Panthera Resources

Did India steal a literal gold mine?

Good Morning Team.

A caveat before we begin. This is high-risk investing for experienced individuals capable of making their own sovereign decisions. Arbitration stocks are a highly specialised, high stakes investing theme with a sharp risk-reward profile.

We start with a gold project in Rajasthan that the Indian government decided it wanted for itself.

Not through negotiation or a fair buyout.

Through two decades of bureaucratic obstruction, a conveniently timed change in mining law, a rubber-stamp dismissal from the local high court, and then — the cherry on top — auctioning the whole thing off to a third party while the company that discovered and developed it was still fighting in court to get it back.

Yes, after my success with GreenX, Emmerson and Zenith, we’re going to consider another arbitration stock.

Panthera Resources is currently sitting at a market cap of roughly £50 million. It’s pursuing a US$1.58 billion damages claim against the Republic of India at the Permanent Court of Arbitration in The Hague, with a hearing scheduled for December 2026.

The PCA case number, for the diligent among you, is Indo Gold Pty Limited v. Republic of India, PCA Case No. 2024-51.

It’s publicly listed and very easy to look it up.

That asymmetry — £50 million market cap, $1.58 billion claim — is the entire thesis. You either think international investment treaty law is a functioning system capable of forcing sovereign accountability, or you don’t.

I think it is. Over the course of the medium term, I believe Panthera will win.

But, as I have been at pains to explain many times, I also believe that the high-risk nature of these investments means that splitting your potential investment over a handful of strong cases makes infinitely more sense than putting all your eggs in one basket.

Anything can happen in court.

But if justice prevails, Panthera shareholders should be looking for a juicy payout.

Let me explain why.

Bhukia Gold Project: What India Took

Before we get into treaty law and arbitration mechanics, you need to understand what’s at stake. Once you do, you’ll understand India’s brazenness.

In around 2004-2005, Panthera’s Australian subsidiary Indo Gold Pty Ltd (IGPL) made an initial investment in the Bhukia project in Rajasthan, through a joint venture with Metal Mining Pvt Ltd (MMI) — an Indian entity in which IGPL held a 70% interest.

IGPL provided all the funding and managed the exploration programmes, conducted in full compliance with Indian government rules and regulations.

They drilled 20 holes between 2005 and 2006. In October 2006, they published a then JORC-compliant mineral resource estimate of 38.5 million tonnes at 1.4 grams per tonne of gold, for a total of 1.74 million ounces.

By 2007, the company had identified exploration targets of 6 million ounces of gold and was planning a systematic drill-out campaign — the moment they received their Prospecting Licence.

That licence never came.

But the deposit kept getting bigger.

A lot bigger.

The Geological Survey of India — India’s own government agency — published a report in 2014 after completing over 150 drill holes.

Their conclusion: an indicated and inferred resource of 6.7 million ounces of gold. More recent GSI drilling hasn’t been fully incorporated, meaning the actual resource is likely even larger.

The Government of Rajasthan subsequently issued a gazette notification with an updated estimate: 113.52 million tonnes at 1.96 grams per tonne gold and 0.14% copper.

That's 7.2 million ounces of gold, plus copper, nickel and cobalt credits.

At today's gold price — let’s say around $5,000 per ounce — the in-ground value of Bhukia is somewhere north of $36 billion.

Think about that, from the perspective of the man on the Clapham omnibus. Put aside the law, and think in terms of what ‘feels’ fair.

India’s own geological agency confirmed 7.2 million ounces of gold, and the government that announced this then decided it wanted that gold for itself.

The company that found it got offered its costs back.

And then India auctioned the project off.

The winning bid came from Saiyyed Owais Ali, a director of a metals and minerals processing company. His winning offer: a 65.3% mineral share — meaning he pays India 65.3% of the value of all gold extracted every single month, plus $60 million upfront and $60 million in performance guarantees.

The GSI had reported an in-ground value of $16.7 billion at the gold price prevailing during the auction. India is therefore entitled to a royalty stream with a lifetime value north of $13 billion from an asset it simply took from Panthera.

Back when gold was a lot lower.

Someone looked at that deal and said yes.

That’s how good Bhukia is. And that auction — conducted in June 2024, after a Notice of Dispute had already been served — will prove to be one of the most expensive mistakes India made in this entire case.

Twenty Years of Obstruction

What distinguishes Panthera’s case from many resource arbitrations is that the expropriation didn’t happen in a single dramatic moment. India — and specifically the Government of Rajasthan — spent the better part of two decades constructing a slow-motion theft.

This is perhaps becoming a more common tactic as governments think they can simply outlast the financial and managerial resources of a junior - though with legal funding and big law firms now seeing the money to be made in these cases - this is also changing fast.

IGPL’s joint venture partner MMI held the Prospecting Licence Application for Bhukia. The application was repeatedly frustrated — not denied outright, just endlessly delayed, reviewed, sent back and reviewed again.

For over a decade, despite the project’s validity being confirmed by India’s own geological survey after over 150 successful drill holes.

This is a textbook government tactic in expropriation cases. Block the licence without giving formal public reasoning. And the obstruction is politically useful — it keeps the asset out of foreign hands — and legally deniable for years.

Until it isn’t.

Then in August 2018, the Government of Rajasthan rejected the application outright, on ‘spurious and legally untenable grounds.’ Even the local judiciary blinked at this — the High Court of Rajasthan issued an interim Stay Order on the decision. That Stay Order remained in place while MMI’s legal challenge worked through the courts.

Then India played its trump card.

In 2021, the Government of India passed the Mines and Minerals (Development and Regulation) Amendment Act — MMDR2021. Clause 13 stated that any pending Prospecting Licence Applications were deemed to have lapsed.

The legal basis that MMI had been fighting to vindicate in court simply ceased to exist. Parliament had legislated it away.

There was provision to reimburse companies for expenditures incurred.

Expenditures only -not the value of the asset.

Just: here’s your costs back, go home and give up.

Consider what that means.

Paying only expenditures assumes a 0% return on invested capital — that the mine wasn’t an investment at all from a time value of money perspective. You had £1 a year ago, you spent it on exploration, and now you have £1 back.

The £1 could have been generating returns in the meantime. The very existence of a compensation provision acknowledges the injustice. It’s just calibrated to be as small as legally defensible.

In September 2023, the Rajasthan High Court dismissed MMI’s writ petition, citing — you guessed it — the very MMDR2021 legislation that had been engineered to kill the claim. The court that had previously granted a Stay Order protecting Panthera’s interests now used India’s own law to terminate them.

And then Rajasthan auctioned Bhukia.

In summary, the government frustrated a foreign company’s legitimate licence application for fifteen years. Passed a law to extinguish that application. Won a court case using that same law. Then auctioned the deposit to a domestic buyer — while a Notice of Dispute was sitting on the government’s desk.

India bet Panthera would fold.

They were wrong.

Why India Has a Problem

The legal foundation of Panthera’s claim is the 1999 Agreement between the Government of Australia and the Government of the Republic of India on the Promotion and Protection of Investments — the Australia-India Bilateral Investment Treaty.

If you’ve followed my work for years, you’ll know how this works, but for the newcomers…

BITs are international contracts between sovereign states. When India signed this one, it agreed to treat Australian investors in certain ways. If it breaches those obligations, the investor can take the sovereign to international arbitration and claim damages.

Yes, the treaty has since been terminated, but — like most BITs — it contains a sunset clause preserving investor rights for ten years post-termination.

Ergo, Panthera can still claim under it.

Three articles sit at the core of IGPL’s case:

Article 3 — Promotion and Protection of Investments. Each contracting party must encourage and create favourable conditions for investors from the other to operate in their territory — provided those investors respect local laws, which all evidence shows IGPL did.

India didn’t just fail to encourage investment - they actively obstructed a valid, government-verified mining project for fifteen years and then legislated the investment into non-existence. The fact that IGPL abided by every Indian rule and regulation — carrying out work programmes in full compliance, filing reports on time etc — makes India’s conduct look worse, not better.

Article 4 — Treatment of Investments. Each party must grant investments from the other the same treatment it would grant domestic companies — (aka ‘most favoured nation’ treatment).

India blocked the licensing of a valid mining operation owned by an Australian company while domestically-owned mining operations continued. The Bhukia project’s merits were validated by the government’s own geological agency.

So a domestic operator would have received the licence, but IGPL didn’t.

Article 7 — Expropriation and Nationalisation. India cannot expropriate Australian investments without prompt, adequate and effective compensation at fair market value immediately before the expropriation. MMDR2021 is textbook indirect expropriation — the state didn’t formally seize anything, but through legislative action it destroyed the entire economic value of IGPL’s investment.

The Treaty is explicit in that compensation must be based on market value immediately before the expropriation. That is the key legal anchor for IGPL’s $1.58 billion claim.

Why This Case Is Stronger Than Most

I’ve covered a few of these arbitration situations - and ignored many as hopeless.

Six things make Panthera’s case relatively compelling:

India created its own evidence against itself. By auctioning Bhukia while the arbitration was proceeding — after the Notice of Dispute had been served — India inadvertently provided contemporaneous market evidence of exactly what the project is worth.

A third-party buyer agreed to pay $120 million upfront plus 65.3% of all future mineral production, which is a real market transaction. Panthera’s damages experts will wave that in front of the tribunal and say: this is what the market said Bhukia was worth in June 2024, two years after you took it. Imagine what it was worth when you took it.

India handed Panthera’s lawyers a gift.

India’s own geological survey validated the asset. Panthera’s claim is not built on its own promotional resource estimates, unlike many others.

The GSI — a branch of the Indian government — confirmed 7.2 million ounces of gold after drilling over 150 holes and Rajasthan published the updated estimate as a gazette notification.

It becomes extremely difficult for India to argue that the resource estimate is overstated when their own agency produced it and their own government used it to run an auction.

Twenty years of documented obstruction. This isn’t a case where a government changed one regulation and an investor cries expropriation (there are many of these).

There is a 20 year paper trail of repeated delays, a rejected licence on legally untenable grounds that prompted a court Stay Order, targeted legislation to extinguish that application and then an auction. The pattern of conduct is extensively documented.

LCM’s extended due diligence is a signal. Litigation Capital Management (despite their own financial concerns) spent six months stress-testing this case — extending their due diligence deadline six times between May and August 2023, to the market’s considerable anxiety. Then they came back and not only confirmed the deal but increased the facility from $10.5 million to $13.6 million.

More scrutiny, more confidence, more capital committed. Despite their current position, LCM hs a strong win rate overall, and their increased commitment after extended scrutiny is the closest thing to independent validation of the case’s merits that we’re going to get in the public domain. LCM also funded others I’ve covered - with success.

Precedent supports the claim. Three comparable cases matter.

Indiana Resources vs Tanzania: expropriation of a nickel project resulted in a $109 million award in 2023, with Tanzania subsequently paying $90 million (82.5% of the award) to avoid asset seizures.

Montero Mining vs Tanzania: a $70 million claim for rare earth expropriation settled pre-hearing at $27 million (39% of the claim).

Cairn Energy vs India — a $1.2 billion award against India itself (for retroactive tax treatment), which India ultimately settled for $1.06 billion in 2021 after Cairn began seizing Air India planes in France. Yes, this does eventually happen.

Post-Cairn, India is acutely aware that defying PCA awards has real consequences.

India is a far superior counterparty to Tanzania. The Indiana Resources and Montero settlements were constrained by Tanzania having limited foreign assets to seize.

India has hundreds of billions of dollars of assets outside its borders. PCA awards are enforceable in 145+ countries. India knows what happens when it ignores them. Cairn taught them.

Legal Teams

The PCA case page — publicly available at pca-cpa.org/en/cases/343 — lists the full legal teams for both sides. And the names are illuminating.

IGPL’s team is led by King & Spalding LLP, one of the pre-eminent international arbitration firms in the world, described by industry observers as ‘the best international arbitration team on the market.’

King & Spalding built its reputation on a series of landmark investor wins against Argentina in the 2000s, helped Anadarko and Maersk settle a multibillion-dollar dispute with Algeria, and won a $2 billion award for Dow Chemicals.

The firm has obtained some of the most significant awards in history in investment arbitration.

Their team on this case includes Wade Coriell (head of King & Spalding’s international arbitration practice), Aloysius Llamzon, Thomas Sprange KC, and several associates.

Alongside King & Spalding is Ben Juratowitch KC of Essex Court Chambers — and his is the name that should make you pay attention.

Juratowitch is described by Who’s Who Legal as ‘one of the best advocates in the business’ in international arbitration. Chambers Global calls him ‘outstanding... fiercely bright, an extremely effective advocate.’

He was appointed King’s Counsel in 2017, served as Head of Public International Law at Freshfields for seven years, holds a DPhil from Oxford where he was a Rhodes Scholar, and was named Legal 500’s Silk of the Year for International Arbitration in 2023.

His case history reads like a tour of the world’s most significant investment treaty disputes: represented South Africa in expropriation claims arising from black economic empowerment mining policies, acted for Romania in the Micula case, represented investors in the Egypt-Israel gas pipeline arbitrations against Egypt, and acted before the International Court of Justice and the International Tribunal for the Law of the Sea.

There’s one more thing worth noting about Juratowitch.

His Essex Court Chambers case page lists, alongside the Indo Gold v India PCA case, another active matter: Zenith Energy v Tunisia, the ICSID arbitration I wrote about previously.

He’s simultaneously acting as counsel in both the Panthera and Zenith arbitrations — two of the most interesting resource expropriation cases in the market right now, both against sovereign states, both under bilateral investment treaties.

You don’t hire Ben Juratowitch KC if you think you might lose.

Also listed on IGPL’s team are representatives from 7 Wentworth Selborne, an Australian barristers’ chambers, including Belinda McRae and Callista Harris — appropriate given IGPL’s Australian domicile and the Australian dimension of the treaty.

India’s team is Hogan Lovells International LLP, led by Dr Markus Burgstaller, alongside P&A Law Offices in India. Hogan Lovells is a competent international firm with sovereign-side experience.

But they’re not in King & Spalding’s bracket for investor-state work, and the pairing with a domestic Indian firm suggests a structure built partly around navigating Indian government bureaucracy.

The asymmetry in legal firepower isn’t everything. India has the home advantage on facts that occurred in its territory, and sovereign states mount serious defences regardless of counsel quality.

But the quality of Panthera’s legal team — King & Spalding plus Juratowitch KC — tells you something about the confidence of those closest to the case.

The Arbitrators Three

The tribunal is composed of three arbitrators, as is standard in PCA proceedings of this nature.

The Presiding Arbitrator — whose neutrality and approach matters most — is Professor Juan Fernández-Armesto, with the remaining two co-arbitrators appointed respectively by Panthera and by India.

Fernández-Armesto is Spanish, based at his boutique Armesto Dispute Resolution in Madrid. He was previously a partner at Uría Menéndez — one of Spain’s most prestigious law firms — Chaired Professor of Commercial Law from 1988–2009, and Chairman of the Spanish Securities and Exchange Commission (the CNMV) from 1996–2000.

Since 2001 he has acted as sole arbitrator, co-arbitrator or chairman in over 200 proceedings, including over 60 investment arbitration cases, in most cases as chairman or president of the tribunal. He is a member of the Panel of Arbitrators of ICSID designated by the Kingdom of Spain, and sits on the panels of AAA/ICDR, LCIA and others.

His case history includes presiding over investment arbitrations against Venezuela (multiple), Colombia (Glencore, where he awarded $19+ million to the investor), Morocco (Carlyle Group), Romania (Energy Charter Treaty) and Mozambique among many others.

He has presided over cases where bifurcation was requested and denied — including deciding ‘not to bifurcate pro tem’ in the Rusoro Mining v Venezuela case while reserving the right to revisit the question later.

In other words, he’s an experienced operator when it comes to exactly the kind of procedural maneuvrering India is attempting here.

Professor Stanimir Alexandrov, appointed by Panthera, is Bulgarian-American and based at Sidley Austin in Washington DC.

He is one of the most prolific and experienced investment treaty arbitrators in the world, having sat in hundreds of proceedings, and is well known for a broadly pro-investor analytical approach — tending to favour expansive readings of treaty protections, jurisdiction and liability — and his appointment by Panthera is a deliberately strategic one.

He is precisely the kind of co-arbitrator an investor selects when it wants rigorous, experienced advocacy in tribunal deliberations for the claimant’s position.

Justice L. Nageswara Rao, appointed by India, is a retired judge of the Supreme Court of India. His background lies in Indian constitutional and public law rather than international investment treaty arbitration, making him a less specialist appointment than either of his fellow tribunal members.

India’s intent is clear — a jurist with sovereign instincts, likely sympathetic to state regulatory authority — but his relative unfamiliarity with the specific doctrines of investment arbitration (BIT interpretation, fair and equitable treatment, expropriation standards) may limit his influence in deliberations against two arbitrators of Fernández-Armesto and Alexandrov’s calibre.

Overall, the tribunal composition is favourable for Panthera. This is a subjective view, but I think not a controversial one.

Alexandrov is a known and highly effective voice for the investor’s position in deliberations, while India’s appointment — though defensible — is the weakest of the three in terms of investment arbitration expertise.

The presiding arbitrator is the decisive figure, and Fernández-Armesto, while scrupulously neutral, has a long track record of awarding against states when the facts and law support it.

A tribunal of this composition, presided over by one of the most experienced investment arbitrators in the world, is one in which a well-founded investor claim can expect serious, expert consideration — and one that India will find difficult to steer through procedural tactics alone.

From Notice to The Hague

Let’s walk through how we got here.

January 2024 — IGPL formally issues a Notice of Dispute to India. Under the Treaty, parties must attempt amicable settlement for six months before proceeding to arbitration.

April 2024 — No settlement in sight. The Government of Rajasthan announces the preferred bidder for the Bhukia auction. A Notice of Dispute is live on the government’s desk. They proceed anyway.

July 2024 — IGPL issues its Notice of Arbitration. The PCA case is officially commenced.

September 2024 — Both IGPL and India appoint their arbitrators. The presiding arbitrator is pending.

November 2024 — Prof. Fernández-Armesto is appointed. The three-member tribunal is fully constituted.

December 2024 — Initial tribunal hearing held. Procedural timetable and seat of arbitration agreed (London as legal seat; The Peace Palace, The Hague as physical hearing venue).

January 2025 — Terms of Appointment executed. PCA confirmed as administrator. All submissions, witness statements, expert reports and supporting documentation are confidential.

May 2025 — IGPL files its Memorial — the full statement of its case, expert reports on liability and quantum included. Damages claimed: US$1.58 billion, net of Indian taxes. Filed on time.

September 2025 — The arbitral panel orders Phase 1 to cover jurisdiction, merits and general principles of compensation together. India had applied to limit Phase 1 to jurisdiction only — a bifurcation attempt designed to delay by splitting the proceedings. The panel rejected this. Bifurcation requests are standard defensive plays in expropriation cases because a successful jurisdictional challenge can send the case to domestic courts where the state has home advantage. Not here.

October 2025 — LCM reaffirms the facility remains fully available following market speculation about its own strategic review. Approximately 50% of the facility drawn at this point.

February 2026 — India files its Counter-Memorial on schedule. The case is now in the phase where India makes its arguments.

Going forward:

One important caveat: this timetable will almost certainly change.

Seven or more procedural orders before a hearing is not unusual in cases of this complexity. There are multiple opportunities between now and December 2026 for extension requests, evidence disputes and procedural motions.

So we are very much close to a resolution (close being in the same family as soon, shortly and their best friend, imminently).

LCM’s Skin in the Game

LCM Funding — a subsidiary of Litigation Capital Management, itself listed on AIM — has committed up to $13.6 million in non-recourse financing to IGPL. Non-recourse means exactly what it says: if Panthera loses, LCM gets nothing back.

Their interests are entirely aligned with shareholders.

The facility started at $10.5 million in February 2023. After six months of due diligence — extended six separate times between May and August 2023 — LCM came back and increased the facility to $13.6 million.

By the September 2025 interim results, 63% of the facility was drawn.

In October 2025, following market nervousness about LCM’s own strategic review, Panthera confirmed LCM had explicitly reaffirmed the AFA was unchanged and the full facility remained available.

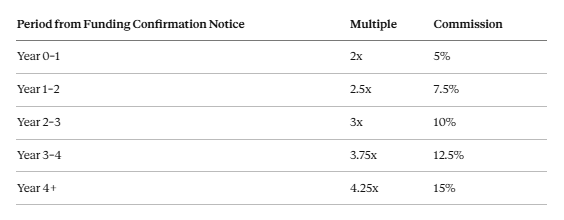

The repayment terms if Panthera wins:

LCM gets its deployed capital back first. Then the greater of:

a) Approximately $1.36 million — 10% of the total facility cap

b) A commission of 5% to 15% of damages recovered, scaling with time

c) A multiple of 2x to 4.25x of total deployed capital, also scaling with time

After year five from the Funding Confirmation Notice (August 2023), LCM additionally earns 25% per annum interest on deployed funding.

We are currently in year three.

If Panthera wins and collects in 2027-2028, LCM’s return falls in the 3x–3.75x band on total deployed capital. On $13.6 million fully deployed, that’s approximately $41–51 million back to LCM including principal. The economics for Panthera’s shareholders depend on the net award after LCM’s return and legal costs.

Even accounting for both, the residual from a meaningful award is transformative relative to the current market cap.

It’s also worth noting that LCM itself may be on the cusp of several large wins, and just needs to hang on a while longer.

What’s This Actually Worth?

Before you start dreaming of diamonds (or perhaps gold piles), remember that this is a complex international arbitration against a major sovereign state. Anyone offering false precision on the outcome is either naive or selling something.

What I can do is run a disciplined scenario analysis.

The claim: $1.58 billion

Filed May 2025, net of Indian taxes, developed with multiple legal, mining and valuation experts. The Treaty requires compensation based on market value immediately before expropriation.

GSI’s own resource estimate (7.2 million ounces of gold) at current prices gives an in-ground value running into the tens of billions of dollars.

India’s own auction attracted a buyer who committed to $120 million upfront plus 65.3% of all future production. IGPL’s 70% JV interest in a project with those characteristics being valued at $1.58 billion is not an aggressive claim.

Scenario analysis

Bear case (20% probability): No damages awarded. The tribunal finds India’s conduct doesn’t meet the treaty threshold, or rules against jurisdiction. Award: $0.

Base case (50% probability): Award at 30% of claim — $474 million — plus 3% annual interest from expropriation date (September 2023) to award date (estimated end of 2027), adding approximately $57 million. Total gross award: approximately $531 million.

Bull case (30% probability): Award at 75% of claim — $1.185 billion — plus 4% annual interest adding approximately $178 million. Total gross award: approximately $1.363 billion.

The probability assignments reflect: the bear is roughly half the historical base rate failure for funded arbitration cases, adjusted upward to reflect the strength of the facts.

The base represents a conservative outcome acknowledging that tribunals frequently apply significant haircuts to quantum. The bull accounts for a tribunal that agrees both on liability and that India’s auction provides strong market evidence for damages.

Liabilities to deduct

LCM litigation funding: on full deployment of $13.6 million at the year 3-4 multiple of 3.75x, the gross return owed to LCM is approximately $51 million. Taking the greater of the multiple vs the commission (5-15% of award), the relevant figure in the base case is approximately $80 million (15% of $531 million exceeds $51 million). In the bull case the commission at 15% of $1.363 billion is $204 million, again exceeding the multiple.

Balance sheet liabilities (provisions and payables): approximately $2.5 million.

Probability-weighted net award

Fairly simple.

(20% × -$2.5m) + (50% × $448m) + (30% × $1,156m) = -$0.5m + $224m + $347m = approximately $570 million

Against a diluted market cap of approximately $82 million (£50 million), that’s roughly 595% upside — call it 6x.

On a two-year timeline to payment — optimistic but within the procedural calendar — that’s a CAGR north of 160%.

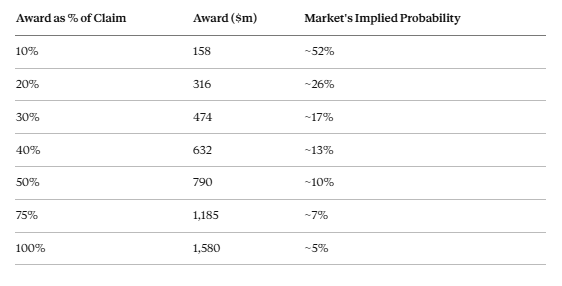

There is another way to look at it. If the diluted market cap is $82 million and the filed claim is $1.58 billion, what probability of collecting each fraction of the claim does the current share price imply?

The market is currently pricing roughly a 13-14% chance of Panthera receiving the probability-weighted award estimate. That is too pessimistic given:

the strength of the documented obstruction

India’s own auction evidence

LCM’s endorsement after extended due diligence

the calibre of the legal team

the Cairn precedent showing India will eventually pay

And here’s the kicker: a shift in market implied probability from 14% to 25% produces a 78% share price increase before a single dollar of award is received.

The case developing publicly between now and the December 2026 hearing is itself a catalyst for re-rating - and this is exactly what happened with GreenX, Emmerson and Zenith.

I predict the same here.

What happens to the cash if Panthera wins

Management have been explicit with shareholders: they acknowledge that the vast majority of the shareholder base is in the stock for the arbitration, and they intend to distribute a large portion of any award.

Board approval is required, but the CEO is supportive, and management own options rather than shares — meaning they’re incentivised to take actions that maximise share price appreciation rather than hoard cash on the balance sheet.

If the board attempts to retain the lion’s share of the cash in company, I’ll be the first man calling for an EGM, whilst wielding a pitchfork.

A conservative assumption is that 70% of the net award is distributed as a special dividend. On the probability-weighted outcome, that’s a dividend equivalent to approximately 490% of the current share price, separate from any share price appreciation leading up to the award.

The remaining 30% would fund the West African exploration portfolio — Cascades and Bido in Burkina Faso, Kalaka and Bassala in Mali.

Bido has returned 14 metres at 0.91g/t Au including 10 metres at 1.15g/t; Kalaka has a JORC-compliant inferred resource of 803,000 ounces at 0.5g/t Au. The market is currently writing these off entirely as a margin of safety measure, which seems reasonable for valuation purposes.

The Complicating Factors

There are some additional risk factors to consider, though these are all (to my mind) normal for this type of risk play:

India is a serious sovereign. This is not Tunisia. India has a $4 trillion GDP, a sophisticated domestic legal system, a long history in international legal forums and perfectly competent counsel in Hogan Lovells. They will mount a serious defence.

Jurisdictional risk is real. Jurisdictional challenges are standard defensive plays in expropriation cases. The panel’s decision to hear jurisdiction together with the merits rather than bifurcating is a mildly positive signal — they could have granted bifurcation to dispose of the case early if they thought India’s jurisdictional arguments were obviously strong. They didn’t. But the arguments themselves are confidential, and we don’t know their substance.

The timetable will slip. It always does. Seven or more procedural orders before a hearing is not unusual. Build time in. The December 2026 hearing could move to mid-2027.

Quantum is contested. $1.58 billion is IGPL’s number. India’s experts will produce very different numbers. Tribunals frequently land somewhere in the middle, and somewhere in the middle covers a lot of ground.

Enforcement is not automatic. Winning at The Hague and collecting from India are different things. The Cairn precedent is encouraging — India paid >$1 billion — but enforcement can still take years even in the best case.

LCM’s own situation. The facility has been reaffirmed, but LCM has been through a strategic review. Worth monitoring as background risk, though I am certain the best LCM-funded cases will be scooped up by competitors if the need ever arises.

The Bottom Line

Panthera Resources is pursuing a $1.58 billion damages claim against the Republic of India at the Permanent Court of Arbitration, under a clear bilateral investment treaty with an unambiguous expropriation clause, with a fully constituted tribunal presided over by one of the most experienced investment arbitrators in the world, a legal team led by King & Spalding LLP with Ben Juratowitch KC — Legal 500’s 2023 Silk of the Year for International Arbitration — as lead advocate, litigation funding from specialists who increased their commitment after six months of extended due diligence, and a hearing scheduled for December 2026.

My probability-weighted net award, across conservative bear, base and bull scenarios, is approximately $570 million against a diluted market cap of $82 million. That’s roughly 6x upside. Management intend to return the majority to shareholders by way of special dividend.

You don’t need to think Panthera will definitely win. You need to think the probability of success is materially higher than the ~14% the market is currently implying.

Remember that India can come to the table and settle at any time.

The case rests on:

India’s own geological agency confirming 7.2 million ounces of gold

20 years of documented obstruction with an extensive paper trail targeted expropriatory legislation

India’s own auction — conducted after the Notice of Dispute was served — which handed Panthera’s lawyers contemporaneous market evidence of exactly what Bhukia is worth

The case against requires believing that twenty years of obstruction, targeted expropriatory legislation and a domestic auction don’t constitute treaty breaches; or that India’s own resource estimates massively overstate Bhukia’s value; or that enforcement against a $4 trillion economy with assets across 145 convention countries somehow proves impossible.

The December 2026 hearing is the main event.

Between now and then, IGPL’s Reply in July 2026 and India’s Rejoinder in October 2026 may become partially visible, providing further catalysts for re-rating.

One way or another, this resolves well before the end of 2027.

And like all arbitration stocks, you’ve got to be in it to win it.

Hi Charles! Thanks for the excellent, clear, logical and detailed desciption of the case! If want to show a friend this oppoetunity, besides Swen Lorenz and Triple S pieces, your current writing would be that I will share.

One addition I want to highlight. Similarly to Almaden Minerals, Panthera is going to amend ita claim (probably in july in their next response, fit to the gols price move since memorial submission. In the models they calculated the sum of claim, this will definetaly result in a meaningful raise (probably to 2-2.5 bn at least).

One more potential trigger/milestone, and a factor thaat furher improves the math overall.

Great summary.

Is it also worth noting that the ceo said the 1.58bn claim reflects current gold prices.

The old claim made early In 2025 when gold was circa 3k/ oz.

He confirmed they will update the claim on the July response. So hopefully this will reflect gold prices of circa 4k+

There has also been some big M@A recently such as rupert resources. They were taken out for 500 usd an oz and the buyers noted there was a big scarcity of tier 1 gold assets ( I think theirs was only 4m oz)