Fulcrum Metals

Turning Canada’s toxic legacy into gold. Literally.

Good Morning Team.

With copper, gold and silver all staying stubbornly elevated, tailings piles all over the world are becoming ever more economic.

Jubilee in Zambia has the Large Waste Rock project.

Halo is coming to the market this month.

And in the case of this particular company, their tailings were already economic at IPO three years ago when gold was still a pet rock.

Let’s consider the story.

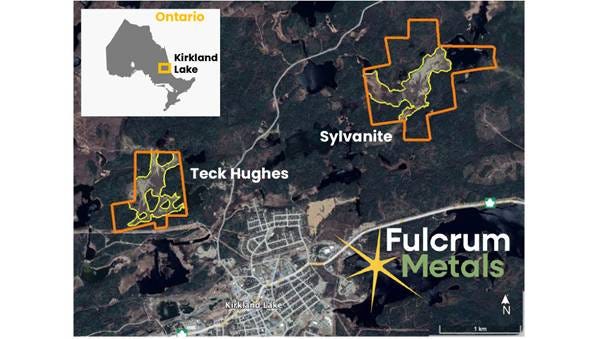

There is a town in northern Ontario called Kirkland Lake, that sits atop of one of the best gold deposits ever discovered.

Between 1917 and the late 1960s, mines in its immediate vicinity pulled roughly 24 million ounces of gold from the ground along a stretch of land locals called the Mile of Gold.

For context, that is worth somewhere north of $120 billion at today’s prices.

When the mines were done, they left something behind.

Tens of millions of tonnes of crushed, processed rock — the waste material left over after the gold had been extracted — pumped into nearby lakes or piled into enormous heaps across the landscape.

At Kirkland Lake’s Teck-Hughes site, tailings were pumped two kilometres north into Lost Lake until it hit capacity, then held back by wooden dams.

This waste has been sitting there, slowly leaching into the surrounding environment, for the better part of a century. The Canadian government has no real plan for dealing with it.

And the thing to understand about those tailings is that the gold extraction technology of the early twentieth century was not very good.

A very meaningful percentage of the gold went straight into the waste pile.

This is where Fulcrum comes in.

Fulcrum’s investment case

Fulcrum Metals is an AIM-listed company, currently trading around 10p per share, with a market cap that puts it firmly in the micro-cap bracket.

It describes itself as a ‘technology-led company focused on the recovery of precious and critical metals from mine tailings in Canada.’

The company has two flagship assets, both located in Kirkland Lake, Ontario: the Teck-Hughes Gold Tailings Project and the Sylvanite Gold Tailings Project, situated just 3km apart.

It also retains a significant equity stake and a royalty in the Tully Gold Project in the Timmins district, which it sold to Loyalist Exploration in late 2025 (along with interests in various side projects).

The basic proposition is this: those enormous piles of century-old mining waste contain extractable gold, silver and (as it turns out) a range of critical minerals including gallium and tellurium.

Fulcrum has the rights to those piles, the technology to extract the metals without using cyanide, and an exclusive licence to deploy that technology across two of Canada’s most historically productive gold regions.

The tailings are already at surface, already crushed to fine particles and already sitting on land with established infrastructure.

There is no drilling through rock, and no blasting.

Indeed, there is no conventional mining at all.

The assets

Teck-Hughes is the flagship.

The historic mine milled approximately 9.6 million tonnes of ore between 1917 and 1968, producing around 3.7 million ounces of gold — a decent mine by any measure.

When it closed, the waste was pumped into Lost Lake, held back by wooden dams, and then largely forgotten.

Historical sampling and auger drilling campaigns conducted in 1980 and again between 2018 and 2022 produced a non-compliant resource estimate of roughly 6.5 million tonnes of material grading 0.66g/t gold for approximately 138,460 ounces of contained gold.

Fulcrum’s current drilling programme is working to verify and formalise this into a 43-101 compliant figure.

Crucially, Fulcrum now owns Teck-Hughes outright. In November 2025 it completed all option payments totalling CAD$275,000 — a remarkably low acquisition cost that works out to less than US$3.30 per ounce of contained gold in the ground, compared to the industry average of around $82 per ounce for a drilled resource.

The optionors retain a 3% NSR royalty, of which Fulcrum can buy back half at any time for CAD$500,000.

The reason the acquisition was so cheap is that, until Extrakt’s technology came along, the gold was considered largely unrecoverable.

Sylvanite was the fourth-largest producing mine in the Kirkland Lake gold camp. Between 1927 and 1961 it milled 4.58 million tonnes of ore and produced 1.67 million ounces of gold.

Historical estimates suggest approximately 67,000 ounces of contained gold remain in the tailings at around 0.47g/t.

That number already looks conservative: Fulcrum’s recent surface sampling programme across 26 new sites returned an average grade of 0.66g/t gold — materially above the historic estimate — with the highest single sample reaching 2.25g/t, the highest on record at the site.

Sampling consistently ends in mineralisation, meaning the grades hold to depth.

More interestingly, Fulcrum’s expanded multi-element assaying at Sylvanite has identified gallium averaging 17.1g/t, tellurium averaging 11.72g/t, silver at 0.71g/t, and notable concentrations of rubidium (115g/t average), strontium (637g/t average) and zirconium (144.5g/t average) — none of which had ever been tested for at the site previously.

The full critical minerals picture at Sylvanite is still being assembled, with a systematic auger drill programme being designed off the back of the scout hole results.

The two sites sit just 3km apart, which is the foundation of Fulcrum’s plan to develop them as a regional processing hub — sharing infrastructure, processing capacity and operational overhead rather than treating each as a standalone project.

Together, Teck-Hughes and Sylvanite have a combined estimated in-situ metal value of over $700 million in gold, silver, gallium and tellurium based on current commodity prices.

At current prices, (let’s say gold at $4,900/oz at sale), the recoverable value from Teck-Hughes alone is estimated at over $550 million.

These are conceptual figures rather than compliant resource estimates, and they will need to be validated — but they give a sense of the scale of what is sitting there.

Extrakt’s technology

This is the part that separates Fulcrum from every other junior explorer sitting on a patch of Canadian geology.

Conventional gold extraction from tailings typically uses cyanide leaching.

Cyanide is effective, but it is also slow (leach times measure in days), environmentally problematic, produces toxic effluents, and is increasingly unwelcome from a regulatory and social licence perspective.

For legacy tailings sites in communities that have already lived with decades of environmental damage, turning up with cyanide is not a great look.

In fact, they will tell you to fuck off. Loudly.

It’s also expensive to manage and dispose of safely.

Fulcrum has an exclusive licence — covering the Kirkland Lake and Timmins regions of Ontario — for a proprietary cyanide-free technology developed by a company called Extrakt Process Solutions.

The technology is branded TNS, and it is covered by approximately 40 patents across multiple applications. At a high level, it combines a novel leaching chemistry with a solid-liquid separation process to do three things in a single closed-loop system:

extract precious and critical metals from the tailings material

dewater the processed solids

and then recover water and reagents for reuse

The practical implications are significant.

The leach chemistry works on refractory ore — material that resists standard processing — which is exactly what most historic mine tailings are. It doesn’t produce toxic effluents.

The dewatered tailings it leaves behind are described as dry-stacked, inert and non-acid generating, meaning they can eventually be returned to the environment safely. And because the system is closed-loop, water consumption and waste generation are both minimal.

The headline results from testing at Teck-Hughes to date:

Gold recovery of up to 78% — a 31% improvement over initial Phase 1 testing

Silver recovery of up to 95%

Tellurium recovery of up to 96%

Copper recovery of up to 85%

Gallium recovery of up to 20% (with further optimisation work ongoing)

Optimised leach time of just 6 hours

Dewatering in under one minute, producing approximately 80% dry-stack material

80% of water and reagents recovered for reuse

These are Phase 3 laboratory results, announced in February 2026 after a structured programme of testing that has been running since early 2024.

The broader implication is that what comes out of the process is saleable metal concentrate; what goes back into the ground is dry, inert, non-toxic material that can eventually be revegetated.

The environmental profile is, in the context of Canadian mining history, exceptional.

Why Extrakt and Bechtel matter

There is a reasonable question about whether revolutionary new metallurgical technologies actually work as advertised.

The mining industry produces a steady stream of claims about breakthrough processes that rarely materialise at commercial scale.

Two things should give investors more confidence than usual here.

The first is Bechtel. In February 2024, Bechtel Energy Technologies & Solutions — a division of one of the world’s largest and most prestigious engineering firms, with 25,000 projects completed in 160 countries since 1898 — announced a strategic global alliance with Extrakt specifically for the TNS technology.

Bechtel does not attach its name to technology that does not work. It’s also now directly involved in Fulcrum’s pilot plant scoping study, announced in February 2026.

The second is Silver One Resources, which has been testing the TNS technology at its Candelaria silver mine in Nevada. Silver One reported that the technology could potentially double silver recoveries compared to previous cyanide leaching, with leach times a fraction of those previously required.

These are not theoretical endorsements.

Exclusivity agreement

In May 2025, Fulcrum signed a Master Licence Agreement with Extrakt granting it exclusive rights to use the TNS technology on legacy gold mine waste in the Kirkland Lake and Timmins regions of Ontario — two regions covering over 3,700 square kilometres with more than 110 million ounces of historical production and over 70 documented mine waste sites.

The exclusivity runs for an initial four-year term, extendable by mutual agreement to a total of twelve years. Individual site licensing agreements will sit underneath the MLA on a site-by-site basis.

This is the strategic moat.

If the technology works at Teck-Hughes — and the evidence is increasingly strong that it does — Fulcrum is the only company that can deploy it across this territory.

Every tailings operator, every legacy site owner, every government body trying to deal with decades of environmental liability in these regions has one option for cyanide-free extraction at commercial scale.

What the drilling is showing

Alongside the metallurgical testing, Fulcrum has been running a systematic auger drilling programme at Teck-Hughes to build the data needed for a formal Mineral Resource Estimate.

Auger drilling is a cheap, low impact method suited to surface tailings — the company has acquired its own equipment including a Cobra Drill, rods and samplers, keeping costs in-house.

A total of 159 holes have now been drilled across a grid of 50m x 50m and 25m x 25m spacings, covering the entire property from surface to the full depth of the tailings. Holes reached depths of up to 12.4 metres.

All samples are being processed through photon assay for gold — a newer technique that Fulcrum has noted is particularly effective with coarse gold deposits — with comparative fire assays for validation and full ICP-MS multi-element analysis for silver, gallium, tellurium and other metals.

The headline numbers from the first 94 holes with complete multi-element assays:

Average gold-equivalent grade of 0.701g/t AuEq, incorporating gold, silver, gallium and tellurium

Best single intersection of 1.68g/t AuEq over 0.8 metres

Best hole average of 1.08g/t AuEq over 4.75 metres from surface

33% of holes returning in excess of 0.7g/t gold alone

Higher-grade zone identified in the southwest area of the tailings

Consistent gallium averaging around 16-17g/t across all holes, present in every hole drilled

Consistent tellurium averaging around 13-14g/t across all holes

It’s worth noting that the 0.7g/t average may be slightly diluted by holes drilled specifically to test the boundary contact of the tailings — in other words, holes designed to find where the tailings end rather than to sample the heart of the resource.

The grade distribution across the core of the deposit is likely to look somewhat better once the full 159-hole dataset is assembled and the MRE is prepared.

The remaining 65 holes are currently at Actlab for multi-element analysis. Once all results are in, the data feeds into a 43-101 compliant Mineral Resource Estimate, which then feeds into a Phase 4 Preliminary Feasibility Study level economic assessment with Extrakt.

For context on why the critical minerals matter: gallium is trading at around $246/kg and China accounts for approximately 98% of global production. Tellurium is at approximately $102/kg, with China producing 76% of global supply.

Canada has no domestic gallium production and minimal tellurium output. Both are on Canada’s official critical minerals list. The geopolitical context — the West’s urgent need to diversify critical mineral supply chains away from China — is directly relevant to how these assets will be valued and financed.

The non-optimised economics, and why they may improve

In March 2025, Fulcrum published a Phase 2 conceptual study at Teck-Hughes. This was explicitly described as non-optimised — a first-pass look at project viability using early test work, accurate to plus or minus 50%. The base case:

Processing 2,000 tonnes per day of tailings over a 9-year operational life

59.4% gold recovery (the Phase 1 result, now superseded)

6-hour leach time

Gold price of US$2,899/oz (gold is now above US$4,900/oz)

Single-product economics — gold only, no co-products

Pre-tax NPV7.5 of $33 million, IRR of 21.4%, payback period of approximately 3 years

Even at those deliberately conservative assumptions, the project worked. The sensitivity analysis in the same study showed that a 25% increase in either recovery rates or gold price would push the NPV to $75.5 million with an IRR of 37.7% and a payback period of under two years.

Since that study was published, essentially every material variable has moved in Fulcrum’s favour.

Gold has risen by roughly 70% and is now well above the study price. Recovery rates have improved from 59.4% to 78% in Phase 3 optimisation. The asset now has multiple confirmed co-products — silver at up to 95% recovery, tellurium at 96%, copper at 85%, gallium at 20% with further work ongoing — none of which featured in the Phase 2 economics at all.

The Extrakt Reagent Management System test work suggests the potential to reduce process solution volume by around 80% while increasing precious metal concentrations by 85-90%, which improves both operating costs and downstream recovery efficiency.

The Phase 4 PFS, when it arrives, will need to incorporate all of this. The starting point of $33 million NPV is best understood as a floor established under deliberately cautious conditions, not a ceiling.

It’s also worth considering the acquisition economics. Fulcrum paid the equivalent of less than $3.30 per ounce of contained gold to acquire Teck-Hughes — against an industry standard of roughly $82 per ounce for a drilled, compliant resource. Even if the formal MRE comes in below the historic estimate, the entry cost remains very low.

What is happening right now?

Several workstreams are running in parallel:

Pilot Plant Scoping Study — Commissioned with TDI and supported by Extrakt and Bechtel, this 10 week study will analyse the technical, logistical and execution requirements for scaling from laboratory to pilot-scale operations.

Key questions include pilot plant configuration and scale options, alternative pilot locations and logistics, vendor and contracting strategies, and an order-of-magnitude CAPEX and OPEX estimate.

In early March, the CEO, Chairman, director (and legend) Aidan O’Hara with consultant Andrew Kane attended PDAC in Toronto for arranged meetings on the tailings strategy - before the CEO and Kane visited Timmins alongside William Florman (President of Extrakt) and John Gunn (Manager of Emerging Technologies at Bechtel Energy) to assess potential pilot plant locations.

Pilot-scale demonstration is arguably the most important de-risking milestone in the entire project lifecycle, and the market will watch this closely.

Remaining auger hole assays — Full results for all 159 holes, including the multi-element suite for the final 65, are expected in the coming weeks. These feed directly into the MRE preparation.

Sylvanite development — Scout holes and surface sampling are underway across previously unsampled areas, following encouraging results from the recent 26-site programme.

A systematic auger drill programme — mirroring what has been done at Teck-Hughes — is being designed. The potential to develop Sylvanite’s 67,000+ oz tailings resource as part of a regional processing hub alongside Teck-Hughes is central to the longer-term economies of scale story.

Permitting — WSP Canada, a leading engineering and professional services firm with experience in the Kirkland Lake area specifically, has been appointed to advise on environmental and engineering permitting strategies, with an initial focus on a gap analysis for Teck-Hughes and the pathway to incorporating Sylvanite.

Government engagement meetings during the October 2025 site visits were described as producing positive alignment, with further meetings planned.

The Ontario Mineral Recovery Permit framework — which came into effect on 1 July 2025 — is providing a streamlined regulatory pathway specifically designed for operations of this type. Fulcrum is described as an early mover on this new framework.

Indigenous community relations — The company has already secured an agreement to work on the Traditional Lands of the Apitipi Anicinapek Nation, a step that consultant Andrew Kane specifically highlighted as a reflection of Fulcrum’s cyanide-free, environmentally transparent approach.

Kane’s 30-year network across Ontario government, industry and First Nation communities appears to be an underappreciated operational asset at this stage of development.

The bigger picture

There is at least $10 billion worth of gold in tailings in Ontario alone. The provincial government has no coherent plan to deal with decades of mine waste.

Local communities have legitimate and deeply-held objections to new mining developments partly because they have watched previous operators leave behind long term environmental damage.

Fulcrum’s pitch to all of these stakeholders is different in kind from any conventional miner: we will take the toxic waste that has been blighting your landscape and your water table for 60 years, extract the metal from it using a process that produces no cyanide and leaves behind only dry, inert material, and then restore the site.

We need no environmental approvals for new open-pit or underground mining. Our tech uses off the shelf materials, so there will be no surprises.

We are solving an existing problem, not creating a new one.

The business model that flows from this — an exclusive technology licence across an entire region, a pipeline of 70+ documented mine waste sites, a scalable process plant that can move from site to site, with Bechtel as engineering partner and Extrakt as technology provider — looks less like a junior miner and more like an environmental services company with attractive economics.

That matters for two reasons.

First, a different and larger class of investor is attracted to ESG-oriented technology businesses than to standard junior explorers.

Second, access to finance on better terms becomes possible when the environmental story is genuinely positive rather than managed.

Share register strength

More than half the shares are not in public hands.

The lowest price at which anyone invested in the company initially was 10.25p — there are no seed investors sitting on a 10x return waiting to sell into any positive news.

In early February 2026, it was disclosed that John Story had crossed the 10% threshold — a new significant shareholder, and one whose arrival at that level suggests conviction in the direction of travel.

CEO Ryan Mee and director Aidan O’Hara each hold significant positions.

And today, they’ve raised £550,000 through a direct subscription with a single investor - at a small premium - at 11p per share. The capital will be used

The register is, as far as can be determined, largely in patient hands — I’ve been waiting since the IPO for 2026 - which is the year the story kicks into gear.

The bottom line

Fulcrum Metals is not a conventional gold miner, and it is a mistake to evaluate it as one.

It’s a company with exclusive rights to a breakthrough processing technology, applied to a large and largely untapped resource base in one of the world’s great historical gold regions, with a business model that aligns commercial interest with environmental remediation.

The Phase 3 results — 78% gold recovery, 95% silver, 96% tellurium, 85% copper — represent technical validation of the core proposition.

Bechtel’s involvement as an alliance partner and co-author of the pilot plant scoping study is an external endorsement that deserves to be taken seriously.

The path from here to production involves the pilot plant, the MRE, the PFS, and the permitting process. Each of these is a meaningful step with its own timeline.

But the direction of travel has been consistent, and each milestone over the past two years has validated rather than undermined the thesis.

You don’t want to throw the kitchen sink at this. But you might want to consider a Fulcrum fee.

Tailings stories are set for a run.

i hope you are doing better with fulcrum then me as jubilee shareholder (lost more then 50% already.)

recovery is indeed needed