GreenX Metals

Three reasons to buy, and one to avoid

Good Morning Team.

I want to highlight a new opportunity that you should all have on your radars - and potentially within your portfolios. As ever, this is not financial advice.

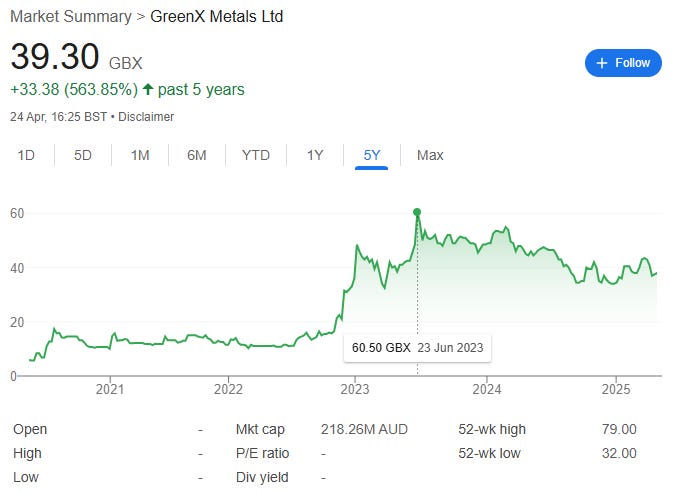

GreenX Metals (LON: GRX) has already seen some significant gains - up >500% over the past few years - but there are in my view more rises ahead.

Here’s three reasons why:

1. MONEY MONEY MONEY

On 8 October last year, GreenX won compensation and interest across two awards worth £252 million in arbitration against Poland under the Australia-Poland Bilateral Investment Treaty and the Energy Charter Treaty, within the bounds of the United Nations Commission on International Trade Law Rules.

As the market capitalisation comes in at just north of £100 million, I imagine the mathematically blessed among you might have already worked out the potential upside.

Oh, and interest will continue to accrue at SONIA +1% compounded annually until full and final payment.

The Tribunal unanimously held that the Republic of Poland had breached its obligations under the Treaties in relation to the Jan Karski project.

All GreenX costs are being funded to the tune of A$18 million on a non-recourse basis from Litigation Capital Management - and they are being represented by ‘the Boys’ - Boies Schiller Flexner, alongside international disputes firm Lalive.

These guys don’t lose. See also Emmerson - my moonshot for 2025 - which is seeking similar compensation with support from the same law firm.

It’s worth noting that Polish media had reported that the company could seek as much as 10 billion zlotys ($2.64 billion) in compensation, so this is arguably already a ‘win’ for both sides.

It’s literally dime on the dollar.

But of course, Poland has lodged a set aside request for the awards, though importantly, this is not an appeal.

A set-aside motion is basically a cousin to judicial review, and similar arguments apply to both: procedural impropriety, illegality, irrationality, or legitimate expectation.

If you don’t know what these are, then you never did a law degree and are blessed in ways you cannot imagine.

But basically, the threshold - whether in Singapore or England - where one award each will be examined, is extremely high. Pretty much all set-aside motions are lost.

It’s like when Federer won that incredible Australia Open in 2017 against Nadal - Nadal used a Hawk-Eye challenge when it was clear Federer had won the match, because, honestly…

Why not?

But the challenge was hopeless, and so is Poland’s.

Polish Prime Minister Donald Tusk, upon the set-side news noted that:

‘The case is rather hopeless, because a lost arbitration is a lost arbitration. We have two big cases on our shoulders. The PiS government blew this issue.

The Australians, as you know, were promised that their mine would be built there. For years they were misled and later the commitment was withdrawn. It was quite obvious that they would go to arbitration, and it was rather obvious that they would win this arbitration.

Speaking frankly, I would most likely, and I cannot exclude that it will go this way, to find the person directly responsible for Poland now having to pay well over a billion zloty if we do not find a legal solution - which I think has very little probability to set aside the award in this arbitration. So, speaking the truth, I will expect my officers to inform the public in the coming days who made a decision or refrained from making a decision with the consequence of these gigantic losses, that is the compensation that we as the Polish State must pay to the Australians.’

So why challenge really?

Because it allows Poland to go to the Boys and offer a settlement in exchange for not dragging it out for as long as possible. Would you take 80% of the settlement to be paid in cash tomorrow?

Maybe, but it’s already a dime on the dollar judgement - and only one project misled on was awarded for.

Plus, it’s worth noting that as of mid-January, another £3.2 million in interest had accrued.

But the most important thing to ‘get’ is this:

‘Upon satisfaction of the award, it is GreenX's intention to return the majority of the available cash to shareholders.’

Once the set aside motions are dismissed (the BIT award in England and the ECT award in Singapore), the stock is going to double overnight.

This is a high conviction play for me.

2. Project Superiority

But the free money isn’t all.

GreenX has some fantastic assets - most importantly, the Tannenberg Copper Project in Germany - which was recently selected for the BHP Xplor 2025 program.

Yes, even if there are not strings, there are always strings (limited exclusivity, pre-emption, and data-sharing rights).

But $500,000 in grant funding helps, as does the association with the FTSE 100 major. It’s worth noting that many of the Xplor projects go on to receive significant financial backing from the major; this is not just a gimmick, even if the majors have decided exploration is no longer worth their time.

The cash is to be used over a six month period from 6 January 2025, so the start of Q3 could see BHP get really serious.

As a reminder, Xplor offers in-kind technical assistance, mentoring and access to BHP’s global networks and partnerships, and ‘is designed to fast-track critical minerals discovery and development aligned with the global energy transition.’

Can anyone say EU strategic project status?

Geophysics across the license area, which hosts historically producing copper mines and multiple high-grade drill intercepts is ongoing.

CEO Ben Stoikovich enthuses:

‘This is an exciting opportunity for GreenX and a strong endorsement of the exploration potential of the Tannenberg project. Kupferschiefer-style deposits are globally significant, and the historical mining and drill data at Tannenberg indicate the potential for shallow, high-grade, and large-scale copper and silver discoveries. We are pleased to be recognised by BHP, a global industry leader, and look forward to working closely with their team.’

Marley Palin, BHP’s Head of Xplor acknowledges that:

‘The field of applicants for BHP Xplor was extremely strong this year. Successful applicants had to demonstrate that their projects were not only geologically compelling but also innovative in their approach to data and exploration. GreenX stood out on both counts.’

Yeah I’m not surprised given who’s in charge - we’ll get to that in a minute.

GreenX has also just expanded the project area sevenfold from 272 km² to 1,900 km² with the addition of a second exploration licence, Tannenberg 2, which covers 1,628 km² and is valid for an initial three-year term, extendable under German mining law. The original licence, Tannenberg 1, has also been renewed for an additional three years.

Historical intercepts within Tannenberg 2 include 0.69 metres at 3.1% copper and 31.7 ppm silver from 378 metres depth, and 2.2 metres at 0.9% copper and 23.1ppm silver.

BHP Xplor are fully on board, directly supporting the accelerated development of the expanded Tannenberg area.

Upcoming work programs include airborne magnetic and radiometric surveys, additional ground gravity data collection, relogging and reassaying of archived drill core, and comprehensive collation of historical geophysical and mining data. The first phase of magnetic data collection is ongoing, with core relogging and data integration continuing through the summer.

This thing is just getting started, and I am confident we will see great things.

Greenland Exploration Projects

GreenX also continues to advance its two major critical mineral exploration projects in Greenland: the Eleonore North and Arctic Rift Copper Projects.

If you’ve read my commentary on Amaroq, you will know I am 100% pro-Greenland, and these assets are hype.

This is the new frontier for critical minerals and the US, China and Russia knows it.

At Eleonore North, the company recently received outstanding results for antimony, which is rocketing to new highs due to the Sino-US trade war. For perspective, antimony and tungsten were also recently designated as critical minerals by both the US and EU, with NATO classifying tungsten as defence-critical.

See also: GMET. Tungsten was a clear win years ago.

High-grade antimony veins, including grab samples grading up to 23% Sb, and additional samples returning up to 4g/t gold have been reported back already, while mineralisation has been traced along a 4km trend that aligns with a broader 15km gold-bearing structural zone.

Ongoing review of radiometric and historical data is expected to further refine exploration targets.

Then there’s the Arctic Rift Copper Project, which covers a vast 5,774 km² licence area and is highly prospective for large-scale copper mineralisation across multiple geological settings.

GreenX has assembled an enhanced technical team, including a specialist geologist based in Scandinavia, to lead its exploration program design and analysis. Remote sensing techniques are currently being evaluated to support data interpretation and the planning of follow-up exploration work.

3. Dream Team

Here’s your last reason to buy: the company is run by the dream team - a crack squad of elite junior resource specialists who are not shit at their jobs.

I know - amazing right?

CEO is Ben Stoikovich - where have we heard this name before? Could it be the same Ben Stoikovich who’s Chairman at Sovereign Metals?

The same SVML names crop up a few times - Sapan Ghai, Ian Middlemass, Mark Pearce & Dylan Browne all feature on GreenX’s website.

And as you know, management competence is the Number 1 most important feature in any investment case. I suspect that when RIO buys Kasiya from these chaps at some point in the next 12 months, all focus will switch to GreenX.

On the SVML share price - it’s on sale. Enjoy.

So you know where to put the profits should you want to double down.

You’ve got a funded company, with stunning assets, due to be awarded over £250 million - backed by the best lawyers and management team in the business - for a snip over £100 million.

It’s not hard to see where this is going (though yes, of course with all legal cases there is a risk it goes wrong).

One reason not to invest

If you’re an idiot and don’t like making money, then stay away.

You could also mention the fact that EVEN IF one Court annuls it, the other might keep it

And that does not account for the fact that on of arbitrators who wrote the unanomous award, has a status of King Council – and that pretty much gives a clarity of his standards and level of award.

Any idea what’s behind the pullback?