Alien Metals

Market Cap vs Net Asset Value

After interviewing Bruce recently, I wanted to revisit the investment thesis for Alien Metals and consider where the company now sits — and where it could realistically go next.

The simplest place to begin is with the gap between market capitalisation and underlying asset value.

Alien currently trades at a market cap of roughly £18 million.

Yet the implied value of Alien’s interests in West Coast Silver and GreenTech Metals stands at approximately £30.4 million. The Hancock iron ore assets are likely worth around A$15–16 million (circa £7.6 million) if disposed of today, giving a core NAV of roughly £38 million.

In a rational market—where these equity interests and project stakes could be realised at fair value — Alien should trade well over 100% higher than today’s valuation.

In other words, at a share price close to 0.4p.

And that is before factoring in the considerable upside potential across both GreenTech and West Coast.

The Strategy: Monetise, Retain, Free-Carry

Under Bruce, Alien has executed a deliberate and coherent strategy: monetise assets through partnerships, retain meaningful free-carried exposure, take cash off the table to fund other priorities, and hold equity in partner companies to capture district-wide upside.

The result is a portfolio that increasingly resembles a royalty-style leveraged exposure to a multi-commodity district, without the capital intensity or dilution typically associated with junior exploration.

Elizabeth Hill: Template Deal

Before Munni Munni, there was Elizabeth Hill.

In May 2025, West Coast (via Crest Silver) acquired a 70% interest in the Elizabeth Hill tenement and 70% of the silver rights across the broader Pinderi Hill tenements. Alien retained 30% in both, free-carried through to a decision to mine.

Consideration to Alien was approximately A$2.5 million, comprising A$900,000 in cash and 44.5 million West Coast shares. Alien subsequently sold down 14 million shares, retaining 30.5 million shares, representing an effective ~9–10% equity stake.

West Coast concurrently raised A$3 million to fund drilling, which commenced shortly after deal completion. Alien deployed the cash toward working capital and advancing Hancock and Pinderi Hills.

This established the template: monetise the asset, retain free-carried exposure, fund core assets, and capture equity upside.

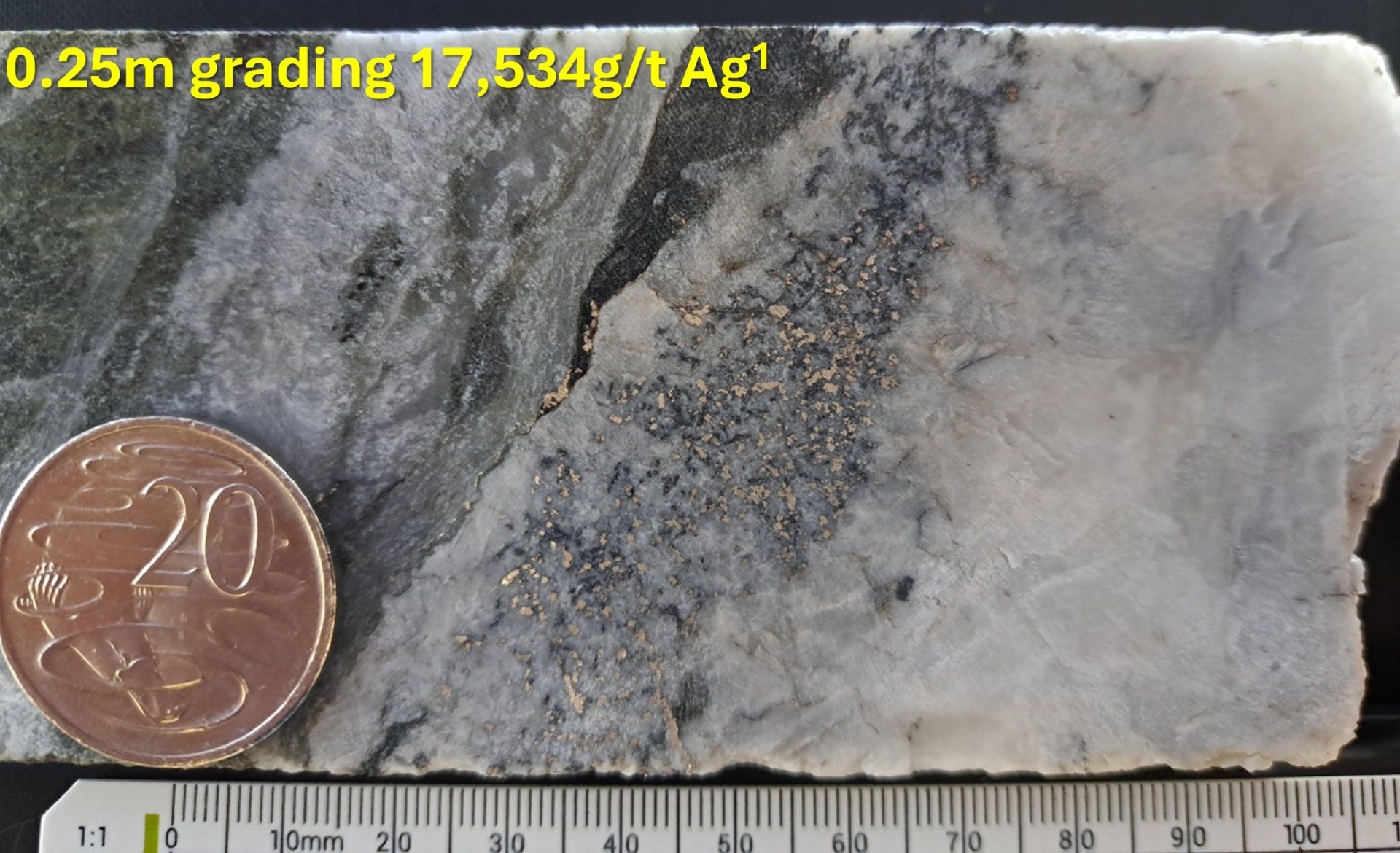

Elizabeth Hill: Bonanza-Grade Silver in a Modern Market

Elizabeth Hill is one of Australia’s highest-grade silver systems. Between 1994 and 2000, the mine produced 1.2 million ounces of silver from just 16,830 tonnes of ore at a head grade of 2,194 g/t—among the highest-grade silver production ever recorded in Australia.

Mining ceased due to low silver prices and JV disputes, not geology.

Modern drilling has validated and exceeded expectations. Recent Phase 2 diamond drilling delivered extraordinary results:

27.4m @ 1,314 g/t Ag from 49m

including 0.35m @ 33,107 g/t Ag

including 0.25m @ 17,534 g/t Ag

including 0.4m @ 16,291 g/t Ag

including 0.9m @ 5,290 g/t Ag

22.0m @ 578 g/t Ag from 6m

25.8m @ 151 g/t Ag from 20m

1.95m @ 1,252 g/t Ag from 54.6m

Bonanza-grade silver is typically defined as >500 g/t. Elizabeth Hill is delivering intervals well into the thousands.

The system remains open, with mineralisation extending beyond historical drilling.

West Coast is advancing toward a maiden JORC resource and evaluating processing at Artemis’ Radio Hill plant, which already hosts a gravity circuit suited to native silver recovery—potentially removing a major capital hurdle.

Alien retains full upside exposure, without funding obligations.

Munni Munni: Replicating the Playbook at Larger Scale

In December 2025, Alien executed a conditional sale agreement with GreenTech Metals for a 70% interest in the Munni Munni PGE project.

The structure mirrored Elizabeth Hill:

GreenTech acquired 70%

Alien retained 30% free-carried to bankable feasibility study

Consideration: A$500,000 cash + 47 million GreenTech shares (~A$6.11 million)

Alien now holds ~17.4% equity in GreenTech

GreenTech has an option to acquire an additional 10% via 20 million shares.

Munni Munni hosts a historical resource of 24Mt @ 2.9 g/t 4E PGE for ~2.2 million ounces (non-JORC 2012). Metallurgy is straightforward flotation-based, and the project sits on granted mining leases with extensive historical drilling.

Why 2Moz+ Matters

If a modern JORC resource exceeds 2 million ounces, Munni Munni transitions from a junior exploration story into strategic Tier-1 PGE territory. At that scale, valuation multiples expand and corporate interest becomes credible.

Copper: The Underappreciated Wildcard

GreenTech has recruited Kevin Frost via its advisory team—best known for identifying Chalice’s Julimar PGE-Cu-Ni discovery (PDAC Discovery of the Year, now a ~$1.5bn+ project).

Frost has already identified new advanced copper targets on the Munni Munni project.

This is significant. Copper is a critical metal with structural demand growth, and any meaningful Cu system could materially re-rate the district. Alien benefits from this technical firepower at no cost, and the copper angle remains largely unappreciated by the market.

The West Pilbara District Thesis

Munni Munni, Elizabeth Hill, and GreenTech’s Whundo copper-gold project sit within a tightly clustered district near Karratha. Shared infrastructure, processing, and geology could materially improve project economics.

Mining history shows district consolidation creates exponential value — Kambalda, Red Lake, and the BC Golden Triangle are classic examples. Alien sits at the centre of this emerging district with free-carried exposure to both silver and PGEs, plus equity leverage to both operators.

Iron Ore: Strategic Optionality, Not a Distraction

Alien retains 100% ownership of Hancock, Vivash, and Brockman iron ore assets. Hancock hosts an 8Mt DSO resource grading 58–62% Fe.

Approved iron ore mining leases are not easy to obtain, and there is no shortage of interest in Pilbara iron ore. Alien should not give these assets away cheaply.

Even at a conservative intrinsic value of ~£7.6 million today, Hancock contributes real underlying value and optionality — either as a development pathway or a sale asset.

Alien has engaged Mark Pudovskis, ex-BHP and part of the core team that built Fenix Resources from $5m to a $500m market cap. This materially strengthens the iron ore strategy.

Valuation Scenarios: Market Cap and Share Price

Using approximate figures (current market cap £18m, share price 0.17p):

If Alien traded purely at the value implied by its equity holdings and JV interests (excluding Hancock), a £30–35m market cap would be reasonable, implying a share price of roughly 0.29–0.33p.

Including Hancock’s intrinsic value lifts NAV to ~£38–45m, implying 0.36–0.43p per share.

If Munni Munni delivers a 2Moz+ JORC resource and Elizabeth Hill continues to expand, a district re-rating at 2–3x NAV implies £75–115m market cap, or ~0.7–1.1p per share.

What to Watch Next

Over the next 6–12 months:

Munni Munni drilling results and maiden JORC resource

Elizabeth Hill ongoing drilling and maiden JORC silver resource

Processing feasibility at Radio Hill

Whundo development studies

Hancock drilling and resource model updates

The Bottom Line

Alien has transformed itself from a capital-intensive junior explorer into a leveraged district exposure play. It holds free-carried stakes in two potentially world-class precious metal systems, equity in both operators, and 100% ownership of strategic Pilbara iron ore assets—all while avoiding dilution during the highest-risk exploration phase.

The market is valuing this portfolio at roughly half of its implied NAV.

If Munni Munni crosses the 2Moz threshold, if copper targets deliver, and if Elizabeth Hill continues to extend, Alien could sit at the centre of one of Australia’s most compelling emerging multi-commodity districts.

And right now, the sum of the parts is trading at a deep discount.