Guardian Metal Resources

The time has come.

Good Morning Team.

It’s been a while since I’ve looked at Guardian Metal Resources (LON: GMET, OTCQX:GMTL), but when you’re at record highs, why not have another look?

But as this is a bit of a read, perhaps go make yourself a nice cup of coffee, retire to your comfiest armchair and grab a biscuit.

We’re going to be here a while.

Let’s rewind the clock to early July 2023, when GMET was unlikely to be on many people’s radars - here’s a selection of questions from my Q&A at the time. It’s interesting to see just how it all played out:

2023 Questions:

2. Do you personally ‘get your hands dirty’ when inspecting new sites? Any photos?

I’m a exploration geologist by trade so I spent the first +10 years of my career in the field (getting my hands dirty). It is one thing to review a project or opportunity from your computer, but to really understand the value you need to get your boots on the ground.

4. GMET seems very underpriced compared to its potential; why is this?

I think mainly a function of listing during the summer. Many investors take time off so some of the very exciting news we are putting out is potentially not getting in front of as many eyes. I am confident we have added considerable value to the business since our IPO less than 2 months ago so we will continue to pound the table and get the message out. The market is starting to take notice now and investor interest is picking up. Regardless of the macro outlook, the need for the USA to secure domestic sources of critical/battery and defense metals is NOW – and therefore we are extremely confident as to the future of GMET.

5. Is ‘Golden Metal’ a bit of a misnomer given that you are primarily targeting Tungsten?

Yes it is. A name change is in order.

7. Infrastructure in Nevada is usually pretty good — are you close enough to other processing plants that you could pay to use?

Yes the infrastructure is fantastic – especially at Pilot Mountain. We have road/power/water access all in the immediate vicinity. There are mills/processing facilities nearby but this is typically a preferred option for smaller scale operations. We have bigger ambitions than that.

8. Are there any environmental concerns — or is this piece of Nevada essentially dead country?

Baseline environmental studies were completed by the previous owner and zero impediments to development were noted.

13. The US & Canada seem to be in a regulatory trading spat over dozens of issues from spy balloons to Taiwan. How does this help GMET’s investment case?

Only a few days ago China imposed an export ban on two rare-earth metals (both of which have military applications) – so the trade war continues to escalate. China controls 86% of the world’s total tungsten exports and are the USA’s largest import partners. As of 2026 January 1st the US Department of Defense is banning imports of tungsten from China. The USA has no active tungsten mines and Pilot Mountain is the largest undeveloped tungsten deposit in the USA. I think those few statements represent one of the more powerful and impactful investment cases you can come across at the moment.

14. You already have an off-take letter of intent with Global Tungsten & Powders. Would you prefer the sale price of your tungsten to fluctuate with the market price or be fixed price?

The price in the agreement is not fixed – it varies based on market pricing. So we still get exposure to the upside if/when tungsten prices go up.

15. The plan seems too be to secure non-dilutive funding through various grants to develop Pilot Mountain. As most of these are ‘top secret’ with no timeline attached, isn’t there risk attached there?

I wouldn’t say there is much risk. The risk is you apply and don’t get one. The reward on the other hand – is potentially significant non-dilutive funding. That is a pretty good trade-off I would say.

16. Given the US government’s loan to Ioneer which allowed it to retain 100% control of Rhyolite Ridge, do you anticipate direct support for Pilot Mountain?

I can’t comment as to how confident I am we will get support. I think based on the answer to question 14 it should be clear how strategic this asset is – but will leave it at that.

18. In a few words, why should investors find space for GMET in their portfolio when there are dozens of other small caps on the market?

The USA needs a domestic source of tungsten – and GMET owns 100% of the largest undeveloped tungsten deposit on US soil. You would be hard pressed to find a company in a much better position than this in the UK markets.

And here we are.

Shortly thereafter, in October 2023, I set out the case that tungsten would be made subject to Chinese export controls (I suspect before anyone else) - which became the case in late 2024.

In Q2 2024, I covered slides from the National Defence Industrial Association (NDIA, US-based), which effectively tells you that grant funding for a feasibility study for Pilot Mountain should be here any day now….

and this should bring you mostly up to speed.

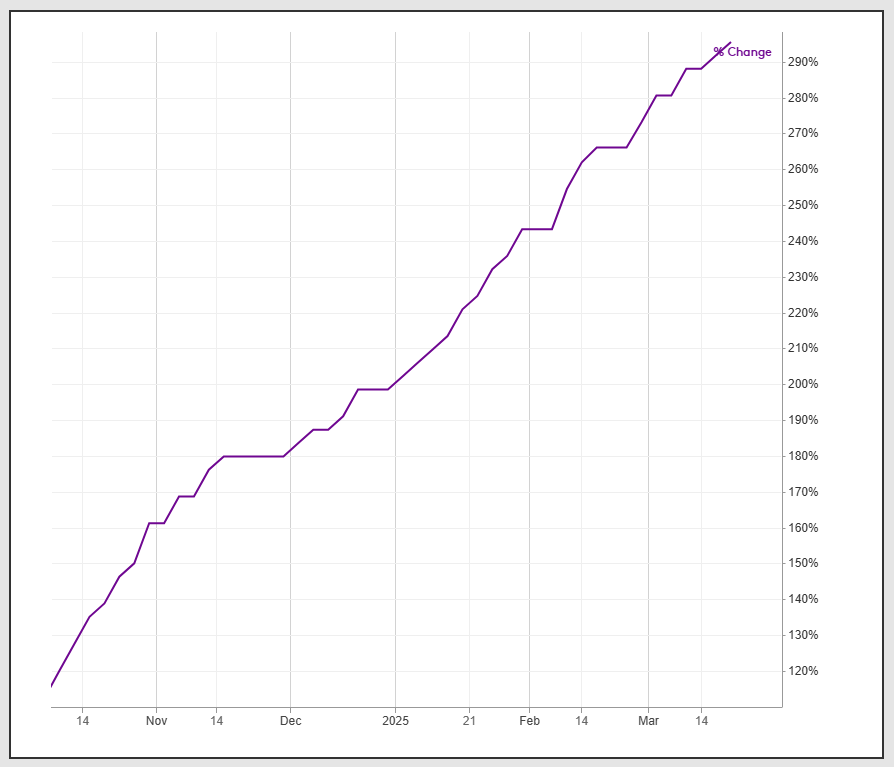

Now we’re going to consider the investment case for 2025 and beyond. For context, I’m writing this over the weekend, with Guardian having now surpassed a £50 million market capitalisation for the first time.

That’s a lovely chart.

And importantly, the £50 million market cap mark - held for a reasonable period of time - is well-known as a minimum level for institutional investment.

But it’s not like GMET is short of institutional interest.

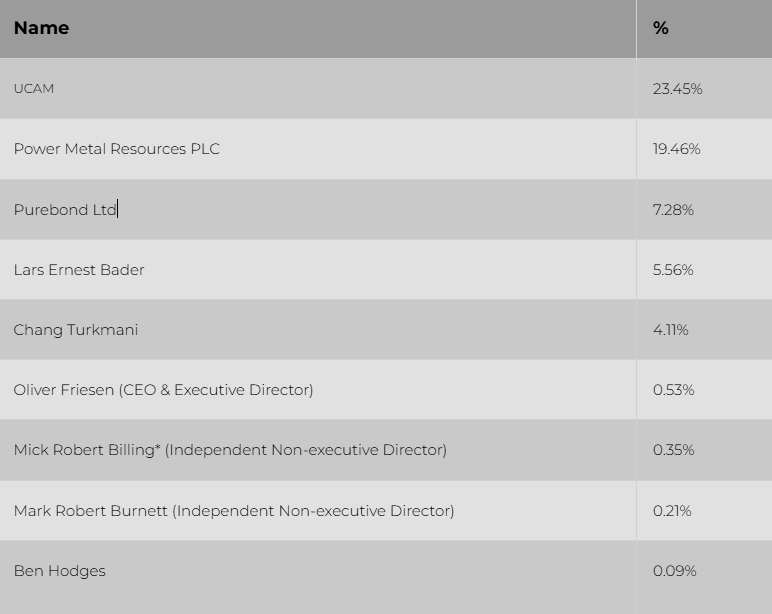

As we know, Power Metal has sold off circa 30 million shares in GMET at 31p per share to UCAM (ACAM LP - Bacon and Leslie), leaving UCAM with just under one quarter of the stock in issue, POW with just under 20%, Purebond with over 7% and various individuals also holding for gold.

It’s also worth noting that POW enjoys Rick Rule as a key shareholder, who will have made his investment at least in part for its GMET holding back in 2023 - and if there’s one thing the man knows, it’s to hold the dips for the long-term profit vision.

On POW, I am relaxed that this stock will see its day in the sun - though I know it’s been a couple of years - but this is all about Guardian.

If you want to consider the most up-to-date POW investment case in detail, consider Oak Bloke’s Herculean effort.

But what’s GMET’s investment case today?

First off, I want to set aside secondary assets: Garfield, Golconda, Kibby and Stonewall are just going to have to be put on the backburner for now. Yes, we love all our children equally but this picture from July 2024 is not representative of GMET today.

Nowadays, it’s more like this:

Upgrades people. Upgrades.

I’m not sure whether you noticed, but Sino-US tensions are well beyond simmering - Nvidia chips are on the verge of being blocked from entering China through Singapore (a backdoor designed to maintain the illusion of restrictions), while China is continuing to restrict metals to the west.

Consider the price of antimony. It’s gone a bit insane over the next few months:

Tungsten is next, because it is a sister element to antimony both by periodic table, use (defence metal), and Chinese export controls. Just wait.

And yes, Tungsten West & Greatland Gold will both stand to benefit from this too.

But GMET is uniquely positioned.

Because flagship asset #1, Pilot Mountain, is widely considered to be the largest undeveloped tungsten asset on US soil, in a country where there is no domestic tungsten production and the President is pissing off his allies like an overexcited younger sibling with one too many Risk cards.

But beyond the madcap plans to assimilate Canada, Greenland and various other countries or assets into the good ol’ US of A, the President is intent of being able to make global threats without having China (or anyone else) being able to have leverage against him:

Consider key passages:

‘The United States was once the world’s largest producer of lucrative minerals, but overbearing Federal regulation has eroded our Nation’s mineral production. Our national and economic security are now acutely threatened by our reliance upon hostile foreign powers’ mineral production. It is imperative for our national security that the United States take immediate action to facilitate domestic mineral production to the maximum possible extent.’

You could not print a more bullish statement.

Further:

(c) Agencies that are empowered to make loans, loan guarantees, grants, equity investments, or to conclude offtake agreements to advance national security in securing vital mineral supply chains, both domestically and abroad, shall, to the extent permitted by law, take steps to rescind any policies that require an applicant to complete and submit to the agency as part of an application for such funds the disclosures that are required by Regulation S-K part 1300.

I suspect agencies affected will include the Export-Import Bank (EXIM), the Development Finance Corporation (DFC), the Department of Energy (DOE), and Department of Defense (DOD), as they all play a role in securing mineral supply chains through financial instruments.

And for context, regulation S-K, Part 1300 sets SEC disclosure requirements for publicly traded mining companies, ensuring transparency in their mineral resource and reserve estimates. Companies must file a Technical Report Summary prepared by a Qualified Person and disclose annual updates on mining properties, including economic feasibility, environmental risks, and operational factors. These rules exist to provide investors with reliable, standardised data on mineral assets.

But now, they are being (to an extent) set aside in favour of speed. Trump wants critical mineral development quickly, and any red tape in the way has to go.

Or in other words, where having a PFS would have helped get grant funding and loans, this is no longer as important (if at all).

(e) Within 30 days of the date of this order, the CEO of the DFC and the Secretary of Defense shall develop and propose a plan to the Assistant to the President for National Security Affairs for the DFC to use Department of Defense investment authorities (including the DPA) and the Department of Defense Office of Strategic Capital to establish a dedicated mineral and mineral production fund for domestic investments executed by the DFC.

(f) Within 30 days of the date of this order, the President of the Export-Import Bank shall release recommended program guidance for the use of mineral and mineral production financing tools authorized under the Supply Chain Resiliency Initiative to secure United States offtake of global raw mineral feedstock for domestic minerals processing, as well as under the Make More in America Initiative to support domestic mineral production.

Domestic.

Domestic.

DOMESTIC.

And this isn’t about tomorrow, or after breakfast. It’s NOW. It’s a wake-up call to the US mining industry to wake the fuck up and get mining in the US, in as few DAYS as possible.

For context, the USA remains 100% reliant on imports for no less than 15 critical minerals. Imports make up more than 50% of US consumption for 26 nonfuel commodities.

As we all know, October 2023 saw China tighten export controls for some graphite products - and then they did the same for some rare earth magnets in December 2023.

In December 2024, we got the gallium, antimony and germanium export bans - and in January 2025 export restrictions on tungsten, indium, bismuth, tellurium and molybdenum.

Metals are being weaponised, ladies and gentlemen - and more are to follow. Meanwhile, the US Department of Commerce estimates that demand for critical minerals will rise by circa 500% in the next few decades….

and on the other side of the coin, China has just announced plans to ‘vigorously boost consumption’ and ‘expand domestic demand in all directions,’ - at least, according to Xinhua, China’s state news agency.

Ostensibly, this is with a focus on raising incomes, stabilising real estate and stocks, and improving medical and pension services. Yes, China has its own structural problems (real estate is worth circa 40% of GDP and is fucked), but the bottom line is that the trade war is well and truly on.

China plans to add to its strategic reserves of key industrial metals this year - cobalt, copper, nickel and lithium are among the metals the government plans to purchase, according to multiple reputable sites.

The National Food and Strategic Reserves Administration, which manages the country’s official commodities stockpiles, is already making price inquiries and bidding for some of these metals, while the National Development & Reform Commission — China’s top planning body, including for stockpiles — has told the country’s annual parliament that China would ‘move faster to fulfill the yearly task of stockpiling strategic goods.’

So, you have huge US demand on one hand, to import metals before Trump’s tariffs take effect in early April (also designed to increase domestic production), and thereafter to boost domestic demand to avoid tariffs with the government’s financial blessing…

…and on the other, huge Chinese demand to take advantage of the looser monetary policy.

Both massively increase metals pricing, and you can see why the US urgently needs domestic production up and running.

Even if you have a tungsten deposit in Canada, the UK or Australia, if the US needs it - then it becomes a bargaining chip.

What else do you need to hear?

Rio Tinto is going all in:

The Resolution Project has been on the backburner for 30 YEARS.

Something major has changed.

Meanwhile, Kobold (Gates & Bezos) is going in for another African play, planning to take on Manono in the DRC.

The AI billionaires know that the AI winners will be the ones with the raw materials to build data centres. It sounds hyperbolic, but the race to AGI is as critical as the race to nuclear weapons.

Who gets there first wins, and it’s going to require metal. Lots and lots of metal.

Defence, reshoring, critical minerals, tungsten.

Guardian Metals is at the centre of it all.

Yes, a couple of years ago, the investment case was to get some grant funding to get a PFS for Pilot Mountain and go from there.

Now, the plan is - with UCAM’s help and perhaps courtesy of the US government - to corner the US domestic tungsten market.

Is the CEO nervous? Watch for yourself.

Forgive my appearance - this was at the tail end of a 12 hour live shift on Australian time.

Let’s briefly consider the assets. I don’t feel the need to rehash what’s already in the RNS’s, but there are a few points I think are worth considering.

First - Guardian Metal has designated Tempiute as a co-flagship asset and as such it will be advanced and derisked towards production in parallel with Pilot Mountain, Nevada.

This feels a bit Michael & Jim to me. But regardless, Tempiute is on patented mining claims (see the full recent interview for details), but these kinds of claims basically mean this:

https://t.co/tDv8l2Mx8P\" / X")

Tempiute already has existing, usable infrastructure - loading facilities, mill & concentrate buildings, foundations, load out bays, and water pipes & pumps etc etc - and based on a 2003 appraisal for ‘internal planning and mortgage financing purposes,’ the infrastructure alone was worth $17,890,000 - and this was back in 2003 money.

Workstreams are ongoing (yes, you have to wait for details), but Friesen considers the asset ‘a game-changer for Guardian Metal.’

He goes on to enthuse that:

‘the ability to leverage existing infrastructure, including mill facilities and an operating 3,000 KW substation, provides a substantial advantage, reducing both capital costs and permitting/build out timelines.’

In other words - you want GREAT AMERICAN TUNGSTEN TRUMPY?

Then you need to copy this AI-generated video word for word and make it happen. This asset is ready to be developed if you just throw some capital at it.

Oh, and there’s a processing plat up for grabs nearby too.

Then we have Pilot.

At Desert Scheelite, other than some decent silver intersections (always good to have), we recently saw:

Drillhole PM24-034: 27.1m @ 0.46% W03, 32g/t Ag, 3,278ppm Cu & 0.71% Zn from 20.7 - 47.8m including 5.3m @ 1.08% W03, 130.5g/t Ag, 2,382ppm Cu & 0.32% Zn from 34.2 - 39.5

These are very good grades - and in depth exploration is only really getting started.

On development - I’ve done the maths on Tempiute by comparing other brownfield renovations in Nevada. You're probably looking at circa $50 million to get a sizeable operation up and running, which is much lower than a greenfield site.

Generally you have a 30/30/20 split in debt financing, equity and offtake - so maybe $15 million in dilution or £12 million, which would mean roughly 20% dilution at the current market cap.

ACAM might even front the cash. The outfit:

Took shares in Jubilee Metals at 2.25p (including warrants at a 50% premium at 3.38p) to fund the acquisition of Sable back in 2019. ACAM continues to hold 6.85% of JLP.

Invested at least £18 million into 49% of the strategic mineral JV with AEX Gold (now Amaroq) in June 2022. Check the share price action since.

Was the money behind the POW uranium JV, announced in June 2024. As an aside, they selected these licenses among thousands of others for investment, for a reason.

Recently TR-1’d in Andrada.

And also cornerstoned a $50 million investment into Mayur’s Central Lime Project in October 2024.

It has form financing these things, and is very well incentivised to do so. GMET remains in a strong financial position due to recent institutional placings and continued warrant execution shoring up the balance sheet.

And if not, there should be no shortage of suitors.

Time to bring Tungsten home.