GreenX Metals

Tier 1 Copper with BHP's blessing

Good Morning Team.

Back in April 2025, I highlighted GreenX Metals (LON: GRX) as a high-conviction opportunity.

At the time, I focused on three things: the £252 million arbitration award against Poland, strong management led by Ben Stoikovich and the Sovereign Metals veterans, and what I described as decent assets including the Tannenberg Copper Project in Germany.

Seven months on, and I’m writing this update for one reason: Tannenberg has gone from ‘decent asset’ to ‘exceptional discovery story.’

The transformation has been rapid, and I want to walk you through exactly what’s happened since April and why the stock has gone from high conviction to top play for 2026.

What’s Happened Since April

Let’s quickly talk the arbitration case - it remains materially unchanged. Poland’s set-aside motions are exactly as hopeless as they were when I wrote in April.

Prime Minister Donald Tusk himself called it ‘rather hopeless,’ noting that ‘a lost arbitration is a lost arbitration.’ The Singapore hearing for the ECT award is done and dusted.

The English courts will hear the BIT award challenge in due course. Nothing fundamental has shifted on that front, and frankly, while the £252 million + interest remains important and will eventually flow to shareholders, it’s not what makes this update compelling.

What does make it compelling is Tannenberg, and what’s emerged from German archives over the past six months.

Shallow, high-grade, historically-producing copper in the heart of European industry, backed by a government that desperately wants domestic supply and has put its money where its mouth is with a €1 billion fund to prove it.

GreenX has just found 728,000 tonnes of contained copper sitting in 1940s archives that everyone forgot existed for eighty years.

The Archive Detective Discovery

In September, GreenX announced something extraordinary.

They’d found records for 95 drillholes from the 1930s, holes drilled by the Nazi government between 1935 and 1938 as part of a systematic exploration campaign to establish domestic copper supply ahead of the Second World War.

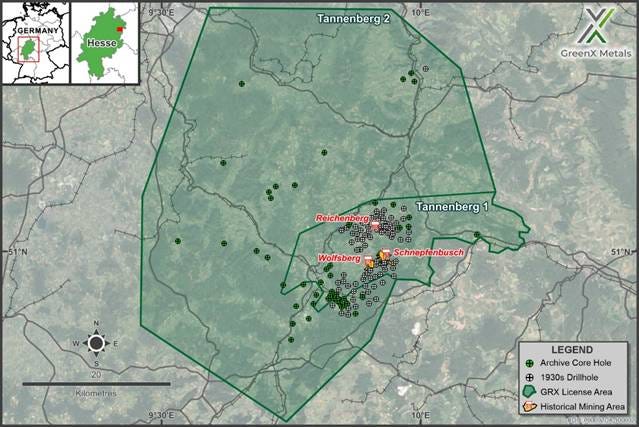

These 95 drillholes formed the geological basis for opening three major underground copper mines within what is now GreenX’s licence area: Reichenberg, Wolfsberg and Schnepfenbusch.

These mines, collectively known as the Richelsdorf Mining District, operated successfully and produced substantial copper and silver until the 1950s. The drilling was conducted by Mansfelder Kupferschieferbergbau AG, known as Mansfeld AG, which was essentially the consolidated German copper mining expertise of the era.

This was the best geological and mining knowledge Germany possessed at the time, focused on a strategic objective.

The drilling campaign tested two concepts.

In the southern area, holes tested the downdip continuation of known Kupferschiefer mining sites from the mid-1800s, which led to the opening of the Wolfsberg and Schnepfenbusch mines. In the northern area, the drilling discovered previously unknown down-faulted Kupferschiefer that doesn’t outcrop at surface and had never been exploited.

This discovery led directly to the opening of the Reichenberg mine.

To date, GreenX has recovered original detailed geological documentation for 43 of these 95 holes, including lithological descriptions, stratigraphic interpretations, and comprehensive data that would cost millions to recreate today. They’ve found historical assay results for 35 of the holes, covering copper, silver, lead and zinc, with additional sporadic assays for nickel, cobalt, molybdenum and vanadium.

Then in October, the company announced they’d found something even more valuable in those archives: a 1940 Historical Estimate prepared by Mansfeld AG showing 728,000 tonnes of contained copper at an average grade of 2.6% copper.

That’s over 1.6 billion pounds of copper at grades that would make any modern explorer cry tears of joy.

And this wasn’t speculative.

This estimate was based on actual drilling, cross-checked against production grades at the Wolfsberg and Schnepfenbusch mines that were operating at the time. Mansfeld AG compared their drill assays to the actual mining grades and found favourable correlation, so they used the exploration hole data with confidence.

The estimate covers four zones: Ronshausen in the south with 463,000 tonnes of contained copper, Hönebach with 130,000 tonnes, Wolfsberg with 93,000 tonnes and Schnepfenbusch with 66,000 tonnes.

Mansfeld AG made specific adjustments to account for sterilisation, omitting 250,000 tonnes of contained copper where surface features might prevent mining. They also subtracted 23,793 tonnes of contained copper that had already been extracted by mining at Wolfsberg and Schnepfenbusch at a production grade of 2.2% copper.

This is a solid estimate by the standards of 1940, and GreenX has reviewed the original records covering 17 of the 18 holes used in the calculation with no discrepancies found.

Now here’s the critical question: how did this information get lost?

The answer lies in the Cold War.

After World War II, Germany was partitioned into East and West.

The Richelsdorf mines ended up in West Germany, just over the border from what became East Germany. But the administrative centre for the mining district, along with much of the geological knowledge and records, ended up in neighbouring Thuringia, which became part of the German Democratic Republic, the communist state that existed from 1949 to 1990.

The Mansfeld copper mining district itself, where Mansfeld AG was based, also ended up in Soviet-controlled East Germany. For over forty years, the Iron Curtain ran right through this story.

The mines were in the West.

The data was in the East.

And for 80 years, nobody put the two back together.

GreenX is now conducting an expanded archive search in out-of-state archives from the former East Germany and in private collections. These documents likely haven’t been looked at since they were archived decades ago. The Company is systematically digitising everything they find and integrating it into their geological database and 3D models.

The magnitude of this discovery cannot be overstated.

Drilling 95 holes today would cost over €25 million and take several years given modern permitting requirements in Germany.

GreenX has effectively been handed a decade of work and tens of millions in drilling data for the price of some diligent archive searches.

1984 Validation: St Joe Exploration Confirms the Model

Historical estimates are valuable, but modern geologists quite rightly want validation before getting too excited. Fortunately, there’s a second historical estimate that provides exactly that validation.

Between 1980 and 1984, an independent company called St Joe Exploration conducted limited drilling at Tannenberg. They focused on just a portion of the Ronshausen zone, covering only 28% of the area included in the 1940 Historical Estimate for that zone.

Based on 14 holes, St Joe estimated 169,000 tonnes of contained copper and 6.5 million ounces of contained silver at grades of 2.1% copper and 25 g/t silver.

What makes this significant is that St Joe benefited from both technological advancement and enhanced geological understanding in the 40 years following Mansfeld AG’s work.

They assayed wider intersections and found that the mineralisation was up to 3.45 metres in width. Their historical estimate used thicknesses between 1.5 to 2 metres, considerably thicker than the narrow Kupferschiefer that Mansfeld AG had focused on in 1940.

This is crucial because it points to the fundamental limitation of the 1940 Historical Estimate: it was based on an outdated geological model that believed copper mineralisation was syngenetic and restricted to the thin Kupferschiefer shale horizon, typically just 20 to 60 centimetres thick.

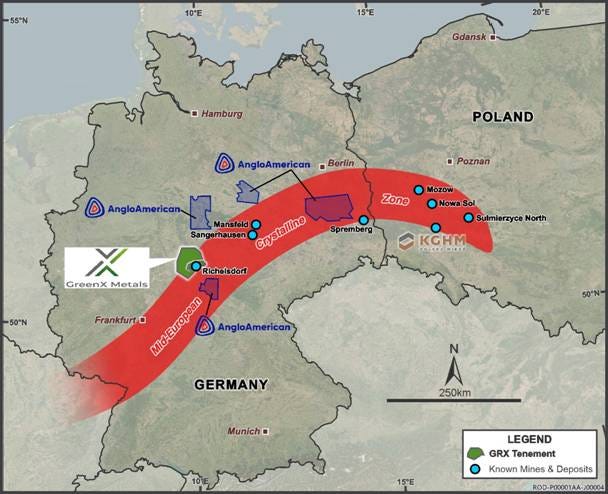

We now know this model is wrong. Modern understanding of Kupferschiefer systems, demonstrated extensively at KGHM Polska Miedź’s operations in Poland, shows that copper mineralisation is epigenetic and can extend up to 30 metres above and 60 metres below the Kupferschiefer horizon.

The shale itself often contains only a small fraction of the total copper. Up to 95% of mineable copper can be hosted in the footwall sandstone and hanging wall limestone.

KGHM, by the way, is the ninth largest copper producer globally and the second largest silver producer, with a market capitalisation of €9.2 billion. In 2024, they produced 730,000 tonnes of copper and 43 million ounces of silver from Kupferschiefer deposits.

Their operations are located on the same geological structure as Tannenberg, which we’ll come to in a moment.

So when St Joe found thicker mineralisation and included silver credits that Mansfeld AG had completely excluded from their 1940 estimate, they were providing validation of two things: first, that the 1940 grades were accurate; and second, that the true mineralisation is significantly larger than the 1940 estimate captured.

Given that St Joe drilled only 28% of one zone and still found 169,000 tonnes of contained copper with significant silver credits, the implications for the other zones in the 1940 Historical Estimate are substantial. The exploration upside is considerable.

Modern Assays: November Results

Historical estimates and archive discoveries are fascinating, but what really matters to modern resource geologists are modern assays conducted to current QAQC standards.

In November, GreenX delivered exactly that.

The Company has been systematically re-logging and re-sampling 47 archived drill cores from holes drilled in the 1980s. These cores have been stored for 40 years by the Hessisches Landesamt für Naturschutz, Umwelt und Geologie, the Hessen state authority responsible for preserving geological assets for future explorers. The core was found to be in excellent condition.

GreenX transported the core to Palsatech in Sala, Sweden, a specialist mining industry facility with established best-practice procedures. Analysis was performed at SGS in Ankara, Turkey, an ISO/IEC 17025 accredited laboratory. The Company implemented its own Quality Assurance and Quality Control program to ensure results meet JORC Code standards.

In November, they released results from six of the 47 holes where over 90% of the historical core was available over the target sample interval. The results were exceptional.

Ro 23 returned 1.5 metres at 2.7% copper and 55 g/t silver from 366 metres depth. This is high-grade copper by any standard, with silver credits that add meaningful value.

Ro 45, located near Nentershausen to the north of the main historical estimate area, intersected 2.4 metres at 1.4% copper and 18 g/t silver from 268 metres depth. Ro 25 hit 1.0 metre at 2.0% copper and 41 g/t silver from 533 metres.

Ro 17 delivered 1.3 metres at 1.2% copper and 24 g/t silver from 481 metres. Ro 15 intercepted 3.7 metres at 1.2% copper and 17 g/t silver from 286 metres.

And Ro 38 returned 1.8 metres at 0.7% copper and 15 g/t silver from 536 metres.

These results confirm several critical things.

First, the historical grades from the 1980s work were accurate, and in some cases modern assays show slightly better grades.

Second, the mineralisation is demonstrably thicker than just the narrow Kupferschiefer shale. Intercepts ranging from 1.0 to 3.7 metres significantly exceed the maximum thickness used in the 1940 Historical Estimate.

Third, silver is consistently present at economically meaningful grades across all holes.

Most importantly, these holes are located up to 12 kilometres apart, demonstrating genuine scale. This is a district-scale mineral system.

And this is just six holes out of 47 in the program. Of those 47 archived cores, 18 holes have never been assayed at all. They represent completely untested copper potential. The remaining 29 holes have limited historical assaying, typically focused on just a narrow 5-metre interval across the Kupferschiefer shale, leaving the broader mineralised zones in the footwall and hanging wall completely untested.

GreenX is continuing the core logging and sampling program through Q1 2026.

Every set of results has the potential to expand the known mineralisation or discover entirely new zones.

BHP Endorsement

Let’s now consider BHP Xplor, because this matters more than people realise.

In January 2025, Tannenberg was selected as one of eight early-stage exploration projects globally for BHP’s 2025 Xplor accelerator program.

This is a $500,000 grant, in-kind technical assistance, mentoring, access to BHP’s global networks and partnerships and a program explicitly designed to fast-track critical minerals discovery and development aligned with the global energy transition.

The field of applicants was extremely strong. Successful applicants had to demonstrate that their projects were not only geologically compelling but also innovative in their approach to data and exploration.

According to Marley Palin, BHP’s Head of Xplor, GreenX stood out on both counts.

Since January, BHP has directly funded and collaborated on every major piece of work at Tannenberg. The airborne magnetic and radiometric survey flown in May, covering 58 square kilometres over the historical Richelsdorf Mining District, was 100% funded by BHP Xplor.

The historical core re-logging, re-assaying, and hyperspectral scanning program is being funded by BHP Xplor.

The reprocessing of archived geophysical data and collation of historic mining and production data are all part of the BHP-supported work program.

BHP extended the Xplor program to 31 October 2025 to allow for completion of this work. They’re actively involved in designing surveys, interpreting results, and planning next steps.

Now, it’s worth noting that Xplor often comes with strings. There can be limited exclusivity provisions, pre-emption rights, and data-sharing arrangements. But these are standard for such programs, and many Xplor projects go on to receive significant financial backing from BHP.

The majors have decided that exploration is no longer worth their time on a standalone basis, but they’re very interested in backing projects that de-risk through early-stage work.

The endorsement from BHP matters because it signals to the market that serious technical people with decades of experience in finding and developing copper deposits think Tannenberg is worth backing.

That’s not nothing.

Geophysics Breakthrough

In September, GreenX released results from the airborne magnetic and radiometric survey.

The survey covered 58 square kilometres over the Richelsdorf Mining District, flying 660 line-kilometres with high-resolution data collection at 100-metre line spacing. This was the first modern exploration work at Tannenberg in four decades.

Advanced processing techniques including analytic signal, tilt derivative, and reduced-to-pole transforms were applied to extract maximum geological information from the dataset.

The survey identified two large amplitude magnetic anomalies. Combined with reprocessed residual gravity data showing a northeast-southwest striking gravity high, GreenX’s geologists concluded that these anomalies represent deep volcanic rocks within an uplifted basement block beneath the historic mines.

This matters because it means the Mid-European Crystalline Zone, known as the MECZ, underlies the historic mines.

The MECZ is a belt of very old rocks running across central Germany and into western Poland. These rocks include ancient granites, volcanic rocks, and sediments that were metamorphosed during the Variscan orogeny about 300 million years ago. In some places like the Odenwald south of Frankfurt, the MECZ is visible at surface.

At Tannenberg, it’s buried under much younger sediments.

Here’s why this is critical: the consensus in European Kupferschiefer research is that the MECZ basement and intra-basinal volcanic rocks are the source of the copper and other metals in these deposits.

When a mineral deposit forms, you need a source of metals through which fluids move to scavenge the copper. These fluids then redeposit the metals higher up within sedimentary rocks. The MECZ provides that source.

Every major Kupferschiefer deposit in Germany and Poland is associated with the MECZ. KGHM’s massive Polish operations sit on it. The historical Mansfeld district in Sachsen-Anhalt sits on it.

And now we know with certainty that Tannenberg sits on it.

While the major geophysical anomalies identify the source of the copper, other patterns in the magnetic data reveal faulting that could have provided pathways for upward movement of the metal-bearing fluids. These structures are hidden below the deepest drilling known to date and represent an important advancement in understanding the deep geological architecture.

Most importantly, the anomalies and faults extend well beyond the boundaries of the survey area. They extend to the east into Tannenberg 1 and toward both the north and southwest into the new and larger Tannenberg 2 licence area, which covers 1,628 square kilometres and was granted in early 2025.

This means the exploration potential is far larger than anyone previously understood. The geophysics has just opened up the entire 1,900 square kilometre licence package as prospective for significant copper-silver mineralisation.

Scale, Infrastructure and the Dream Team

The sum of all these parts is greater than the individual discoveries.

They have 142 historical drillholes across two databases: 95 from the 1930s National Socialist campaign and 47 from post-1970s exploration. They have three fully documented underground mines with unprecedented sample density, including over 15,000 unique grade records from the Reichenberg mine alone. They have detailed mine plans, thickness measurements throughout the workings, and comprehensive information about geological structures and stratigraphy.

They have a 1940 Historical Estimate showing 728,000 tonnes of contained copper that was based on an outdated geological model and excluded silver entirely. They have a 1984 validation showing thicker mineralisation and significant silver credits. They have modern 2025 assays confirming grades and demonstrating intercepts up to 3.7 metres thick with consistent silver mineralisation.

They have geophysics confirming the MECZ source structure beneath the project and extending the prospective area across nearly 2,000 square kilometres. They have BHP as an active technical partner funding accelerated exploration.

They have shallow mineralisation from surface down to 500 metres depth in the Richelsdorf District, significantly shallower than other Kupferschiefer projects. They have excellent infrastructure in central Germany with road and rail access, established industrial base, and a mining-friendly regulatory environment.

And they have the Sovereign Metals management team running it. Ben Stoikovich as CEO. Sapan Ghai, Ian Middlemass, Mark Pearce, Dylan Browne all featuring on GreenX’s website.

These are the same people building Kasiya into a monster. Management competence remains the number one most important feature in any investment case, and this team has proven they don’t waste shareholder capital.

This is not an early-stage exploration play run by people who’ve never built anything. This is a brownfields redevelopment of a historically-producing district run by some of the best operators in the junior mining space, backed by BHP, with 80 years of forgotten data suddenly available.

European Copper Crisis

Copper in Europe in 2025 is not just another commodity. It’s a strategic crisis.

Germany is the largest copper consumer in Europe. The country’s entire industrial base, from automotive manufacturing to renewable energy infrastructure to defence production, depends on reliable copper supply. Yet Germany produces almost none of its own copper.

Europe as a whole produces only 3.6% of world primary copper supply. Over 80% of Europe’s refined copper requirements are imported.

Global copper demand is projected to rise over 40% by 2040 driven by electrification, renewable energy, electric vehicles, data centres, artificial intelligence infrastructure, and defence applications. Wood Mackenzie and Morgan Stanley both forecast structural deficits.

Only three Tier-1 copper discoveries have been made since 2010: Kamoa-Kakula, Cascabel, and Filo del Sol. Ore grades are falling globally. Permitting is slow. The world needs 80 new copper mines by 2030 just to meet baseline demand.

Europe has recognised this problem and acted. In May 2024, the EU Critical Raw Materials Act came into force, legally binding across all EU member states. The CRMA designates copper as a Strategic Raw Material. Projects that receive Strategic Project designation can access fast-track permitting of 27 months or less, compared to the typical decade-plus timeline for new mines.

This is not symbolic. This is the EU fundamentally reorienting its approach to resource security. The policy shift is from passive regulation to proactive support. The EU is now actively incentivising domestic mining, exploration, and processing.

Germany has gone further. In 2024, the German government launched a €1 billion KfW Raw Materials Fund specifically to support early-stage financing of mining and processing projects that secure raw material supply for German industry. This represents a fundamental policy shift.

Germany is now focused on active facilitation of responsible mining and financing with the explicit goal of strengthening supply-chain resilience and reducing dependence on external exporters, particularly China.

Stefan Wintels, Chief Executive Officer of KfW, stated in February 2024 that ‘access to critical natural resources is strategically important for our country and Europe and a necessary prerequisite for our competitiveness. Strengthening the resilience and sovereignty of Germany and Europe is one of KfW’s strategic action areas in this decade.’

Projects like Tannenberg, located in Hesse in the heart of German industry, with shallow copper-silver mineralisation in a historically-producing district, are exactly what this policy framework was designed to support.

Add to this the defence dimension. Modern warfare is reshaping metals demand. Fighter jets, submarines, drones, tanks, ammunition, sensors, communications systems—all require enormous amounts of copper. Defence demand is rising 14% annually. The United States and NATO are scrambling to secure domestic supply chains for strategic metals.

Copper is at the top of that list.

Tannenberg is not competing with projects in remote jurisdictions with no infrastructure and hostile regulatory environments.

Tannenberg is in Germany, in a proven mining district, with full government support and capital available to bring it into production.

The timing couldn’t be better.

What Happens Next

GreenX has been clear about the path forward. They’re completing the 47-hole historical core program with results continuing through Q1 2026.

They’re systematically digitising and integrating the 1930s drill database into 3D geological models.

They’re planning a twin drilling campaign to verify the historical estimates and establish a mineral resource estimate in accordance with the JORC Code.

They’ve just exercised the option to acquire 90% of Group 11 Exploration GmbH, the private German company that holds the Tannenberg exploration licences.

Under the earn-in agreement announced in August 2024, GreenX had until 31 December 2025 to elect to acquire 90% of Group 11. They’ve made that decision.

They’ll pay A$3 million in GreenX shares to the vendors, with the vendors’ 10% interest free-carried until completion of a feasibility study.

They’re also investigating applying for EU Strategic Project status under the CRMA, which would provide fast-track permitting and access to additional funding mechanisms.

The next major catalysts are clear: continued assay results through Q1 2026, completion of the 3D geological modelling, announcement of a drilling campaign to verify historical estimates, and potential Strategic Project designation.

The Greenland Pivot: Antimony and Tungsten Come Into Play

One other material development since April: GreenX has made strategic decisions about its project portfolio.

They’ve withdrawn from the Arctic Rift Copper Joint Venture in Greenland, recognising a A$7.77 million impairment. This is the right decision. Capital is finite, and Tannenberg is the flagship asset that deserves full focus.

However, they’re retaining 100% of the Eleonore North Project in Greenland by issuing A$1 million in GreenX shares. Why? Because Eleonore North has suddenly become a lot more interesting.

The project hosts outcropping gold and high-grade antimony mineralisation at the Noa Prospect, with potential for a reduced intrusion-related gold system analogous to large bulk-tonnage deposits like Donlin Creek and Fort Knox in Canada. Historical specimens have graded up to 23% antimony, with other samples up to 4 g/t gold. A 14-metre chip sample graded 7.2% antimony and 0.53 g/t gold. Antimony mineralisation has been identified along a 4-kilometre trend that aligns with gold veining at surface within a 15-kilometre trend.

But what makes Eleonore North compelling right now is the Margeries Prospects, where historical estimates show 83,000 tonnes of mineralised rock at 4.6% antimony at North Margeries, 58,000 tonnes at 3.2% tungsten at South Margeries, and 32,000 tonnes at 1% tungsten at North Margeries.

Both tungsten and antimony are on the USA and EU critical raw materials lists. Both have experienced dramatic price increases over the past year due to Chinese export restrictions. Antimony has gone from $5,000-10,000 per tonne historically to $60,000 per tonne today.

China controls about 50% of global antimony mining and most downstream processing. In September 2025, the US Defence Logistics Agency awarded US Antimony Corp an exclusive contract for up to $245 million to supply antimony metal ingots for the national defence stockpile. In October 2025, JPMorgan announced a $75 million investment in Perpetua Resources’ Stibnite gold-antimony project in Idaho from its $1.5 trillion fund for US national security.

Tungsten is similarly strategic. About 90% of global tungsten comes from Russia, China, and North Korea, with China alone accounting for 80% of output. The US has had no domestic tungsten production since 2015. In February 2025, China announced sweeping export controls on tungsten and other metals used across defence, clean energy, and industry.

GreenX will conduct field mapping and sampling at Eleonore North in 2026 to ground-truth targets and identify drill targets. They’ll collect bulk samples for both tungsten and antimony metallurgical testwork. Over 2,000 metres of historical core still exists in Greenland archives and is available for inspection and sampling.

This is the right portfolio decision. Tannenberg remains the flagship and gets primary focus and capital allocation. But retaining Eleonore North for A$1 million in shares provides strategic optionality on two of the hottest commodities in the critical minerals space right now.

Why I Remain Convicted

Here’s what you need to understand: this story has fundamentally transformed since April.

In April last year, I liked GreenX for three reasons. The arbitration award provided a £252 million floor value. The management team from Sovereign Metals provided confidence in execution. And the assets, particularly Tannenberg with BHP Xplor backing, provided upside optionality.

The arbitration? Still there. Still growing.

£252 million. That’s the number. It was the number in October 2024, and it’s still the number now.

But numbers that accrue interest at SONIA plus 1% compounded annually don’t stay still.

Since the award was made in October 2024 through the end of December 2025, approximately £17 million in additional interest has piled on. And it keeps compounding — every year Poland doesn’t pay up, add another £14 million to the tab.

(Of that £252 million total, about £183 million comes specifically from the ECT award, with payments under the BIT award offset against it. But we’re getting into the weeds.)

Poland tried.

Poland failed.

On 9 January, the Singapore International Commercial Court did something Poland really didn’t want it to do: it rejected their set aside application.

In its entirety.

Poland had challenged the ECT award on jurisdictional grounds. They claimed procedural unfairness in how damages were calculated.

The Singapore Court looked at all of it and said:

NO.

This matters because the threshold to overturn an arbitration award is very high. Singapore courts — like most courts dealing with international arbitration — reject set aside applications in the vast majority of cases.

Poland is also trying to set aside the BIT award in English courts. That motion was filed in late 2024. Same uphill battle, and as English and Singaporean legal systems are so similar, it’s a foregone conclusion.

What happens when Poland pays?

The same thing that was always going to happen: GreenX returns most of the cash to shareholders.

That plan hasn’t changed. What has changed is that it’s looking increasingly inevitable.

The management remains. Stoikovich and the Sovereign team continue to execute with the same competence they’ve demonstrated at Kasiya. That hasn’t changed.

But Tannenberg has changed completely.

What was an interesting early-stage exploration opportunity backed by BHP has become a genuine redevelopment of a historically-producing brownfields district with 728,000 tonnes of contained copper in a 1940 Historical Estimate, modern assays validating and exceeding historical grades, geophysics confirming the MECZ source structure beneath the project, 142 historical drillholes providing tens of millions of euros worth of exploration data, and the most supportive policy environment for domestic copper mining that Europe has seen in decades.

Tannenberg could be a genuinely significant European copper-silver discovery. KGHM has a market capitalisation of €9.2 billion producing 730,000 tonnes of copper per year from Kupferschiefer deposits on the same geological structure as Tannenberg. If GreenX can establish even a fraction of that scale through this year’s drilling and establish a JORC-compliant resource, the re-rating will be substantial.

The free money from the arbitration will come.

But increasingly, that feels like a bonus rather than the main event.

Charles, great job, as always!

One more thing, yesterday Marcin Michalek found in danish archives plans for mines in Eleonore North. And they say it is possibile to do it in 6-18 months!

Great post as usual.

So the arbitration payout (assuming it comes) is greater than the company's current market cap? Assigning a value of (less than) £0.00 to it's other assets? Am I reading that correctly?