot riding on them.

Remember, free carry to mine.

At present, the value in West Coast is about the same as Alien’s market cap, meaning that Hancock, the additional iron ore tenements, and Munni Munni are all valued at zero enterprise value.

So despite some nice movement from a low base this month, it’s still cheap.

Hancock was treated to a new exploration target of up to 27 million tonnes at grades of up to 62% Fe - in addition to the current 8.4Mt @ 60.0% Fe in Mining Reserve and Mineral Resource estimate - and the BHP Access Agreement has been fully executed for tenement E47/5159.

There does seem to be some cautious optimism at last.

Blencowe - I spoke to Mike a few days ago, so think not much else needs to said at this stage.

I would note though that their new offtaker Perpetuus was going to be acquired by China back in 2022 but the UK government ordered a national security review - and the deal was dropped immediately.

This perhaps goes to show what kind of offtaker/graphite quality they’re working with.

Bezant - I think had an opportunity to sell its Blackstone Minerals shares (at times, worth more than its own market cap - sense a theme?) during the Macquarie raise, but chose not to.

This suggests Bird has the financing for Hope & Gorob at hand -I’ve estimated circa $15 million - and the free cash flow numbers for that capital input are exceptional as discussed several times in the past.

Interestingly, Blackstone has jointly bought a diamond drill rig to drill out Mankayan, so perhaps further increases in the investment are on the horizon.

But as last month, the re-rate higher hinges on financing for the mine, so sit and wait.

Guardian Metal got its initial grant from the US Department of Defence for $6.2 million this month, as predicted.

I covered the stock in depth days ago, but the bottom line is that in combination with the financing raised, the company now has the official backing of the US government with Pilot Mountain as a strategic US asset, and tens of millions of dollars to explore, develop and deliver.

Power Metal retains that insanely low market capitalisation which is often lower than its shareholding in GMET. But it’s also got millions in cash, a massive ongoing uranium exploration campaign in the Athabasca, a giant stake in FDR in which any drill win will see a huge value leap…Saudi Arabian plans and more.

I’ve now given up on the timing of the re-rate; I’m unsure what else can be done except slowly buying more shares.

Energy Pathways - again covered in depth this month, but the bottom line is that it’s a fully integrated, low-carbon energy hub designed to deliver energy storage, clean fuel production and dispatchable power.

In the past week alone, the company has signed transformative partnerships with Hazer Group (for clean hydrogen and graphite via methane pyrolysis), Siemens Energy (to lead a comprehensive system-wide feasibility study), and Costain (to assess onshore infrastructure locations).

The project aligns closely with government climate and industrial policy, promising to reduce reliance on imports, cut carbon emissions, and repurpose curtailed offshore wind. If approved, MESH could provide up to 20 TWh of clean energy services annually and become the backbone of a resilient, reindustrialised, net-zero UK energy system.

Importantly, the multi-asset nature of MESH means that it is useful to, but does not rely on, Net Zero continuing as national policy.

We just someone with the power of the pen to make the correct decision soon.

Year-to-date, Asiamet is up 19%, Alien 38%, Blencowe 19%, Bezant 125%, Guardian 95%, and Power flat (though this last one feels a tad unfair).

As a group then, we’re up 49% across the dealmakers portfolio, which perhaps speaks more to the febrile M&A ground than my stock picking skills.

Energy Pathways was added in during March, and has fallen about 25%, dragging the average return down to 38% - but this last one is a little different in that there is a binary risk with the licensing award.

Still though, not bad.

Jubilee & African Pioneer

Jubilee - we had an update on South Africa operations but this was largely irrelevant as these are being sold to fund a Zambian bonanza.

While I am fully aware that many long term shareholders are growing increasingly impatient, the Zambian copper update on numbers will come in August and this will give us something to work with.

I do think that this stock remains very undervalued.

If you consider the market cap is around £100 million ($130 million), and the asset sale of chrome/PGMs is worth $90 million - then the enterprise value of Roan, Sable and all copper mines in Zambia stands at a paltry $40 million, which is ridiculous.

It’s down about 10% year-to-date but has been bouncing around all over the place - which is to be expected given that the fundamental nature and risk/reward curve of the business is changing.

African Pioneer is recovering nicely from the dip. Swann has become an even more significant shareholder - and it makes sense.

AFP was awarded the mining licence for Ongombo at roughly the same time as sister company Bezant received its one for Hope & Gorob - both mines are in Namibia.

While AFP does not have shares in Blackstone, it sports a market capitalisation of just £2.8 million - and given the rise Bezant enjoyed, I suspect it will continue to recover from here.AD

AFP could sell Ongombo alone for multiple of this market cap and then there’s also the exploration with FQM to consider.

One imagines that any financing deal for Bezant will be swiftly followed with one for AFP - or vice versa.

When one comes, it may make good sense to position accordingly.

The Helium Pick

Again - covered this month - but bottom line is that Helix Exploration is still going strong.

In recent days, David Minchin has stepped down from his Executive Chair role, while Keith Spickelmier has been promoted to independent Non-Executive Chairman.

David was the right man for the IPO; he knows how to raise capital and keep the book tight. Shareholders wish him well, and will be keeping both eyes out for whatever his next venture may be.

Spickelmier is an interesting choice. He has a strong track record both in growing companies from exploration to production, and in corporate asset sales - including growing Westside Energy from inception to sale for $200 million back in 2008 money.

He notes:

‘The Company is currently in a very strong position; fully financed with supportive institutional investors, four production wells already drilled with a fifth on the way, and production plant construction commenced and going well.’

It’s good to see our institutional investors continue to support this play - and the names involved are not in for a quick 10%.

Get producing, or get sold.

The Moonshot

Emmerson is back up to 2p, and remains up 175% year-to-date. I de-risked on this one a couple of months ago, taking out my original stake.

You’re looking at what is likely to be a $2.2 billion claim - and the ones bringing it are a legal team which rarely misses.

Their recent wins are very public.

Happy to chill out now and wait for the RNS alert, whenever it comes.

Except the services which used to do this have all given up - come on Vox!

Closing Comments

Last month, I noted that ‘Mirriad Advertising, was a scalp idea - but it’s basically done nothing. You can’t win them all, but I still think a pop is possible (with beer money).’

It did shoot up for a few days in mid-July, I sold and got out.

My other monthly pick for July was GMET:

‘It’s on the list already, but I’m going to say it again.

Guardian Metals.

It’s coming.

Politico has reported that the US has halted shipments of some air defense missiles and munitions to Ukraine because its own stockpiles have fallen too low.

And there’s been yet another executive order: ‘Simplifying the Funding of Energy Infrastructure and Critical Mineral and Material Projects.’

The urgency to reshore is rising.’

The grant funding did come, but the rise was tempered by the fundraising activity. I have not taken any profits from this one and plan to continue to hold.

However if you were trading, it ended the month effectively flat - though did rise from 58p to 68p on 9 July before losing these gains. For now.

There are two takeaways from this month to consider.

The first is that to make real gains, you need to endure boredom in some cases as you wait for the right RNS to materialise, and sweating in others when something comes out of left field to knock you down a peg or two.

If you can’t do these things, small cap mining is not for you.

The second is that there is a very real value disconnect matrix going on - whether Power, Alien, Bezant or many others - where a shareholding in a portfolio company is worth less than its own market cap.

In my mind, these are effectively risk free investments - though of course the market can stay irrational longer than you can stay patient.

My monthly pick for August?

I don’t have one.

Like many others, I’m sitting happy on casino profits from the BTC treasury plays - more thoughts on these to come soon.

But rather than reinvest, or trying to pick more winners, I’m going to spend most of this month sitting on a beach, drinking cocktails and building sandcastles with my children while they’re still young enough to want to.

The market will still be here next month.