Helix Exploration

they may have more helium than they realise

Good Morning Team.

I want to take a few moments of your time to catch up with Helix Exploration (LON: HEX). Shares are trading at just under 15p - 50% higher than the IPO price - but down from mid-20s highs of last quarter.

In 2024, I called Helix the best helium exploration play for the year - and the stock has never traded for under the IPO price.

The question now is this:

Is #HEX still an attractive gambit?

Let’s dive in.

Funding Secured

First up, in late January Helix announced plans to raise at least £4 million at 15p per share - it then raised around £5 million. In this market, that’s a good sign.

For context, the IPO was heavily oversubscribed back in April 2024, with most investors scaled back. Helix could have raised significantly more than the £7.5 million it initially launched with, but has now conducted this raise at a 50% increase to the IPO share price, less than a year down the line.

Chairman David Minchin, in defence of the placing, argued that:

The decision to move forward with an equity raise comes after a detailed review of the economic model and terms of available debt finance. Equity became preferable over debt considering the high cost of debt capital as well as onerous terms including long term take-or-pay agreements that would have limited the Company's ability to market produced helium to end-users and the wider USA market. In-house analysis showed a higher post-dilution NPV per share on an equity raise compared to a debt raise.’

The good news is that the debt was on offer, it just wasn’t the best path forwards in terms of investor value.

For perspective, HEX had previously noted that they preferred debt over issuing equity, but on a bottom line level, there's probably not much difference between owning a higher overall % of shares in a company which has taken on £5 million in debt, or a lower overall % of shares in a company which has issued equity to remain debt free.

But Minchin is clear that issuing the equity was in his view the right call at this juncture - and arguably, they should be able to take debt on at much more favourable terms once in production.

HEX needed access to more capital, and now has it - which leave space for a move higher - especially with the churn almost complete.

On this - share prices don’t rise before the churn is over as a general rule. Retail investors here - this is not advice - but there is nothing wrong with buying at the right time.

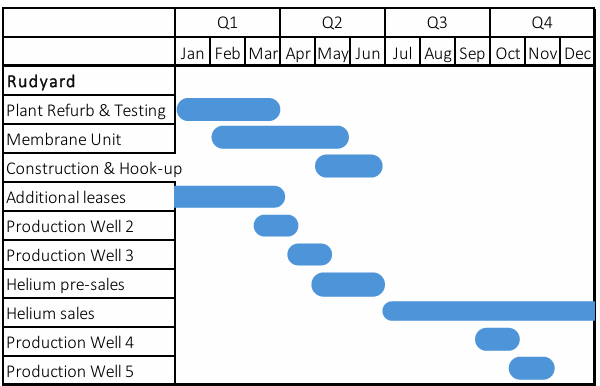

Rudyard Moves Forward

With the discovery at Rudyard, Helix has managed to buy a Xebec Helium Pressure Swing Adsorption (PSA) processing plant - to be installed at the asset. The plant cost only $500,000 (now paid in full), due to ‘management's long-term industry relationships’ - again Bo and Minchin are in tight with the right crowd.

This plant previously produced 48,000Mcf/yr of high grade helium, with 98.5% uptime when previously in use between 2015 and 2022 - which makes it good enough for HEX, especially because this should (all going well) hugely decrease time to production.

Refurbishment and installation of the plant at Rudyard will be managed by Wikota Design & Construction, a trusted strategic partner with extensive experience in gas processing and industrial infrastructure.

Bo remains ‘delighted to announce the acquisition of a proven helium processing plant, a game-changing development for Helix Exploration…This acquisition underscores our commitment to delivering shareholder value by fast-tracking our Rudyard Project into production while maintaining financial discipline.’

I’ve gone on before about how the market only cares about making money - and this plant should start delivering. Nobody cares about your magical RNS’s if there’s not a path to generating cash, either through production or an asset sale.

Helix is installing the plant close to the Darwin #1 wellhead and near to existing natural gas facilities, which should keep construction costs low - especially as roads and power run all the way to the plant gate.

Wikota has already advised that the plant is in an ‘excellent’ condition requiring only minor refitting - though anyone who has ever bought a house will know that visual surveys don’t always give a full picture.

After inspection, the plant will move to its planned location in Q2 2025, with production to follow - only front-end membrane units are needed to make this happen.

Bo has also advised that ‘results from Darwin #1 indicate that the anticline at Rudyard surpasses our expectations and is larger than previously modelled. This could represent the largest producing helium structure in the State of Montana.’

Happy days.

For context, independent consultants Aeon have advised that there are some 355 million cubic feet of helium within the northern dome alone - which could generate net revenue of some $115.2 million over a 12.5 year field life…

…representing sustained post-tax cash flow of $15-25 million per year using a flat helium price of $500/Mcf.

As a reminder, HEX’s market capitalisation stands at circa £23 million - so the upside potential is decent. For context, Aeon’s model sees an NPV of $77.9m and an IRR of more than 1,000% on reserves in the northern part of the dome.

In-house modelling goes further, with an NPV of $145m and net revenue of $220 million, but including contingent resources in southern part of dome.

Bo notes the company is now ‘fully funded to bring the Rudyard Project into production and positive cash-flow, targeting first production within Q2 of this year. Early cashflow gives Helix the freedom to pursue exploration and M&A, self-financing development and growing Helix into a strategic helium producer for the USA market.’

The company is also cashed up to drill two additional production wells at Rudyard (location surveying ongoing) - and there may also be cash left over for additional exploration. These new wells will be drilled in early Q2 - simply because it will be cheaper in a warmer season - and could amplify revenues.

Management have been on site recently, discussing power provision with the local electricity supplier, inspecting potential pipeline routes from the wellhead to the plant, and getting ready to do business in general.

And then there’s Trump’s push to secure domestic supplies of critical minerals and gases to consider - don’t rule out grant funding for production…

But perhaps most interestingly, you don’t need to rely on Helix’s word on Rudyard. I’m not even certain whether the company is aware of this, but if you delve into the National Technical Reports Library (a segment of the US Department of Commerce), and research the right keywords, you’ll find a 1977 report into Rudyard’s Helium reserves.

At Souris River, you have a historical reserve estimation of 652 million cubic feet @ 0.9%, and over two billion cubic feet @ 1.3%.

This blows both Aeon’s independent and HEX’s internal estimates out of the water - with reserves from a time where helium simply was not as strategically valuable.

And best of all? It’s already been flow-tested by Texaco back in 1960. Read the entire thing - it’s very informative.

I’ll let you do your own maths on what this means financially.

Ingomar Update

Of course, Rudyard was marketed by the company as the lieutenant to the flagship at Ingomar Dome, and work here continues.

Days ago, Helix announced acidisation of the Clink #1 well would start later this month, with re-entry and acidisation expected to complete by the end of February. This will test the capacity to stimulate flow from the limestone reservoir Charles Formation - which appears to be the most promising at present - based on

drill cuttings that demonstrated visible porosity

gas shows including helium

pulsed neutron wire-line logs indicating high reservoir quality

an interpretation of pressure build-up data from HEX’s initial flow test in November 2024.

Following an initial swabbing, a pump-in test indicated a pressure break at approximately 1,800 psi, equivalent to around 0.8 psi/ft.

The difference in pressure build-up before and after the pump-in test suggests that the induced minor fracture created a flow path to virgin reservoir - this path quickly closed, due to near-wellbore damage caused by heavy muds - but the acidisation is hoped to establish a permanent flow path.

You can then get new flow testing (and gas composition) results, by early March - and then we shall see if the juice has been worth the squeeze.

Bo notes that HEX remains ‘committed to the significant potential of Ingomar Dome, and the promising helium and hydrogen indications seen at Clink #1.’

For perspective, the company has seen 2.5% helium in the Flathead - the highest grade in Montana, and argues that Ingomar could well become ‘the first large-scale hydrogen discovery in the USA.’

55% hydrogen in gas has been isolated from mud, the highest seen in the country - so wait and see what comes next.

The bottom line

Helix is cashed up, plans to produce next quarter, has masses of helium reserves, and has near-term news-flow from Ingomar.

With the placing almost churned, and the potential to see revenue in the tens of millions of dollars, a decent move upwards may not be far off.

A further 12% down since this was published. All very interesting, but sometimes the market just doesn’t like stock. HEX much loved by retail is not popular with the markets. Genuinely don’t see this changing any time soon.