ARC Minerals: the beginnings of a Tier 1 deposit

with $21 million about to go into the ground

Good Morning Team.

After yesterday’s RNS, it turns out that if you pray to Kothar (the Ugaritic god of copper), he may sometimes listen to your prayers and reward you with an embarrassment of riches.

Before we get cracking, listen to Arc’s management talk through yesterday’s RNS (if you haven’t already). This is required listening, so please don’t skip.

I also have a wealth of material on #ARCM for first time readers.

Most can be found through the posting history on this Substack - and probably amounts to a medium-sized book of copy. For first timers, consider the wider investing case on MININGAIM and work your way through the Substack updates thereafter.

Then come back here and get in a good mood.

Taken from my Investor Call in Q4 last year:

Let’s dive in.

Tier 1 Potential

At the start of every ARCM RNS, Arc Minerals calls itself ‘an exploration company forging partnerships to discover and develop Tier 1 copper deposits.’

Apart from the the nature of the fantastic Joint Venture with FTSE 100 major Anglo American, this phrasing has perhaps been a little optimistic. But yesterday’s results from initial Anglo drilling in Zambia now warrants the epithet - and with one RNS, Arc is starting to build evidence of a Tier 1.

Before we get too technical, it’s worth noting that Arc was trading at around 4p in November 2023, and by every fundamental metric is more advanced than back then.

It raised over £4 million last year (at a premium to today’s share price), and has also benefitted from the Anglo cash instalment. This leaves the company fully funded until late 2026, at which point an $8 million JV cash instalment lands in the bank account.

Yesterday’s RNS is exactly what anyone clued in wanted to see.

Diamond Drill Hole KCDD002 - 40.60m @ 0.61% Cu from 22.25m

Including 7.70m @ 1.72% Cu from 26.75m, or 12.75m @ 1.20% Cu from 22.25m

I’m going to give you guys some perspective here: our closest neighbour and constant comparator, Sentinel, is a sulphide-hosted deposit hosting an average grade at present of 0.48%.

You might want to look at some of the assays reported by Kiwara, which owned the Kalumbila project. The company was bought out months after this RNS in 2009 by FQM, and its assets became the cornerstone of Sentinel.

Good work back then, Colin.

Kansanshi and Sentinel - owned by FQM - are now worth circa $10 billion (that’s billion with a B) according to reports that Mitsui plans to take a 20% stake. So the potential is very much there.

I noted publicly before the results that I would be excited by anything above 0.48% and with a length of around 20 metres - so we are bang on the money. In fact, we’re very clearly in the right region of grade and length.

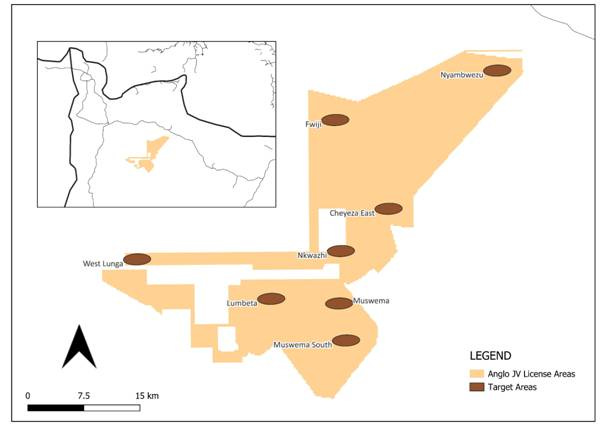

This new discovery is just 1.5 kilometres from the original Cheyeza East Oxide Occurrence. Six holes have now been completed in Zambia covering 4,016 metres at four targets - with the deepest hole going almost an entire kilometre into the earth.

Executive Chairman Nick von Schirnding enthuses:

‘I am delighted to report that the first assay results of the Anglo JV confirm additional near-surface copper mineralisation at the Cheyeza target. The newly drilled mineralisation is similar to historic assays in terms of both grade and thickness and is over 1.5 km away from Cheyeza. Work is now underway to identify further potential drilling targets at Cheyeza to test the extents of sulphide mineralisation.’

There’s three holes left to be reported back on (two at the new priority target south-east of Muswema). And let’s remember - this is just the beginning. If we assume that the JV spent circa $3 million in 2024 (you don’t skip the surface exploration - image below - when you explore as a major), then we have around $21 million that needs to be sunk into the ground over less than two years.

That means multiple rigs, many assays, and plenty of news flow to look forward to - without funding concerns.

Sulphide vs Oxide considerations

I think it’s well worth spending a moment explaining why sulphides have excited the team so much. I want to be clear here that higher grade oxides (for example, the excellent grades found at Midnight Sun’s Kazhiba Target within the Solwezi Project) are valuable ores.

They can be developed as stand-alone mines, or be incorporated into larger operations if close to a major mine.

But oxides are - as a general rule - not Tier 1 material.

And Arc is looking for Tier 1’s.

Oxide deposits are typically processed using heap leaching and SX-EW (solvent extraction-electrowinning), which requires sulphuric acid (not environmentally friendly) but more importantly, large amounts of water. This process can be expensive - and given the drought of recent years in Zambia, even getting sufficient water can be a challenge.

Sulphide deposits tend to be processed via floatation and smelting - this is up-front capex heavy but much more cost-effective over the long run if you have a sufficiently large deposit when economies of scale take over.

This is important because sulphides - while they tend to be much lower grade - are almost always larger and deeper than oxide deposits, which tend to be shallow and deplete quickly.

Again - oxide deposits have advantages - especially if a junior is developing them itself. If Arc ends up with a reasonable Tier 2 oxide resource, this would not be a poor outcome by any means. But it’s just not what a major wants as the main course.

The other key factor to consider is that sulphide ores generally have much higher copper recovery rates, which compensates for lower grades. Meanwhile, oxides not only have lower recovery rates, they’re also more variable which can make mine planning harder. Copper concentrate from sulphides is also more widely traded, with more stable prices.

Of course, it’s often the case that oxide ores are found in the upper layers as part of a weathered cap of a deeper sulphide system - so seeing sulphides within a near-surface oxide core should excite you.

Which is exactly what Arc has just seen.

For perspective, the new KCDD002 assay results are already adding on to the oxide occurrences at Cheyeza - where previous hole CHDDE004 intersected 18m @ 2.35% Cu from 30.60m with a higher grade zone of 7.60m @ 4.15% Cu from 39m, and hole CHDDE060 intersected 39m @ 1.47% Cu with a higher grade zone of 10m @ 2.25% Cu from 41m.

But the key point is that the previous oxide was a ‘remobilised copper oxide occurrence.’ This new hole ‘may be the result of weathering of sulphide mineralisation at source, which is supported by the presence of sulphide mineralisation below the oxide zone.’

You can extrapolate the importance of this statement from the above, but to clarify further:

The original drill result being a remobilised copper oxide occurrence essentially means that the copper oxide was not formed in place but was transported from its original source by natural geological processes (for example, groundwater movement). Essentially, copper was dissolved from its primary mineralisation, moved through rock formations, and then re-precipitated elsewhere as copper oxide.

This new result, with weathering of sulphide mineralisation at source, means the oxide mineralisation was formed in place by the weathering - i.e., the sulphides oxidised due to exposure to oxygen/water, leading to the formation of copper oxides.

Because you have the sulphide mineralisation beneath the oxide zone, you can be almost sure that this oxidation occurred at the original deposit rather than due to remobilisation.

This matters on multiples levels: remobilised oxide deposits are unpredictable and scattered because the copper has been transported from its primary source. But more importantly, in-situ weathering of sulphides suggests a Tier 1 mineral source nearby (or lying underneath the weathering, just ready for a drill bit).

Okay does that all make sense?

It does to me - it’s hard to strike a balance between technical detail and accessibility.

It’s also worth noting that assay results have also been received for the two holes drilled at the new target Nkwazhi - low grade sulphide mineralisation was confirmed in the first hole.

If you look at the map, it doesn’t take a genius to guess where Anglo will stick the drill bit next.

Large Scale Mining License Granted

If the geology isn’t enough for you, then consider the corporate updates - both from mid-January.

First up.

Handa (the Anglo JV company) has had the Large Scale Mining License 33404-HQ-LML approved. This is big, big news and hugely underappreciated by an apathetic market.

Further, Arc noted that ‘the other two Large Scale Mining License Applications 33402-HQ-LML and 33403-HQ-LML now reflects as reinstated on the Zambian Mining Cadastre Portal.’

There are essentially two key concepts to ‘get’ when it comes to obtaining this LML.

First, once the other two LMLs are granted, we have the tenure for the next 25 years. And Anglo may, finally, be able to sing about why they find these particular licenses worth returning to Zambia for.

Given that the company has struck several decent results on near its first try (again, we still have the new target assays to come back), it’s hard not to think they know more than what they are letting on.

As a reminder, obtaining a LML requires geological reports and feasibility studies. This is no great secret, and is outlined as a requirement by the Ministry of Mines and Mineral Development.

The specifics have not been published, but the bottom line is that either this documentation has been provided OR Zambia sees a specific political, financial or strategic interest in making an exception - because otherwise, the LML would not have been granted.

As we know, Duncan Wanblad has made clear that he is bringing Anglo American back to Zambia in a larger fashion. I have speculated on what the game plan is before, but the key point for ARCM is that there are available licenses adjacent to the current JV that, should Anglo take them up, would be folded into the JV and require additional spend.

Injunction Secured

ARCM recently noted that the High Court in Zambia has granted an ex parte interim injunction in favour of Arc against interference at any existing or future licences in Zambia.

The injunction has put Mumena Mushinge firmly back inside his playpen - and most interestingly (among many other conditions), prevents him from:

‘Interfering with any future licences over any existing ground that is under licence or under application, or any future ground over which licences may be obtained by any means whatsoever.’

I love clues.

We can talk potential damages - personally, I’d vote for a special dividend so we can all have a drink on Mushy - but this was a settled legal case and the man has now bitten off more than he can chew.

Zambia wants Anglo back, and Anglo wants an easy life. If you listen to Wanblad’s comments at Indaba, you might have noticed him talk about African nations needing to commit to fair deals with external companies.

You know who else is at Indaba?

A personal message sent from the three to me:

'The sun is shining at Indaba. We're seeing keen interest in our fantastic Joint Venture with partners and friends Anglo American, as we look to step up exploration in the wake of this season's sulphide discovery. Stay tuned.'

More clues.

But to be honest, all the majors are returning to the country.

It’s going to be fun.

Zeus view

Zeus remains of the view that the licenses are in expert hands, and being funded with capital few others have access to.

The broker foresees either a major discovery that Anglo will salivate over (the EuroMillions jackpot), a mid-tier discovery that’s still pretty good but not good enough for a major (the National Lottery jackpot), or nothing.

Sorry, but I’m not sure that’s as informative as it sounds given that these are the only possible options. If I flip a coin, it will either land on heads, tails, or its side.

But the key quote is this:

‘We see fair value at 5.8p per share, though recognise significant upside if a consistent set of drill holes leading to a discovery is made.’

Translation: it’s early days but even so, Arc is horrendously undervalued. I personally remain of the view that these are some of the best copper exploration licenses on the planet, and a large rise is going to happen.

License exceptionalism

As a reminder, ARCM’s Zambian licenses cover some 870 square kilometres located inside the North Western Province, within the Domes region of the Zambian Copperbelt, near world-class producing mines including First Quantum Minerals’ Sentinel and Kansanshi mines and Barrick’s Lumwana mine.

These licences are some of the last Domes areas to be explored in detail and are within the trending arm of the major geological structure known as the Lufilian Arc (Copperbelt), on the western flank of the Kabompo Dome. The Copperbelt is home to all the major copper mines in Zambia, which accounts for more than 80% of Zambian copper production.

The assets were previously explored through an Equinox Minerals and Anglo American Joint Venture during the late 1990s as part of the Kabompo Project.

ARCM’s areas under license encompass nine of 30 exploration ranked targets, including the top seven ranked targets.

FQM’s Sentinel copper mine — which produces over 250,000 tonnes of copper per year — was originally ranked number 22 of the original 30 targets. At the time, it had an exploration target size of six million tonnes of ore, but this was eventually upgraded to a gigantic one billion tonnes.

And we are getting results that mirror Sentinel’s early exploration.

I won’t say what year we’re going to rocket.

But the time is coming.

Assays from the new priority target to come

To remind you of the next course, consider the new target currently in the kitchen:

Located 4 km southeast of Muswema, targeting a second order soil geochemical anomaly.

Initial drilling encountered lithologies and alteration similar to known deposits in the Copperbelt's Domes Region.

Observed copper mineralisation with multiple generations of chalcopyrite in the drill core.

This target is prioritised for follow-up drilling due to encouraging initial findings.

Anglo is the one calling the shots, so must have seen something in a ‘second order’ soil geochemical anomaly that was not there in the primaries - and this target was clearly the reason why senior personnel were called out to inspect the ground.

We are seeing multiple generations of chalcopyrite, meaning copper mineralisation was formed in different stages during the formation of the rock. This means an ongoing, rich, mineralising process - exactly what happened at Enterprise and Sentinel.

For context, the presence of multiple generations of chalcopyrite aligns with these major Domes Region mines’ geological history of tectonic activity and hydrothermal processes, that have contributed to the formation of their significant mineral resources.

And as we do not have assays yet, then clearly this information must be visible.

For perspective, early generation chalcopyrite would form during the initial cooling of hydrothermal fluids rich in copper and sulphur, associated with the early stages of volcanic activity or the movement of magma. Subsequent generations would form due to changes in pressure or temperature, or the introduction of new fluids that modify the chemistry of the mineralising environment.

The early generations would likely host larger crystals while later generations could show finer-grained textures (due to faster cooling or changes in fluid chemistry). Later generations might also be coloured differently as they would contain inclusions of other minerals, or show other signs of alteration.

You need multiple generations to get the grade you need, as it implies that the deposit has been active over a significant geological time, allowing for a substantial accumulation of extensive, complex and more easily recoverable copper.

In Q4, Arc made clear this target was being prioritised for follow-up drilling (note that they made it just into the New Year before being forced to stop by the rains).

We now have sulphides elsewhere - so the geological incentive is there to drill at two locations at least.

The bottom line

ARCM has:

A JV with Anglo American worth up to $88.5 million covering some of the most prospective copper licences on Earth.

Further drilling at this JV set to commence when the much-needed rains cease perhaps as soon as April.

Financing to last for years without needing to go to the market.

A management team chaired by a former senior executive at Anglo American.

Years of exploration not priced into the market cap.

Operations across Zambia which is becoming an ever more favourable jurisdiction.

A share price on the floor that does not reflect the upside potential.

Sulphides with assay grades and lengths comparable to early-stage exploration at Sentinel.

Visible cores that have Anglo geologist David Wood ‘really impressed by what he was seeing.’

Assays from this new ‘priority target’ that has Wood so excited to land soon.

Circa $21 million of cash going into the ground over the next couple of years, requiring multiple rigs and massive assay news flow.

Every major worth a damn heading back to Zambia with ARCM owning objectively the best exploration licenses in the country.

Legal issues being resolved for good.

And Botswana, but that’s a story for another day.

Yes, it’s been (for lack of a better phrase) a choppy journey. But magic happens. When Greatland Gold found Havieron, the stock rose by 71x. I regularly interview CEO Shaun Day, who now - yes after acquisition and dilution, but still - runs a billion pound company.

The AIM market needs something to wake it up.

Let’s give it a Double Espresso.

Or perhaps an Irish Coffee.

Excellent writeups!