Amaroq Ltd.

The Only Way to Play Greenland

Good Morning Team.

I’ve been invested in Amaroq for several years now, and it’s been a rewarding few years.

And three months ago, I took advantage of what I perceived to be unfair share price weakness by doubling down on what was already one of my largest positions.

The stock kept falling for a few more nail-biting days, and then it started to recover.

This week’s operational update and Eldur’s stellar interview are all I need to know.

The conviction has once again paid off and the stock is rapidly recovering from its summer drop.

With the Pentagon planning to stockpile $1 billion of critical minerals, oil low, gold at $4,000 and Greenland/AMRQ firmly in the Trump’s mind, where next?

Let’s consider.

AMRQ is a producing gold miner with district-scale potential, critical minerals optionality and unprecedented government backing.

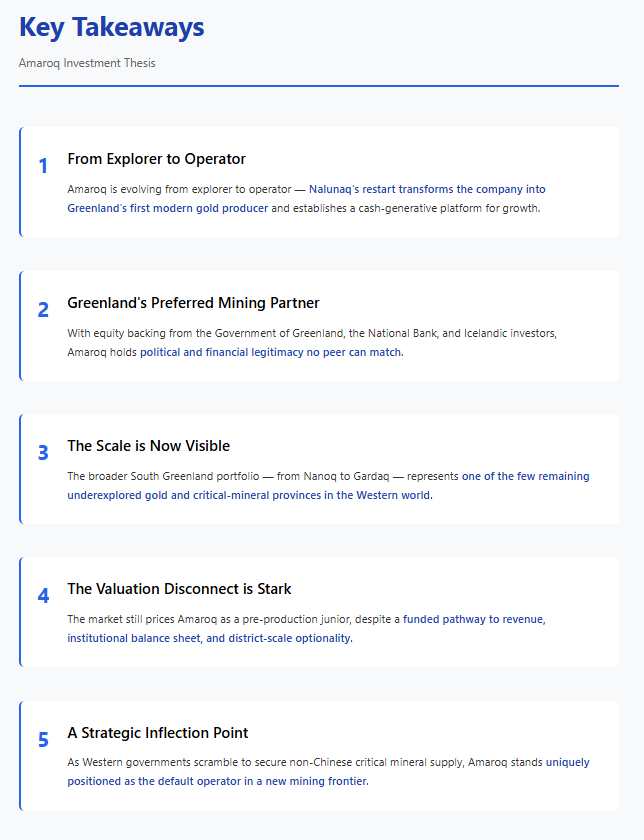

Amaroq has achieved what no other modern mining company has managed: building and operating a mine in Greenland.

Not just permitting it, not just studying it, actually producing gold from one of the world’s highest-grade deposits while simultaneously executing an extremely ambitious exploration campaign.

And they’re doing it with a fortress-like balance sheet, no debt, and the explicit support of governments on both sides of the Atlantic who suddenly care very deeply about where their critical minerals come from.

The market values Amaroq at roughly £400 million. By late 2026, if management executes on even half of what they’ve laid out, this company should be worth significantly more than that.

The near-term noise around commissioning schedules and production guidance adjustments has created an entry point that won’t last once the market fully appreciates what’s being built here.

Here’s the full investment case for why Amaroq represents one of the most compelling risk-reward setups in mining today.

The Nalunaq Foundation: High-Grade Gold, Growing Cash Flow

Let’s start with with the key to the investment case: Amaroq is producing gold from a world-class deposit.

Nalunaq grades 30 grams per ton. For context, most ‘high-grade’ gold mines today run 5-10 g/t. The major producers - Barrick, Newmont, Agnico - operate at 1-2 g/t and make it work through scale.

Nalunaq is in a different league entirely.

The mine was previously operated from 2003 to 2013 before closing due to low gold prices and high operating costs under the previous operator’s management.

Amaroq acquired the asset in 2015 and spent the next few years doing what good mining companies do: drilling, developing, and de-risking.

They put 40,000 to 50,000 metres of underground drilling into understanding the deposit, built out infrastructure, and then poured first gold.

The current resource stands at:

Indicated Mineral Resource of 151kt @ 32.4g/t Au for 157.6koz Au, with an additional 348kt @ 29.2g/t Au for 326.3koz Au.

But here’s what matters more than the current resource: the deposit is open in every direction.

The geological team can literally see the gold vein continuing up the mountain.

They’ve traced it down-dip for 250 metres beneath the valley. There’s a parallel structure called Zone 75 that’s already been drilled. Exploration could yield over 2 million ounces.

For context, the April 2025 resource update delivered a 51% increase in contained gold, and that was before the 2025 drilling program even started. Every time they drill, they find more gold. The question isn’t whether Nalunaq will grow - it’s how much and how fast.

On the operational front, the commissioning phase has exceeded expectations at every turn. By Q3 2025, processing throughput had increased 3.6 times quarter-over-quarter. Mining ore production jumped 2.6 times. In July, the plant was running at 145 tonnes per day on a single shift — halfway to the year-end target of 300tpd.

By late Q3, they’d moved to a double-shift pattern ahead of schedule.

By 7 October 2025, the company had produced approximately 5,000 ounces of gold. That was the guidance for the entire year. Production is running ahead of plan, not behind it.

Now, here’s where it gets interesting from an investment timing perspective. In June 2025, Amaroq completed an oversubscribed fundraise of £45 million from institutional investors who clearly wanted in. The company wasn’t actively seeking capital - they had tens of millions in liquidity and no debt - but when sophisticated institutions come knocking with that kind of enthusiasm, you take the money and accelerate your plans.

Management made a strategic decision to bring forward the installation of Phase 2 flotation recovery systems, which requires temporarily halting gold processing in October 2025 for about four weeks.

This pushed full-year production guidance down to 5,000 ounces from the previous 5,000 to 20,000 ounce range. The market, being the blunt instrument it often is, sold off on the headline without appreciating the nuance.

The guidance reduction isn’t a problem.

By completing Phase 2 during favourable summer weather rather than waiting until next year, Amaroq accelerates the timeline to higher recovery rates and significantly improved cash flow. They’re optimising for 2026 and beyond, not chasing 2025 production numbers that don’t matter in the grand scheme of building a multi-decade mining operation.

Once Phase 2 is complete in Q1 2026 and the plant is running at 300tpd nameplate capacity, we’re looking at a production profile of 40,000 to 50,000 ounces annually at conservative 15 g/t average feed grades. At current gold prices around $4,000 per ounce you can see the attraction.

But Nalunaq is just the beginning. The real leverage comes from what’s being discovered around it.

Nanoq: The District-Scale Opportunity

Thirty kilometres from Nalunaq sits what could be the most significant gold discovery Greenland has seen in decades.

The Nanoq project represents exactly the kind of exploration upside that can transform a company from single asset producer to district scale operator.

The 2024 drilling campaign at Nanoq returned high-grade gold intersections from multiple saddle reef structures.

For those unfamiliar with the geology, saddle reefs are highly predictable mineralisation styles that tend to be continuous, high-grade and massive. They’re the reason Victorian-era gold rushes happened.

You find one, you follow it, and you generally find a lot more.

At Nanoq, the surface expression shows folded vein systems over one kilometre in strike length. The geophysical signatures are strong. The geological model makes sense. And most importantly, the initial drilling confirmed what the surface mapping suggested: this thing is big.

The 2025 program has wrapped with 4,804 metres of core drilling completed on schedule. The team established a 45-person camp with on-site facilities allowing them to log, cut and sample core in real time. This isn’t helicopter-supported exploration where you’re flying in and out burning cash, but systematic work that only a company with Amaroq’s infrastructure and experience could pull off.

Initial assay results are expected in Q4 2025.

If those results confirm high-grade continuity at depth - and the geological model strongly suggests they will - Nanoq could host resources exceeding Nalunaq itself. Olafsson stated in his recent interview that he believes Nanoq could be considerably larger than their flagship mine.

Given that Nalunaq already has 484,000 ounces with 2 million ounces potentially to be discovered overall, ‘considerably larger’ is a big statement.

But here’s why Nanoq matters beyond just the ounces: proximity to infrastructure. The deposit sits 30 kilometres from Nalunaq’s processing plant. Ore can be barged over and run through existing mills, eliminating the single largest capex item in mine development. The economics of satellite deposits feeding a central processing hub are vastly superior to standalone operations, particularly in remote jurisdictions.

Amaroq is building a hub-and-spoke model across the entire Nanortalik gold belt - a 200+ kilometer trend that the company has systematically locked up through strategic license acquisitions. They own the whole belt. Every significant gold showing in South Greenland flows through Amaroq’s land package.

That positioning is worth far more than the current market valuation suggests.

Beyond Nanoq, there’s Naalagaaffiup Portornga (I can’t pronounce it either), which shows surface grades exceeding 2,000 g/t and has already been drilled.

There’s Vagar, where systematic surface work is defining targets.

There’s Anoritooq, where early-stage reconnaissance is identifying new prospects.

Each of these is a potential satellite feeder to Nalunaq’s processing capacity, which can be expanded from 300tpd to 450tpd with minimal incremental capex once additional mine fronts are opened.

The West Greenland Hub: Building the Second Production Centre

In June 2025, Amaroq acquired the past-producing Black Angel zinc-lead-silver mine and adjacent Kangerluarsuk licenses, creating what they’re calling the West Greenland Hub.

This move accomplished two things: it cemented Amaroq’s position as Greenland’s largest acreage holder, and it gave them a clear path to becoming a multi-commodity producer with operations spanning the entire country.

Black Angel isn’t a speculative grassroots project. It was operated by Cominco (now Teck Resources) from 1973 to 1990, producing over 11 million tonnes at combined grades of 12-15% zinc-lead plus silver over 17 years.

This was a real mine that made real money until commodity prices made it uneconomic.

Fast forward 35 years and the economics look completely different. Zinc prices are strong, sitting around $3,000 per tonne versus the $1,000-1,500 range that prevailed for much of Black Angel’s operating life. Modern mining methods dramatically reduce costs and improve recoveries. And the kicker? Most of the infrastructure is still there.

The site has accommodation for 20+ people, helicopter hangars, cable car equipment, a deep-water port, and extensive historical drilling and mine workings. Just building a camp and logistics hub in Greenland costs $3 to $5 million - that’s already in place. The airstrip, the port facilities, the basic infrastructure required to operate in a remote Arctic location - it’s all there, waiting to be reactivated.

The current resource stands at 4.4 million tonnes. Amaroq’s plan is straightforward: drill aggressively through 2026 to expand that to 10+ million tonnes, focusing on the Glacier Zone and Deep Ice Zone where the retreating glacier has exposed new mineralisation. Conduct bulk sampling to confirm metallurgy. Update the resource model.

Then make a production restart decision.

This is the Nalunaq playbook applied to base metals: acquire a brownfield asset with existing infrastructure, drill to expand resources, de-risk through systematic work, then restart operations leveraging everything that’s already built.

It’s a proven strategy that dramatically reduces both capital requirements and development timelines compared to greenfield projects.

Adjacent to Black Angel sits Kangerluarsuk, which shows similar geological signatures to Nanoq - with saddle reef structures that could host significant tonnage. If the 2026 initial drilling confirms the geophysical anomalies and geological model, Amaroq could be looking at a symmetric position in West Greenland: two major base metal deposits (Black Angel and Kangerluarsuk) just as they’re building in South Greenland with Nalunaq and Nanoq.

The strategic value of this approach is hard to overstate.

Geographic diversification reduces operational risk. Commodity diversification provides optionality across different metal price environments. And the infrastructure leverage (using existing camps, ports, and logistics chains to support both operations and satellite discoveries) creates competitive advantages that are nearly impossible for newcomers to replicate.

By 2028 or so, if everything executes as planned, Amaroq could be operating two mines, producing 80,000-100,000 ounces of gold annually plus meaningful zinc-lead-silver production, all supported by a services business and hydroelectric operations.

Of course, everything has to go right first.

Critical Minerals: The Strategic Wildcard

While gold gets the headlines and provides the cash flow, Amaroq’s critical minerals portfolio could ultimately prove to be the most valuable part of the business.

The company holds exploration licenses across copper, nickel-copper-cobalt, and rare earth elements through a joint venture structure that shares both risk and upside with strategic partners.

This Gardaq JV, in which Amaroq holds 51% and GCAM holds 49%, was structured in 2022 with GCAM contributing $30 million CAD in exploration funding.

Over the past three years, this partnership has made some significant discoveries that have flown under the radar while the market focused on Nalunaq’s commissioning.

Under the guidance of Dr Steve Garwin, the exploration team discovered an entirely new copper belt in Archean geology that had been overlooked because it doesn’t fit the typical porphyry or epithermal models most explorers look for.

But it’s very similar to copper systems found in Pakistan and Saudi Arabia - older geology, different mineralisation style, but economically viable at scale.

The Ukaleq prospect is perhaps the most advanced target, with remote sensing datasets and previous exploration results guiding systematic targeting for epithermal or porphyry-style mineralisation.

Scout drilling is contingent on positive surface results from 2025, with a full drilling campaign planned for 2026 if the initial work pans out.

At Stendalen, the team has drilled through disseminated nickel-copper mineralisation over 140+ metres and is continuing to drill to locate massive sulfides.

The comparison being made internally is to Vale’s Voisey’s Bay deposit in Canada.

Voisey’s Bay contains roughly 141 million tonnes at 1.6% nickel, 0.9% copper, and 0.1% cobalt, and is one of the world’s premier nickel sulfide deposits. If Stendalen proves to be even a fraction of that scale, it would be transformational.

The rare earth element portfolio spans multiple licenses across the Gardar Igneous Province, one of Greenland’s most prospective REE regions. Following new license awards in 2025, Amaroq significantly expanded its regional exploration targeting both confirmed and newly identified REE targets.

There’s also the Minturn IOCG (Iron Oxide Copper Gold) project in Northwest Greenland, where a new license application is pending. IOCG deposits are particularly interesting because they can host multiple commodities - copper, gold, uranium, rare earths - in a single system, offering exceptional economics.

Now, here’s the critical context that makes these projects far more valuable than typical early stage exploration.

Governments on both sides of the Atlantic are actively seeking to fund and support them.

The geopolitical landscape around critical minerals has fundamentally shifted.

China controls roughly 80-90% of rare earth processing capacity globally. They dominate graphite production, hold significant positions in copper and nickel supply chains, and have recently imposed export controls on graphite, two rare earth elements, antimony and tungsten. Titanium controls are expected next.

Western governments finally understand that this is a national security vulnerability, not just an economic issue.

The response has been unprecedented. The US Defense Production Act has been invoked for critical minerals. Critical minerals stocks have become defence stocks,

The Department of Defense is providing direct financing - MP Materials received a $150 million loan plus $400 million in direct equity investment plus an offtake agreement with a price floor. The US Export-Import Bank (EXIM) is considering a $120 million loan for the Tanbreez rare earth project in Greenland. The EU designated the nearby Amitsoq project in Greenland as ‘strategic’ under the Critical Raw Materials Act.

And here’s the most important part for Amaroq investors: CEO Eldur Olafsson has stated publicly that the company is in active discussions with multiple state-backed agencies across both sides of the Atlantic about various forms of support. State loans, offtake agreements and direct investments - multiple mechanisms are on the table.

When Denmark’s state-backed investment fund EIFO committed $15.4 million to Amaroq’s June 2025 fundraise, that was a strategic positioning move. When the raise was oversubscribed despite reduced near-term production guidance, that told you everything about what institutions expect to happen next.

The critical minerals portfolio isn’t going to generate cash flow in 2026. But if any of these projects advance with government backing, the market will revalue Amaroq overnight.

Copper, nickel, and rare earths in a Western-aligned jurisdiction with government support could be worth more than the gold business.

And currently, the market is valuing them at approximately zero.

Why Amaroq Has No Real Competitors

Here’s something the market consistently undervalues: operational capability in extreme environments is worth far more than exploration licenses. Greenland isn’t a jurisdiction where you can show up, hire a contractor and start drilling.

Yes, many have tried.

There are no equipment rental companies. There are no established mining services firms. There’s no local expertise to tap into. You build everything from scratch or you don’t operate.

Since 2017, Amaroq has built the only properly functioning mining operation in modern Greenland. They employ 150 people in a region with limited labour pools. They’ve established year-round logistics chains despite challenging weather. They’ve navigated permitting successfully, with environmental and social impact assessments completed in 2-3 years versus 5-10+ years in Canada or Scandinavia.

They maintain strong relationships with the Greenlandic government, local communities and Danish authorities.

The infrastructure they’ve built represents tens of millions in sunk costs and years of operational learning. When you’re operating in South Greenland, your supplies come through Iceland. Personnel rotate through Reykjavik. Equipment mobilisation requires specialised logistics.

Consumables supply chains have to be established from nothing.

Camp construction in permafrost regions follows different rules than temperate mining districts.

Amaroq has figured all this out through experience. And yes, it’s not been easy getting here.

But they operate multiple field camps - a 45 person facility at Nanoq, a 20+ person capacity at Black Angel, the main 120 person camp at Nalunaq. They’ve established an on-site ALS laboratory for rapid assay turnaround. They’ve built ports, roads, tunnels and all the supporting infrastructure required for modern mining operations.

This expertise is so valuable that Amaroq has spun it out into a standalone services business called Suliaq, which will provide equipment and services to Greenland’s growing mining sector.

JLE Group has committed £4 million for a 10% stake, valuing the business at £40 million (roughly $52 million CAD). That valuation is for a services company that doesn’t even include the mining operations themselves - it’s purely the equipment leasing and technical consulting business.

The strategic logic here is brilliant. As more mines come online in Greenland (and they will, given government support and resource potential) the costs for all operators decline through shared infrastructure and logistics.

More importantly, Amaroq positions itself as the essential partner for anyone trying to operate in Greenland.

Want to drill? Rent our rigs.

Need logistics coordination? We’ve got the relationships.

Struggling with permitting? We’ve done it five times.

This creates network effects that compound competitive advantages over time. Anglo American wants to explore their licenses in the region? They’ll likely partner with or contract through Amaroq. Rare earth developers need field support? Same story. Government agencies want to back Greenland mining? There’s really only one company with proven operational capability.

Then there’s the hydroelectric business, IMEQ, which is developing at least 1 megawatt of hydro capacity near Nalunaq. The river that runs past the processing plant drops 70 metres — perfect for a small hydro installation that will reduce operating costs by roughly $2 million annually. Environmental and social impact licenses are already secured. The prefeasibility study is complete, and final permits are planned for 2026.

Amaroq will be the first private hydro developer in Greenland. That alone is significant, as it de-risks the model for others and establishes precedents. But more importantly, it creates a long-lived asset (30-50+ year operational life) that continues generating value long after mining operations eventually wind down. The electricity could supply future data centres, support town infrastructure in nearby Nanortalik, or enable other industrial projects.

What all this adds up to is a competitive moat that’s nearly impossible to replicate. You can’t just hire Amaroq’s advantage away. You can’t acquire it through M&A. You’d have to spend a decade and tens of millions of dollars learning what they already know while they continue advancing their projects.

In practical terms, Amaroq is Greenland mining. Anyone wanting exposure has to go through them.

The Geopolitical Accelerant

Let’s now consider Donald Trump and Greenland, because this matters more than the market currently appreciates.

During Trump’s first presidency in 2019, he floated the idea of purchasing Greenland from Denmark. The media treated it as a joke. But the strategic logic was sound then and has only strengthened since.

The Arctic ice is melting, opening new sea routes and tactical positions. Greenland sits at the centre of future Arctic shipping lanes and military positioning. China has been making overtures to Greenland for years, offering infrastructure investment and resource development funding. Russia maintains a significant Arctic military presence. From a US defense perspective, Greenland matters.

But beyond the military strategy, there’s the resource angle. Greenland has vast untapped reserves of rare earth elements, copper, nickel, graphite and other critical minerals that the US desperately needs to secure. Trump’s second term has seen renewed focus on Greenland, not as a real estate acquisition, but as a strategic partnership priority.

The institutional response to Amaroq’s June 2025 fundraise tells you that sophisticated investors understand something is happening. When Olafsson tells Bloomberg that multiple state-backed agencies are in discussions about backing businesses, backing mining projects, and securing mineral supplies, that’s not speculation.

The precedent has already been set. MP Materials, the only operating rare earth mine in the US, secured $150 million in Department of Defense financing plus $400 million in direct equity investment plus an offtake agreement with a price floor. Guardian Metal Resources, which owns the largest undeveloped tungsten deposit on US soil, is receiving grant funding. The US government is no longer sitting on the sidelines waiting for the private sector to solve critical mineral supply chains — they’re actively deploying capital.

Amaroq’s portfolio positions them perfectly for this support. Gold production provides immediate operational credibility and cash flow.

The critical minerals portfolio — copper, nickel, rare earths —aligns directly with US government priorities. The West Greenland Hub creates geographic diversification.

And most importantly, Amaroq has the operational track record that governments require before deploying taxpayer capital.

The potential mechanisms are diverse: state loans at below-market rates, offtake agreements providing revenue certainty and price floors, direct equity investments at premium valuations, infrastructure grants co-funding ports or power systems, or even technical assistance through government labs and geological surveys.

Any combination of these could accelerate Amaroq’s development timeline by anywhere between two to five years and reduce capital requirements by 30-50%.

But here’s the really interesting part: offtake agreements would solve the single biggest challenge in Greenlandic mining. It’s not the geology - that’s excellent. It’s not the weather - manageable with proper planning. It’s not even the operating costs, because high-grade deposits offset remote location expenses.

The challenge has always been securing customers willing to commit to sourcing from a remote, emerging jurisdiction. Government offtakes eliminate that problem entirely.

If the US government signs an offtake agreement for Amaroq’s copper, nickel or rare earth production - guaranteeing purchase at floor prices - that’s a company-transforming event.

It’s not priced into the current market cap because it hasn’t been announced yet. But the discussions are happening. The precedents exist. And the geopolitical urgency is only increasing.

The Financial Fortress

One of the most underappreciated aspects of Amaroq’s investment case is the balance sheet. As of Q2 2025, the company had group liquidity of $75 million - consisting of $86 million in cash, plus $8.9 million in undrawn credit facilities, less $19.8 million in trade payables. They’re completely debt-free.

The monthly operating budget targeting for 2026, once commissioning capex is complete, is around $5 million USD for all-in sustaining costs across the entire company. With gold production ramping to 10,000+ ounces per quarter at $4,000 gold, the free cash flow will be sickening.

This is not like every other new gold producer (leveraged to their eyeballs and praying for good luck).

Amaroq isn’t burning cash hoping to raise capital for construction. They’re not leveraged to the point where a six-month delay means covenant breaches and death spirals. They’re not going to be forced into dilutive raises at market bottoms.

They have flexibility.

That flexibility allows them to pursue multiple opportunities simultaneously. They can fund aggressive exploration across all their projects — Nanoq, Black Angel, copper, nickel and rare earths— without choosing between them.

They can wait for optimal market conditions before making major capital allocation decisions. They can walk away from government support if terms aren’t favorable. They have leverage in negotiations precisely because they don’t need the money desperately.

For investors, this dramatically reduces risk. The typical mining story goes something like this:

Promising geology → good management team → they build a mine on borrowed capital → commissioning has inevitable hiccups → cost overruns eat the contingency budget → they need to raise money in a weak market → existing shareholders get diluted at the worst possible time → and what should have been a 5x return turns into a 1.5x because the cap table got blown out during construction.

Amaroq has already avoided that entire scenario. They raised opportunistically in June 2025 at a premium to current prices when institutions wanted in. They’re completing commissioning ahead of schedule. Production is running ahead of guidance. The balance sheet is bulletproof.

Any future capital raises, if they happen at all, will likely be strategic (funding M&A opportunities) rather than desperate (covering operational shortfalls).

Management has explicitly stated they don’t foresee needing any capital raises to support ongoing operations. With government support potentially providing non-dilutive financing for critical minerals projects, the odds of meaningful dilution are low.

Long-Term, Strategic Capital

Here’s another signal the market isn’t fully appreciating: look at who owns Amaroq.

The vast majority of shareholders are long-only institutional investors, including pension funds, sovereign wealth funds and specialised resource funds that don’t trade in and out on quarterly results.

Management and the board own 11% of the company and have participated in every single funding round. More than 40% of shareholders are strategic investors with specific reasons for holding beyond just financial returns.

The register includes the Danish sovereign wealth fund, Greenland’s sovereign fund, the only pension fund in Greenland, multiple Danish and Nordic pension funds, US critical minerals funds and European gold funds. This is an exceptionally high-quality shareholder base.

Sophisticated institutions with deep resources for due diligence have looked at Amaroq and decided it’s worth significant capital allocation. These are pension funds managing multi-billion dollar portfolios who need real assets with long-term value creation potential.

When that shareholder base participates in an oversubscribed fundraise despite reduced near-term production guidance, they’re signalling that they understand the strategic rationale and approve of the accelerated optimisation approach.

When sovereign funds from both Denmark and Greenland hold positions, they’re signaling confidence in the political and regulatory environment.

When US institutions are buying, they’re positioning for the government support catalyst that they likely have better visibility into than retail investors do.

The planned Main Market uplisting in London during 2026 will unlock access to even larger institutional mandates and index inclusion. Currently listed on AIM, TSX-V, and NASDAQ Iceland, with OTCQX trading in the US, Amaroq has good liquidity across multiple venues.

But a Main Market listing opens up FTSE index inclusion and the institutional mandates that require main market listings.

Valuation: The Opportunity Hiding in Plain Sight

Let’s talk about what Amaroq is actually worth versus what it’s trading for. The current market capitalisation sits around $700 million CAD, which translates to an enterprise value of roughly $614 million CAD (about $448 million USD) after backing out the net cash position.

On an EV per resource ounce basis, Amaroq trades at approximately $1,300 per ounce. Comparable gold producers trade at $2,000 to $3,500 per ounce depending on jurisdiction, mine life, and production status.

On an EV per 2027 estimated production ounce basis (assuming 40,000-50,000 oz), Amaroq trades at roughly $14,000 per ounce. Comparable producers trade at $8,000 to $10,000 per ounce.

Now you can argue about jurisdiction discounts and commissioning risk, and those arguments have some merit. But what the market is fundamentally missing is that none of the strategic value is priced in.

The Nanoq discovery potential — zero value in current price.

The Black Angel hub with 10+ million tonne resource potential — zero value.

The critical minerals portfolio with government support optionality— zero value.

The services business worth £40 million to a strategic investor —zero value.

The Greenland operational monopoly that makes Amaroq the necessary partner for anyone wanting exposure — zero value.

The bull case, where Nanoq confirms district-scale potential (500,000+ oz), government support materialises, and the Main Market uplisting drives index inclusion, points to $1 billion USD or more, representing huge upside.

Given the near-term catalysts queuing up (Q3 results in November, Nanoq assays in Q4, resource update in Q1 2026), that bull case doesn’t require years of patience.

It could play out over 12-18 months.

The Catalysts Are Queuing Up

Amaroq’s story is packed with near-term catalysts — across production, exploration, expansion, and potential government support — that could materially re-rate the company’s valuation over the next 12–18 months.

1. Q3 2025 Results — November 14, 2025

Confirmation of shutdown completion and Phase 2 restart timeline.

Updated production guidance for late 2025 and into 2026.

Early production strength: already hit 5,000 oz by early October, ahead of full-year guidance.

This is management’s chance to reset expectations and provide visibility into steady-state operations.

2. Nanoq Assay Results — Q4 2025

Results from 4,804m drilling program start coming through.

Major catalyst: if assays confirm high-grade continuity at depth across multiple veins,

→ Nanoq becomes a district-scale opportunity.Expect market re-rating on confirmation of scale and grade.

Resource estimates will follow later, but initial assays should be enough for retail interest.

3. Nalunaq Drilling & Resource Update — Q4 2025 → Q1 2026

Results from:

South Block Deeps drilling (250m down-dip)

Underground drilling (725–790 levels)

Feed into next Mineral Resource Estimate (MRE) due Q1 2026.

April 2025 MRE showed a 51% increase; 2025 drilling was even larger.

→ Expect further upgrades in both indicated and inferred categories.

4. Phase 2 Commissioning — Q1 2026

Flotation circuit commissioning complete.

Automation of the gravity circuit → higher recovery rates.

Path toward 450tpd capacity becomes clear.

Updated MRE likely includes:

Nalunaq resource growth

Potential maiden Nanoq resource

Extended mine life projections

5. Sustained Operations & Cash Flow — Q2 2026

Target: 300tpd sustained operations, then onto 400tpd.

Quarterly production: 10,000–12,500 oz (assuming 15 g/t).

Annualized: 40,000–50,000 oz/year.

Investment thesis shifts from:

→ ‘Can they execute?’

→ ‘How much cash flow can they generate, and where will it go?’

6. Main Market Uplisting — 2026

Planned London Main Market listing (Spring or Autumn).

Opens access to institutional mandates, index inclusion and passive fund inflows

Management has confirmed this as a strategic priority.

Structural buying from index trackers could be meaningful.

7. Exploration & Critical Minerals Optionality — 2026

Black Angel: aggressive drilling to grow from 4.4 Mt → 10+ Mt.

Kangerluarsuk: initial drilling to test saddle reef hypothesis.

Broader critical minerals portfolio progress:

Copper: Ukaleq and others

Nickel-Copper: Stendalen

Rare Earths: early-stage programs

IOCG: Minturn project

Each success here adds optionality and potential valuation uplift.

8. Government Support Potential — Anytime

Possible announcements include:

State-backed loans

Offtake agreements

Direct government investment

Any such support would further de-risk and re-rate Amaroq’s growth trajectory.

By Late 2026

If even half of these catalysts execute as planned, Amaroq could be:

Producing 40,000–50,000 oz/year of gold

Generating tens of millions in free cash flow

Holding a defined Nanoq resource with development underway

Advancing Black Angel toward restart

Operating under a government-backed critical minerals framework

At that point, the company should command a valuation well above what it does today.

Why Now: Three Factors Converging

The investment opportunity in Amaroq exists because three separate factors are converging in late 2025 and early 2026 that create a particularly attractive entry point.

First, the operational inflection point. Mining companies typically re-rate from first gold pour to steady-state production as execution risk declines and cash flow visibility improves.

Amaroq is still navigating the commissioning phase. The market is treating them with development-stage scepticism despite production running ahead of schedule. By Q2 2026, when 300 tpd operations are sustained and commercial production is declared, that scepticism evaporates and Amaroq gets valued as an operating producer.

Right now, you’re getting producing-miner upside at development-stage prices.

Second, the exploration newsflow acceleration. The company is completing the most extensive drilling program in its history —8,500+ meters across seven active projects. Results are coming in Q4 2025 and Q1 2026. Nanoq alone could be a company-making discovery. The Nalunaq resource update should show significant growth. Black Angel and critical minerals results provide additional optionality.

All of this newsflow hits over the next six months while the stock is still digesting the June guidance reduction that the market misunderstood. There’s a significant gap between operational reality and market perception that’s about to close.

Third, the government support clarification. CEO Olafsson isn’t speculating about government interest — he’s describing active negotiations with state-backed agencies. The precedent exists with MP Materials receiving $550 million in combined financing and equity from the US government. The geopolitical urgency around critical mineral supply chains is increasing, not decreasing.

China’s export controls on key materials are forcing Western governments to act. At some point in 2025 or 2026, something gets announced. When it does, the critical minerals portfolio that’s currently valued at zero suddenly has real value.

These three factors together create a compelling setup.

Near-term catalysts (Q3 results, Nanoq assays), medium-term operational milestones (commercial production, resource update), and longer-term strategic developments (government support, Main Market listing) all queue up over the next nine months. You don’t need to wait five years to see if the thesis plays out. You’ll know by mid-2026.

What Success Looks Like: The 2027 Vision

Let’s paint the picture of what Amaroq could look like in late 2027 if management executes on their stated plans and even some of the upside scenarios play out.

Nalunaq is operating at 450 tonnes per day, producing 60,000-75,000 ounces of gold annually. With gold at $4,000 per ounce, that’s an insane amount of cash generation.

The deposit continues growing through systematic drilling. Mine life extends beyond 15 years. The underground infrastructure supports higher throughput if warranted.

Nanoq has a defined resource of 300,000-500,000 ounces confirmed through 2025-2026 drilling campaigns. Development is underway with ore being barged to Nalunaq for processing. First Nanoq production occurs in late 2027 or early 2028. Combined Nalunaq-Nanoq production reaches 80,000-100,000 ounces annually within 18 months.

The district-scale model is proven, with additional satellite prospects identified along the Nanortalik belt.

Black Angel resource has been expanded to 10+ million tonnes through aggressive 2026-2027 drilling. Bulk sampling confirms metallurgy and supports previous mining assumptions. Production restart decision is made with first zinc-lead-silver concentrate scheduled for 2029.

Kangerluarsuk initial drilling identifies significant tonnage potential, confirming the West Greenland Hub as Amaroq’s second major district.

The critical minerals portfolio sees meaningful progress on multiple fronts. Stendalen nickel-copper drilling locates massive sulfides, confirming a deposit analogous to Voisey’s Bay at some meaningful fraction of scale. Copper belt drilling advances Ukaleq toward resource definition.

Rare earth targets are prioritised based on government support framework that has been announced and is being implemented. At least one critical minerals project receives state-backed financing or an offtake agreement, validating the government support thesis.

The services business, Suliaq, is operating profitably serving Amaroq’s projects plus at least two other operators who have established presence in Greenland. Equipment utilisation is high. The business generates steady cash flow and positions Amaroq at the centre of Greenland’s mining ecosystem.

The hydroelectric project, IMEQ, is operational, reducing Nalunaq’s operating costs by $2 million annually while providing long-term infrastructure that benefits both mining operations and local communities. Additional hydro sites are being evaluated for development.

The company is listed on London’s Main Market with inclusion in relevant FTSE indices. Analyst coverage has expanded from limited sell-side research to comprehensive coverage from major banks.

Institutional ownership has increased driven by index inclusion and the operational de-risking. Liquidity has improved across all listing venues.

The market capitalisation sits at $1.5-2.0 billion CAD, reflecting the transformation from single-asset producer to district-scale multi-commodity mining company with significant exploration upside, government backing, and irreplaceable infrastructure position in a strategic jurisdiction.

That’s execution on stated plans with reasonable success rates on exploration programs. Every element described is either already underway (Nalunaq expansion, Nanoq drilling, Black Angel acquisition) or logical next steps based on current trajectories (resource definition, government support, Main Market listing).

The Bottom Line

Here’s the core investment thesis distilled to its essence: Amaroq Minerals is the only company that can actually execute in Greenland. They’ve proven it by building and operating the only modern mine there.

They have the infrastructure, relationships, and expertise that competitors would need a decade to replicate. They’re producing gold from a 30 g/t deposit with district-scale exploration upside.

They’re exploring for critical minerals at exactly the moment when Western governments are desperate to secure supply chains outside Chinese control. And they’re trading at a substantial discount to fair value based on current assets alone, with none of the strategic upside priced in.

For investors who do their own work, understand the mining sector, and can tolerate near-term volatility in exchange for medium-term re-rating potential, Amaroq represents one of the best risk-reward setups available today.

The gold production provides downside protection and cash flow. The exploration portfolio provides upside leverage. The critical minerals exposure provides optionality on the government support megatrend. And the valuation provides entry at levels that won’t exist once the market catches up to operational reality.

By mid-2026, Amaroq should be producing meaningful gold, generating real free cash flow, sitting on expanded resources at both Nalunaq and Nanoq, advancing Black Angel toward restart, and potentially operating under government support frameworks for critical minerals.

The question isn’t whether Amaroq is a good company — the operational track record and institutional backing confirm it is.

The question is just how much better it can get.

That is one impressive report Charles that must have taken ages to write. The potential upside to the SP seems astounding. Thanks

Way to go Charles, thanks for this article, this is especially relevant in 2026. YOLOing 100$ into this and will soon add more.