Apertura Energy

Rebuilding Venezuela.

")

Good Morning Team.

A little over a month ago, I covered the Moonshot investment case for Apertura Energy. My subtitle was ‘The Opening Act’ - a double entendre which implies both the company's launch and the re-emergence of Venezuela’s oil and gas industry.

Back then, the wine had only just been selected. The Sommelier has now uncorked the bottle, and we are now going through the theatrical production that is ‘tasting’ the wine.

And the thing is with wine, there are only really three levels of quality.

Plonk (house wine), the second-cheapest (the one we all order to not appear cheap), and expensive.

Expensive wine is either indistinguishable from the second-cheapest, or close to a religious experience.

And I’m liking the vino Apertura is serving.

Let’s dive in.

The size of the prize

For those of you new to the story, I suggest you go back and read my original thesis as this will help you understand the risk-reward profile.

(TL;DR we’re at the extreme end of both)

For those of you who can’t quite bring themselves to do this, a summary:

Venezuela sits on the world’s largest proven oil reserves - roughly 303 billion barrels, more than Saudi Arabia - concentrated in the Orinoco Belt.

A toxic cocktail comprising decades of nationalisation under Chávez and Maduro combined with sanctions and the exodus of skilled workers, collapsed production from a 1990s peak of 3.5 million barrels/day to under 500,000 by 2020.

That changed in January 2026 when US special forces captured Maduro, who now faces narco-terrorism charges in New York. Interim president Delcy Rodríguez has since rolled back state controls and reopened the sector to foreign capital, with oil revenues now flowing through US-controlled accounts, giving Washington financial leverage and effectively de-risking the environment for western firms.

For context, Venezuela’s output is now up about 20% since Maduro’s arrest - circa 200,000 barrels a day, or about half of Ecuador’s production.

500,000 barrels a day of oil, which is easy for Houston refiners to process, has started reaching the coast.

That’s not nothing.

And most of it used to go to China.

Major oil companies are re-entering, and through safer structures including production-sharing and cost-recovery-via-crude rather than the equity stakes that got them expropriated in the 2000s.

However.

The whole reopening is bottlenecked by an infrastructure gap.

And I pitch Apertura Energy as the prime vehicle to exploit that gap.

It’s built around British-Venezuelan brothers Scott and Greig Gilbert, whose family has three generations of history in Venezuelan oil.

Scott runs AIM-listed frontier E&P company Corcel, giving the company capital markets and deal-making credibility, while Greig runs Conterp, an established Brazilian oilfield services business with hundreds of staff, working rigs and active Petrobras contracts.

My thesis is that this existing operational capability (plus their supply-chain business, AOT International) can be redeployed into Venezuela faster than any other competitor could assemble from scratch, giving Apertura first-mover advantage as the sector reopens.

No deal has closed yet and this is explicitly a pre-revenue, pre-asset bet.

But US bipartisan backing makes the political reopening a long-term reality, and Apertura is positioned as the only London-listed pure-play on Venezuelan oil.

And early investors in London-listed movers into reopened frontier jurisdictions (for example, Gulf Keystone in Kurdistan) made millions.

Caracas has the oil.

London has the expertise.

Put them together?

Fireworks.

Institutional Validation

That original piece was published over the weekend on Sunday 31 May and within 24 hours had reached the retinas of people I had not imagined possible at the time.

Now when talking institutional validation, the first thing to do is talk about the shell’s share structure.

A loose shell goes nowhere, as any hermit crab can tell you.

This is a paper valuation only — but there are only 17.5 million shares currently in existence (RNS, 30 June).

And if placees are holding for gold, it’ll be like Delta Gold. Multiple investors individually believing in the investment case — having independently decided the potential means that even sitting on paper gains, it’s better to keep holding.

Is this mad?

No.

Why?

Because small caps work via the power law. Last year, my own portfolio returned 110% over the calendar year — dominated by a handful of exceptional winners.

When you take a stake in a shell, you’re investing to win.

Yes, you might also lose your money. You need to accept that risk. But if you’re going to risk money in this market, you’re better off going for the extremes because — well — why the hell not?

Other than the occasional inheritance tax advantage, that’s what small caps exist for.

And while I’d love to say that everyone staying in this story is doing so because they believe in my own asymmetric genius, I have already been eclipsed.

Days after my article, we saw three TR-1s land in short order.

Their names are easy enough to find and their respective positions mean something significant.

It means that these investors alone, who in my estimation will not sell, drive down the effective free float from 17.5 million shares to 12.5 million. Add in the Gilberts’ combined block of 3 million shares and the real free float shrinks further still.

That’s not a lot of shares to go around when the wider market picks up this story.

And given the churn since the RTO, I’d venture that the real free float is only a fraction of even this.

Any sustained buying on a fundamental change (let’s say acquiring a Venezuelan asset) and this stock goes into the fucking stratosphere.

Who are these guys?

The first name keeps cropping up elsewhere in situations like this — with fingerprints increasingly visible across small-cap venture and resource plays.

The second sits near the top of a major institutional fund, managing tens of billions in assets — a connection that, given the licences involved, may well be personal rather than purely financial.

The third is Gavin Wilson, a legend in this space. He’s served as investment manager at Meridian for over a decade, and is a NED at PetroTal, TAG Oil and Afentra.

Meridian is a Hong Kong-based international investment firm — where he manages an oil and gas portfolio focused on world-class assets in emerging markets.

That could be handy.

But he’s best known as the founder of both the Rab Energy and the Rab Octane funds, which were highly successful, stand-out performers in the hedge fund industry during Wilson’s tenure during 2004 to 2011.

While the broader parent firm, RAB Capital, struggled heavily during the 2008 financial crisis due to problems in its flagship Special Situations fund, Wilson’s energy strategies remained a distinct bright spot.

Rab Energy, launched in June 2004, saw a 70.4% gain in its first ten months and won the prestigious Eurohedge New Fund of the Year 2004. The fund consistently delivered massive gains, achieving returns of 86% in 2009 and 46% in 2010. At the end of 2010, HSBC ranked it as one of the top-performing hedge funds globally.

When RAB Octane launched in 2005 to focus on pre-IPO private equity and farm-ins, it raised $55 million immediately — the highest launch funding for any RAB strategy at the time. Initial entry was strictly restricted to existing investors of the oversubscribed RAB Energy fund.

Raising capital with a crew who knows how to hold.

With a kickass fund name.

Arguably, when Wilson decided to ‘retire’ in May 2011 (these people never actually retire), it was the key catalyst for RAB itself de-listing.

He also served as the Head of Canaccord’s Oil & Gas division in London, where he led sales, corporate broking and finance activities.

Yep.

He’s that guy.

And given this pedigree, who else may be in this stock below the TR-1 threshold?

Exactly.

Speaking of which.

Major Validation

Apertura has now appointed Chris Steele as a Non-Executive Director, effective immediately.

Chris is based in London (building on the uniquely British branding here).

But he’s also American.

And he’s a geologist.

And he’s a highly experienced energy executive who spent 43 years at Chevron (and Texaco).

In his most recent role as Director of Commercial (E&P Americas), he was in charge of $350 billion major Chevron’s Venezuela sanctions effort.

Indeed.

I know.

Let’s talk context.

Chevron is the sole major US oil company still operating in Venezuela because it has been granted a specific licence by the US Treasury, issued by the Office of Foreign Assets Control (OFAC).

It’s the King of Venezuelan oil.

And to an extent, it’s because of this man.

As a former history teacher, I invite the class to sit down.

Here’s how Chevron went from ‘shut down completely’ to ‘primary Western energy anchor in Venezuela’ in the span of 14 months.

It started with General License 41 (GL41), issued by the Biden administration and handed to Chevron as authorisation to do something almost no other Western major could - pump and export Venezuelan crude straight to the United States.

At its peak, that meant somewhere between 200,000 and 250,000 barrels a day flowing out of joint ventures with PDVSA, Venezuela’s state oil company, into Gulf Coast refineries.

For a couple of years, this was the golden window — serious production in a country most Western energy firms had written off.

Then, in February 2025, the golden goose was summarily executed.

President Trump ordered GL41 killed outright, citing the Maduro government’s failure to meet ‘electoral conditions’ tied to the disputed July 2024 election, along with frustration over its slow pace of accepting deported migrants from the US.

OFAC didn’t just flip a switch — it issued License 41A, forcing Chevron into a hard wind-down.

Exports that had been running at a quarter of a million barrels a day stopped dead.

What followed was months of limbo.

By May 2025, Chevron was operating under an extremely narrow authorisation - no pumping, no exporting, nothing commercial at all. The license existed for one purpose — keeping the physical infrastructure intact and the personnel safe.

Think of it like corporate life support.

Then the screws tightened further. Mid-2025 brought a hardening campaign, with new maritime restrictions specifically designed to cut PDVSA off from any financial proceeds or US-linked shipping networks.

This was, in all but name, an attempt to choke the entire Venezuelan oil economy at the export stage.

Then in early 2026, the Trump administration reversed course again — but not indiscriminately.

It selectively eased components of the blockade specifically to let certain multinational players negotiate limited re-engagement, to redirect Venezuelan oil away from China, rather than let Beijing absorb the barrels the US had walked away from.

Chevron restructured.

In April 2026, the company executed a landmark asset swap with PDVSA:

It doubled down on heavy crude — expanding its stake in the high-yield Petroindependencia joint venture from 34% to the legal maximum of 49%.

Grabbed new drilling rights — securing the Ayacucho 8 block in the Orinoco Oil Belt through its Petropiar venture (30% stake).

Walked away from offshore gas — fully divesting Plataforma Deltana Blocks 2 and 3, along with its stake in the western Petroindependiente venture.

Chevron traded optionality for concentration. Out of offshore gas, all-in on the heaviest, densest crude reserves in the Orinoco Belt — a bet that the future license framework would keep favoring companies willing to operate inside Venezuela’s most complex, most sanctioned terrain.

The groundwork for this pivot was laid years before anyone had heard of a 2026 asset swap.

Steele served as Chevron’s Director of Commercial Americas E&P from April 2023 to January 2024 — a role explicitly focused on leading the company’s Venezuela sanctions strategy.

He took the seat just months after GL41 was first issued, meaning his tenure covered the license’s most productive stretch - the scaling-up period when Chevron was maximising exports to Gulf Coast refineries while building out the compliance frameworks needed to keep doing so legally.

That’s the less glamorous but more important part of the story.

The frameworks and government-relations protocols built during Steele’s window are plausibly what let Chevron’s Venezuelan assets survive the 2025 hardening phase intact, rather than being seized or gutted the way some feared.

Steele’s parallel work restructuring Chevron’s Iraq exposure during that same 10-month stretch also tracks suspiciously well with what came later — a company culture already fluent in divesting non-core international assets, which is essentially the exact move Chevron made with its offshore Venezuelan gas holdings in 2026.

He moved on to a broader role as General Manager of Emerging Countries, but the compliance scaffolding from his direct tenure looks, in hindsight, like the blueprint for everything that followed.

It’s not just the sanctions title that matters here. Steele’s Chevron career also included time actually based in Venezuela, working directly with PDVSA and regional operators, plus a string of senior roles spanning Latin America, Africa and the Middle East — Head of Emerging Countries, General Manager of Strategy, Planning and Commercial for Africa and Latin America, and General Manager for Business Development across Europe, Eurasia and the Middle East.

Country-specific relationships layered on top of broad emerging-market upstream expertise.

CEO Greig Gilbert framed the timing of the hire explicitly around Venezuela’s recovery following the 24 June earthquakes, and enthused that:

‘Chris is one of a few senior energy executives internationally who combines deep Venezuela-specific experience, direct knowledge of the regulatory environment, and a career spent originating and executing complex upstream transactions at the highest level.’

Steele, for his part, noted that:

‘The reopening of Venezuela’s energy sector presents a rare opportunity, and I believe Apertura is well positioned to play a meaningful role in that process. The combination of Apertura’s strategic vision, capital markets platform and operational capability creates a compelling proposition for investors but more importantly for the Venezuelan government and people. I look forward to working with the Board as we seek to identify, develop and execute high-quality opportunities for shareholders.’

The signal is clear - the same person whose 2023–2024 mandate built the compliance scaffolding that let Chevron survive the 2025 shutdown and capitalise on the 2026 reopening is now positioning himself on the other side of the table — helping a nimbler entrant identify and execute opportunities in the specific environment he spent a decade learning to navigate.

If Chevron’s asset swap was the payoff for infrastructure built years earlier, Steele’s move to Apertura looks like the next round of that same trade — this time played through a small cap with a free float that makes the Apples of the Hesperides look commonly available.

Steele isn’t only bringing relationships and institutional memory to Apertura.

He’s bringing the one skill the entire venture is structurally dependent on — the ability to read and negotiate OFAC’s shifting intent in real time.

Apertura’s business model is, in essence, ‘help re-open Venezuela’s energy sector,’ and that’s not achievable without clearing OFAC at every stage - license applications, transaction structuring, counterparty vetting and ongoing compliance monitoring.

Steele didn’t observe that process from the outside — he ran it, through GL41’s peak, its 2025 termination, and the wind-down that followed.

But what assets are we going after?

Yes, this is the billion-dollar question.

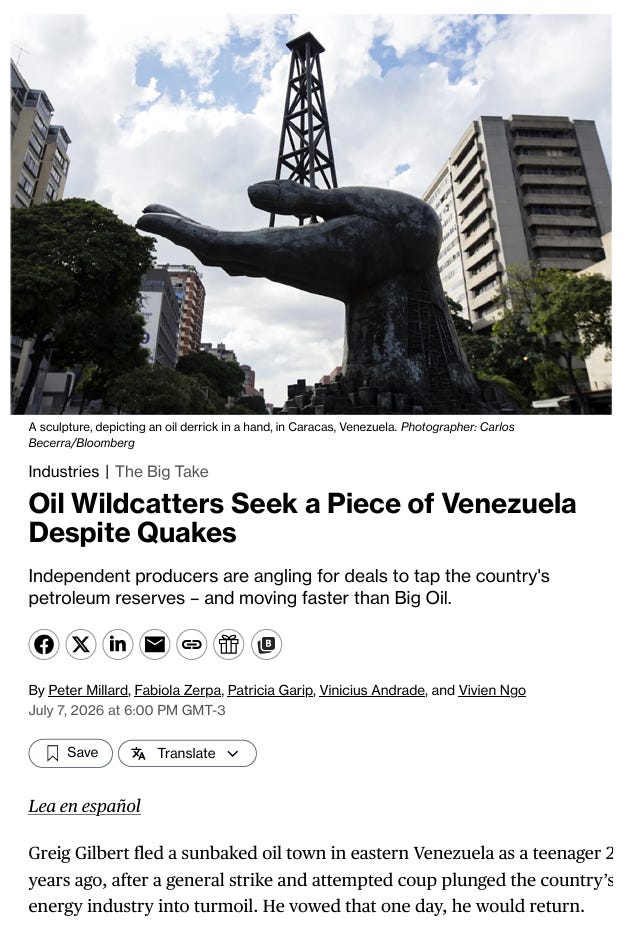

First, consider that on 7 July, Bloomberg - which perhaps holds more reputational capital than a chap with a Substack - published this as a lead piece:

That says ‘20 years ago’ by the way.

Anyway, other than being a genuinely excellent human interest piece, it notes that:

‘The unfolding devastation (earthquakes) has convinced Gilbert that his homeland needs people like him to help rebuild. Gilbert is among a group of scrappy, independent prospectors leading the charge back into Venezuela, seeking to jump-start an oil industry that has deteriorated over decades. The band of fortune hunters is willing to gamble in ways larger companies are not, with the hope that early investments will make for big paydays.’

And despite the disaster, none of the wildcatters consulted by Bloomberg are planning to pull out.

Greig says that ‘the country is hungry to reactivate and it needs all the aid and revenue it can get to rebuild.’

Bloomberg’s article also noted that Trump met with the wildcatters alongside major oil executives in the aftermath of Maduro’s capture, reporting that he ‘clearly enjoyed their enthusiasm more than representatives from major firms’ and even smiled at reps from Armstrong Oil & Gas and Aspect Holdings, calling their profession ‘pretty cool’ and enthusing:

‘I’ll tell you — I would have been a wildcatter too.’

Naturally, some are trying to buy Trump’s favour.

Of course, no US President would stoop to such a level, but the Batista brothers whose J&F SA is a multi-billion-barrel Venezuelan oil project made the largest single donation to Trump’s 2025 inaugural committee.

Coinbase donated $300 million to Trump’s White House ballroom project, and its co-founder Fred Ehrsam has made several trips to Caracas and met with senior Venezuelan and US officials, including Rodríguez and US Interior Secretary Doug Burgum.

Ultimately, a US partner may be a prerequisite to getting a deal.

Perhaps this is something for Apertura to consider.

But let’s take a couple of steps back.

For years Venezuela represented one of the greatest paradoxes in global energy. Investors never doubted the quality of the resource, but they doubted whether Venezuela itself could ever become investable again.

2026 has dramatically altered that calculation.

The change in government, accompanied by a broad easing of US sanctions and a complete reorientation of Washington’s Venezuela policy, has reopened one of the world’s largest untapped energy opportunities.

Instead of focusing solely on humanitarian relief or political normalisation, the new approach has placed reconstruction of the oil industry at the centre of Venezuela’s economic recovery. The underlying assumption is straightforward - no other sector is capable of generating the foreign currency required to rebuild the country on the scale that hydrocarbons can.

And what’s escaped many is that the first organisations to move aggressively were not the international oil majors but the global commodity traders.

That should not be surprising.

Vitol and Trafigura specialise in environments where politics and commerce overlap. They are accustomed to operating in difficult jurisdictions, arranging financing, managing shipping logistics and finding buyers for crude that traditional markets may struggle to absorb.

Their willingness to commit capital often serves as an early indicator that broader commercial confidence is returning.

The recent expansion of the oil marketing agreements between PDVSA, Vitol and Trafigura therefore represents far more than a trading arrangement.

What reportedly began as agreements covering around 50 million barrels has grown into contracts exceeding 100 million barrels.

Those volumes effectively place the traders at the centre of Venezuela’s export strategy, giving them responsibility for marketing a substantial share of the country’s production while reconnecting Venezuelan crude with refiners across North America, Europe and Asia.

Perhaps the clearest indication that these firms expect the relationship to become permanent is their physical presence inside the country.

Vitol’s preparations to establish an office in Caracas is strategically significant.

Yes, a dozen employees may seem inconsequential compared with the company’s global workforce, but opening a permanent office represents a commitment to participate directly in the rebuilding of Venezuela’s petroleum sector rather than simply purchasing cargoes from abroad.

Trafigura has already taken that step, establishing its own office while continuing to co-ordinate regional trading activities from Montevideo.

This transformation has also fundamentally altered the geography of Venezuelan oil exports. During the sanctions era, China became the dominant destination for Venezuelan crude, often through complex intermediary arrangements designed to navigate international restrictions.

Today, those trade flows are being redirected. The United States has re-emerged as Venezuela’s largest customer, India has rapidly increased purchases, and European refiners have returned to the market. We’re seeing, in real time, the reintegration of Venezuelan crude into mainstream global energy markets.

India’s renewed interest is particularly interesting because it reflects broader changes in global energy security rather than attractive pricing.

As one of the world’s fastest-growing economies and its third-largest importer of crude oil, India has always sought to diversify supply. The disruption of energy flows through the Strait of Hormuz has reinforced that strategy.

Approximately half of India’s imported crude normally transits that narrow waterway, making any prolonged instability in the Gulf an immediate concern for policymakers in New Delhi.

Venezuelan crude provides an alternative source of supply. It’s that simple. And the US like sit too, because it reduces Indian reliance on Russian imports.

And although Venezuelan production remains well below historical peaks, the country’s exports have risen steadily as sanctions eased and commercial relationships were restored.

Production is again exceeding one million barrels per day, placing Venezuela among the more significant suppliers within OPEC, even if it remains far below the three million barrels per day the country produced at the height of its oil boom.

This brings us back to Apertura.

Because while it’s getting better, the operational constraints are becoming considerably more visible.

Perhaps none is more serious than electricity, because oil production in Venezuela is increasingly depending on electrically powered pumps and artificial lift systems that require stable, uninterrupted power.

The problem is that the national electricity grid has deteriorated to such an extent that routine blackouts and voltage fluctuations regularly interrupt production. Wells automatically shut down when frequency variations threaten to damage equipment, forcing operators to restart production manually.

Every major power outage translates directly into lost oil output.

Lost output = less money.

Rather than attempting to solve this problem by first rebuilding the national grid, the government has adopted new hydrocarbon regulations which require companies to become largely self-sufficient in electricity generation.

Investors are expected to construct dedicated power plants, install gas-fired generation facilities or deploy large-scale generators capable of supplying their own operations independently of the national grid.

This policy represents an implicit acknowledgement that Venezuela’s broader infrastructure crisis cannot be resolved quickly enough to support the pace of investment policymakers hope to attract.

Instead of delaying projects until the national grid is rehabilitated, authorities have shifted responsibility to private operators while protecting the country’s fragile electricity system from additional demand.

Practicalities, not theory.

Yes, now Chevron occupies a unique position. Having maintained a presence through years of political uncertainty, the company possesses existing infrastructure, experienced personnel and producing assets that can be expanded more rapidly than those of new entrants.

At the same time, Chevron is no longer operating in an environment with limited competition.

Repsol is poised to take back operational control of its Venezuelan oil assets and triple production within three years. It wants to establish a ‘guaranteed’ payment system that will mean Caracas will always pay up.

Importantly, this new deal doesn’t include a specific commitment by the Venezuelan government to pay back the $4.55 billion Repsol says it is owed for natural gas and oil it was not paid for.

Are they letting it go? Not on the balance sheet, but in real life, it looks like they’ve made a calculation.

For context, Repsol is one of the largest foreign investors in Venezuela. It owns a 40% stake in the Petroquiriquire oil asset with the remainder owned by PDVSA. The resource contains three onshore oilfields, which currently produce about 45,000 b/d.

Repsol is also a partner with Italy’s Eni in the Perla gasfield, an offshore development that supplies gas to the domestic market in Venezuela.

And when international traders, independent producers and refiners are also all seeking positions within Venezuela, we’re seeing a far more competitive commercial environment than existed under previous sanctions regimes.

Further, the government’s recently announced regulatory reforms extend well beyond encouraging foreign participation.

The new regulations for the revised Organic Hydrocarbons Law seek to simplify project approvals, provide greater legal certainty for investors and modernise a framework that had become synonymous with state control and regulatory unpredictability.

For those risking their capital, the significance of these reforms is that they signal a durable commitment to stable investment conditions - and for everyone, not just Repsol.

In other words, a framework that applies to all.

Certainty.

Which, when you’re deploying hundreds of millions of dollars of non-refundable capital expenditure, is key (I’m looking at you, North Sea).

The devastating earthquakes that recently struck Venezuela have given these reforms additional urgency. Reconstruction will require massive capital, not only to rebuild damaged infrastructure but also to restore transportation networks, ports, industrial facilities and public services.

Oil revenues are expected to provide the financial foundation for that effort.

The bottom line is that the global energy industry is behaving as though Venezuela’s long period of isolation is over.

And Greig Gilbert - whose childhood was formed among the rigs of Anaco - is, in the words of Bloomberg, “looking for deals in exploration and production, oil services and even manufacturing.’

‘We have equipment, people and expertise and are ready to roll into Venezuela. Will it open up in the most perfect way? Probably not, but it has given us this opportunity.’

An opening, one might say.

As Bloomberg, the Financial Times and the US President are aware, they’re not the only ones. The scale of the rush is hard to overstate.

Miami-based Lionheart Capital has opened talks to merge its Nasdaq-listed blank-cheque vehicle with Keo Energy, aiming to build the first US-listed pure-play on Venezuelan oil at a roughly $1 billion valuation — centered on Maracaibo Basin fields that once produced hundreds of thousands of barrels a day and now limp along at under 2,000.

Formentera Partners, the Austin private equity group co-founded by Bryan Sheffield, has sent a team to assess opportunities after meetings with Venezuela's interim government.

In 2022, Sheffield’s private entity Sheffield Holdings LP initiated a strategic $16 million private placement to acquire a circa 9% shareholding block in Falcon Oil & Gas and a 2% overriding royalty interest over Falcon’s highly lucrative Beetaloo Basin permits in Australia.

Falcon was sold to Tamboran Resources for $172 million on 29 May.

Yeah.

Ali Moshiri, another Chevron former employee and once head of Latin American operations, is raising $2 billion through his Amos Global Energy fund and says he has already identified multiple assets to target.

Interestingly, in June 2016, our proposed non-exec Steele was appointed as the General Manager of Strategy, Planning and Commercial for Chevron Africa and Latin America Exploration & Production (CALAEP).

At that exact time, Moshiri was the President of that exact same division (CALAEP). Because Steele’s role was to handle the strategy, financial planning, and commercial activities for the region, he was a key functional leader operating directly within Moshiri’s leadership team.

In other words, the pair were the dream team.

Interesting.

Trump-linked Yorkville Advisors, which is invested in plenty of UK small caps - ranging from the recently IPO’d Reveille Resources to Ariana and beyond - has set up a $200 million SPAC to buy into the country.

I wonder who they might target.

Set against the current landscape — Lionheart working through a merger it hasn’t yet closed, Formentera still in the assessment phase, Moshiri still raising his fund — Apertura’s argument is essentially that being early with cash isn’t the same as being early with capability.

Venezuela’s reopening is creating dozens of opportunities that look attractive on paper - idle fields, cheap valuations, a state oil company (PDVSA) newly required to cede operational control.

As capital flows into Venezuelan assets from a range of new entrants, the execution side — rigs, crews, in-country operations — will be the gating factor for turning deals into production.

Apertura is positioning to be that execution partner - working alongside deal-makers and asset owners to get the oil flowing once the paperwork is signed.

One single asset acquisition - anything north of 25,000 barrels a day - and this thing goes vertical.

(Risks apply, but you know that.)

My goodness that is very well researched and nicely written, as always.

Great analysis.

nse venture new stratus energy might also be a interesting tool to enter Venezuela.