Ajax Resources

The Undervalued Copper-Gold Story You’ve Never Heard Of.

Good Morning Team.

As long-time readers will know, I’ve been a holder of Bezant Resources for some years. The company has delivered a strong return - but one asset I had my eye that ended up escaping its portfolio was the Eureka project in Argentina.

To be fair, Eureka (and other non-core disposals) simply did not make sense in a portfolio focused on African copper-gold mining.

If you want assets in Namibia, you need boots on the ground in Namibia. The same is true of Argentina.

But I was sad to see it go.

There’s good news though.

That same project is back – and this time, it’s in the hands of someone who can dedicate their focus to it.

Meet Ajax Resources (AQSE: AJAX).

This is a company that just started drilling a week ago at a project that has never seen a modern drill bit in its 400-year production history.

Let me explain why this matters, and why with gold now trading at $4,600/oz, the company is an early-stage potential winner.

Caveat for the newcomers: As ever, this is junior resource and as a sector is higher risk than almost everything else. The rewards are, however, commensurate.

Let’s dive in.

The Bezant Backstory

Bezant bought Eureka back in 2012 for around $7 million – roughly 38% cash, 62% paper. The plan was simple: rapid development of a copper-gold project that had historical estimates suggesting 520,000 to 616,000 tonnes of contained copper (according to major mining firms Codelco and Peñoles, no less).

Remember, that’s $7 million in 2012 money.

Then the wheels fell off.

First, their executive chairman Gerry Nealon died in 2013. Tragic, but his death derailed the project completely.

Colin Bird took over, refocused the company toward Africa, and Eureka became the asset nobody wanted to talk about. By the time Ajax came knocking in early 2025, Bezant accepted just $170,000 in cash. No deferred payments. No royalties.

Just cash and goodbye.

For context, that’s a 97.6% discount on a project that was mined for four centuries.

What Exactly Is Eureka?

Eureka sits in northwestern Argentina, in Jujuy Province, about 4,000 metres above sea level. It’s not some greenfield exploration punt in the middle of nowhere.

This thing has been in production since the Incas, then the Jesuits in the 16th century, then various operators between 1885-1908, 1950-1960 and finally the 1970s-1980s.

Historical production estimates suggest around 9,000 ounces of gold and 2,000 tonnes of copper came out of this ground using pickaxes and swearing.

The underground workings at Mina Eureka have almost 2,000 metres of development. It’s now largely flooded, but the key point is this:

Nobody ever drilled it properly.

Not in the 1980s. Not in the 1990s. Not in the 2000s.

Never.

The geology is strong. You’ve got Red Bed-type copper oxide mineralisation in loosely consolidated conglomerates – think Corocoro in Bolivia, which hosts 80-100 million tonnes at 0.6% copper.

The copper mineralisation at Eureka occurs in discrete horizons, with grades ranging from 0.1% to 6.3% copper. Surface sampling has returned values up to 6.1% Cu, with numerous samples above 0.5% Cu.

Then you’ve got the gold.

Two types, actually:

Primary gold in quartz veins within Ordovician sediments (these veins can be up to 10 metres wide)

Secondary placer gold in the conglomerates of the Eureka Formation

Mantos Blancos (now part of Anglo American) estimated a historical resource of 52,000 ounces of gold at 2.7 g/t back in the day. But a 2007 NI 43-101 report suggested the placer gold potential could be several times larger than this estimate.

Nobody bothered to test it.

Historical Estimates

Now, I need to caveat this heavily: these are NOT JORC-compliant resources. They’re historical, they’re not verified by modern standards and you absolutely should not treat them as bankable.

But they’re instructive.

Codelco’s work:

Undiluted resource: 2.04Mt at 2% Cu (40,800t contained copper)

Diluted resource: 13.1Mt at 0.36% Cu (47,160t contained copper)

Exploration potential: 52Mt at 0.35% Cu (180,000t contained copper)

Peñoles’ work:

Resource estimate: 52Mt at 1% Cu (520,000t contained copper)

Exploration potential: 61.6Mt at 1% Cu (616,000t contained copper)

Codelco is one of the world’s largest copper producers. Peñoles is a serious Mexican mining company. Their work consisted of extensive trenching, test pits, sampling and induced polarisation surveys.

The difference between Codelco’s and Peñoles’ estimates? Peñoles did more work. More trenching, more sampling, a 2,200-metre IP survey covering 1.5km x 3.5km.

The geological target didn’t change – just the understanding of how big it might be.

What Ajax Is Doing

On 8 December 2025, Ajax received formal approval for its Environmental Impact Study from the Director of Mines and Energy Resources for Jujuy Province.

This was the green light to drill.

6 January, they mobilised the rig.

On 12 January, drilling commenced.

The initial programme is 10 diamond drill holes for approximately 1,500 metres. They’re targeting:

Shallow geochemical and IP anomalies where surface sampling has already confirmed high-grade copper oxides

A deeper IP chargeability anomaly identified in a 2014 SRK report – this is potentially the big one, as it may represent the transition zone to a sulphide-rich feeder system beneath the oxide cap

Areas in close proximity to the historic Mina Eureka workings, where 400 years of mining never went deep enough to test the modern geological model

The deeper chargeability target is particularly interesting. In porphyry and Red Bed-type systems, you often find oxide mineralisation near surface (which is what’s been mined historically) overlying a much larger sulphide body at depth.

If that SRK anomaly represents this transition zone, the scale of the system could be substantially larger than the historical estimates suggest.

After this initial phase, there’s a planned 4,000-metre follow-up programme designed to expand coverage and work toward a maiden JORC-compliant resource in H1 2026.

By mid-2026, we should have the first modern resource estimate for a project that’s been mined since the 1500s.

The market is currently valuing Ajax at less than a £10 million enterprise value. If they hit anything close to Codelco’s minimum estimate…

Gold Wildcard

Gold is above $4,600/oz and rising.

Under the terms of Ajax’s acquisition of the La Norteña licence (which neighbours Eureka to the north), there’s an agreement to exploit alluvial gold down to 6 metres depth. The vendor gets 20% of profits; Ajax covers all costs.

The company suggests production of just 150 ounces per month could generate around $5.8 million per year at current gold prices.

That’s potentially twelve months away.

At $4,600/oz (versus the $2,500-$3,000 assumptions when this deal was structured), those economics just got substantially more attractive. We’re talking about potential annual revenue of around $8.3 million from 150oz/month production.

This isn’t even the main game – it’s just alluvial gold sitting near surface that they can process while they’re drilling the main copper-gold target.

The broader gold story at Eureka hasn’t been properly evaluated.

The 52,000-ounce historical estimate only covers one small area.

The 2007 report suggesting ‘several times’ this amount in placer potential was never followed up. The Ordovician quartz veins – some up to 10 metres wide with visible gold – were never systematically drilled.

Codelco didn’t even try to assess the gold potential across the district. They were focused on the copper.

Land Grab

Since acquiring Eureka in May 2025, Ajax management has been systematically consolidating the district:

May 2025: Acquired Minas La Escondida – 2,500 hectares contiguous to Eureka for US$80,000. Includes a tailings dam below Mina Eureka that nobody’s assessed yet.

August 2025: Acquired La Norteña – 6,300 hectares north of Eureka for US$22,500 (plus the alluvial gold profit-share deal mentioned above). Applied for three additional licence areas covering 334 hectares.

December 2025: Signed heads of terms for Rachaite – 200 hectares, another former Alexander Mining property with historical drilling showing up to 15.3 g/t silver, 1.66% zinc, 0.46% lead and 2.4 metres at 0.39 g/t gold.

The really interesting bit about Rachaite?

There’s a 1985 estimate by SEGEMAR (the Argentine geological survey) describing approximately 5 million tonnes of mineralisation at 0.7% lead, 1.5% zinc and 200 ppm silver. That’s roughly 35,000 tonnes of lead, 75,000 tonnes of zinc and 32 million ounces of silver.

Now, this estimate is ancient, it’s not verified, it predates modern standards, and you shouldn’t rely on it for anything.

But Ajax is paying $20,000 in shares for a 90-day look, with the purchase price of $380,000 only payable 36 months after EIA approval if they decide to exercise the option.

That’s how you do it. Low-cost options on high-potential targets. If it works out, you’ve bought it cheap.

If it doesn’t, you’ve lost almost nothing.

They’ve gone from 7,000 hectares to roughly 14,000+ hectares in eight months, all for less than $300,000 in cash.

The entire Eureka district is becoming an Ajax landholding.

The Other Assets: Pereira Velho, Leon and Paguanta

Ajax isn’t just a one-asset story. They’re putting together a portfolio of orphaned, underexplored South American assets that can be brought to account quickly.

Pereira Velho (Brazil)

This one’s key because of who’s selling it: Appian Capital Advisory, one of the world’s largest specialist mining funds. They developed and sold the nearby Mineração Vale Verde copper-gold project to Baiyin Nonferrous for $420 million in cash last year.

Now they’re selling Pereira Velho to Ajax and becoming a material shareholder. Think about that dynamic. Appian could have kept this project. They could have put it into another vehicle.

Instead, they’re selling it to Ajax and taking shares, potentially positioning Ajax as their preferred vehicle for projects that are too early-stage or too small for their direct consideration.

The asset:

14,596 hectares in Alagoas State, Brazil

2.5km+ gold-in-soil anomaly

Historical resource estimate of 350koz gold (oxide and fresh, not JORC-compliant)

Over 80% oxidised mineralisation (free gold, amenable to heap leaching)

6,363 metres of diamond drilling completed between 2018-2022

The deal:

$200,000 cash at completion

$400,000 from Appian subscribing for shares at 5.5p (making them a material shareholder)

$1.5 million in shares if Ajax delineates a JORC-compliant measured resource of 350koz+ gold

2.5% NSR royalty (buyable for $1.5 million within three years of production start)

At $4,600/oz gold, that 350,000-ounce target has an in-situ value of $1.6 billion. Obviously, you don’t get anywhere near that as a junior explorer – you’re talking resource multiples, not spot prices – but the point is the leverage to gold prices is enormous.

The metallurgy is straightforward (heap leach oxidised material), the infrastructure is there, and the jurisdiction is mining-friendly.

Ajax is paying $600,000 upfront for an asset with 350,000 ounces of historical resources. If they hit the earnout target and pay the full $1.5 million, they’re all-in for $2.1 million for what could be a 350koz+ JORC resource in a heap-leach scenario.

That’s $6 per ounce.

In a $4,600/oz gold environment.

Leon (Argentina)

This is the former Alexander Mining project in Salta Province, 55km southeast of Salta city. Alexander reportedly spent $25 million on this between 2005-2010, including over 10,000 metres of drilling.

Historical JORC (2004) resource: 6.6Mt at 0.62% copper and 18 g/t silver (indicated and inferred, oxide horizon only).

There’s also a historical resource (non-compliant) of 44.7Mt at 0.8% Cu and 21.8 g/t Ag that was never properly followed up.

The deal:

$3 million purchase price + $100,000 in Ajax shares

Payable 36 months after EIA approval (so not for three years)

$1 million minimum work commitment after EIA approval

0.5% NSR (buyable for US$450,000)

Ajax is essentially getting a free look at a project where someone else spent $25 million. If they can’t make it work, they walk away having spent the minimum exploration commitment.

If they can expand the resource – particularly into the deeper sulphide zones that Alexander never properly targeted – they’ve got a serious copper-silver asset for a deferred payment structure that costs them nothing today.

Paguanta (Chile)

This one’s coming from ASX-listed Asara Resources, who want to focus on their Guinea gold assets.

The asset:

7,800 hectares in northern Chile’s Tarapacá region

JORC-compliant resource: 6.8Moz silver, 265Mlb zinc, 74Mlb lead (at Patricia prospect)

Resource is open at depth and along strike

Deepest hole ended in mineralisation: 1,765 g/t Ag, 12% Zn, 7.5% Pb, 1.7 g/t Au

Located on northern extension of Chile’s West Fissure (world’s largest concentration of porphyry copper-molybdenum deposits)

Surrounded by BHP and Codelco claims

The deal (revised terms):

$37,500 cash + $37,500 in Ajax shares at completion

$500,000 on defining a proved reserve >25Mt at ≥5% zinc equivalent

$500,000 on defining a proved reserve >5Mt of copper

1% NSR capped at US$500,000 (starting one year after production begins, subject to zinc >US$2,600/t)

This is Ajax acquiring 74.81% of a JORC-compliant 6.8Moz silver resource for US$75,000 upfront. The zinc price is currently around US$2,989/t, well above the NSR threshold.

The resource is already compliant, so no maiden resource risk. And they’re in a district surrounded by major miners who clearly see value in the region.

The fact that the resource remains open at depth – with the last hole ending in 1,765 g/t silver, 12% zinc, 7.5% lead, and 1.7 g/t gold – suggests this could be substantially larger than currently defined.

The Strategy: Fire Sale Acquisitions + Rapid Value Crystallisation

Here’s what Ajax is doing, and it’s brutally simple:

Buy orphaned assets at massive discounts – Projects with historical production, historical resources and historical drilling that got abandoned for non-technical reasons (management changes, focus shifts, funding issues).

Consolidate the district – Don’t just buy one licence. Buy everything around it. Control the entire play.

Drill quickly and efficiently – These aren’t greenfield punts. They’re brownfield targets with known mineralisation. You’re not searching; you’re defining.

Crystallise value with JORC resources – A historical estimate is interesting. A JORC-compliant resource is bankable. That’s where the re-rating happens.

Keep the burn rate at zero – No head office. One cash salary. Everything else in equity. This matters enormously. They raised £1.2 million at 5.5p in December, and they’re currently sitting on approximately £2.6 million in cash. At their current burn rate, they’re funded through to October 2026 – well past the maiden Eureka resource expected in H1 2026.

The Appian relationship is particularly clever. If Ajax successfully develops these assets, they become Appian’s go-to vehicle for projects that don’t meet Appian’s size threshold.

That’s a huge strategic advantage.

Appian has deep pockets, extensive South American experience and a network that could funnel deal flow to Ajax.

The Jurisdictional Question

Yes, we need to talk about this. Ajax’s projects are in Argentina, Chile and Brazil.

But let’s be specific:

Argentina (Jujuy Province): Javier Milei took office in December 2023 and has been focused on economic reform. His party made significant gains in the recent midterm elections. Inflation is stabilising. It’s mid-tier in mining jurisdiction terms, but the new world being built has seen it rise higher in recent years.

Chile: Just elected Jose Antonio Kast in a run-off on December 14, 2025. He’s from the Republican Party, seen as more business-friendly than the previous administration. Chile has operated a hybrid state/private mining model for decades. It ranked in the top 10 globally for mining investment attractiveness as recently as 2018 and ticked upward in 2024.

Brazil: Lula’s back, and there’s some concern about statist policies. But mining represents 4% of GDP and $10 billion in annual exports. Brazil’s economy grew 3.4% in 2024 (better than expected). The mining code is well-established, foreign companies can hold 100% ownership, and the infrastructure in core mining regions is solid.

Are these Canada?

No.

But they’re also not the DRC.

And here’s the thing: if you want assets at fire-sale prices, you’re not buying in Saskatchewan. The discount Ajax is getting on these projects exists because they’re in less fashionable jurisdictions.

That’s the trade-off.

The Corocoro comparison is worth keeping in mind. That deposit in Bolivia – right next door to Eureka – hosts 80-100 million tonnes at 0.6% copper. Eureka shares the same regional geology.

If there’s even a fraction of that scale at Eureka, the jurisdictional concerns become secondary very quickly.

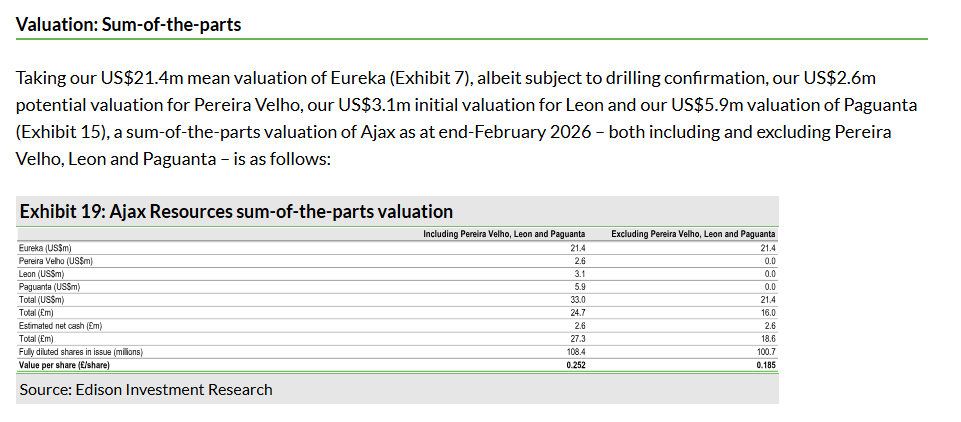

Valuation Puzzle

There’s an Edison research note out there with a sum-of-parts valuation (and underneath a stretch target).

I could plug in slightly different numbers but basically there’s little point. The logic is sound and you can’t really argue with it.

But we’re not here for the base case - or even Edison’s stretch.

That’s boring.

If Ajax hits something close to Peñoles’ exploration potential at Eureka, and if the gold mineralisation is several times the 52,000-ounce historical estimate, and if they successfully expand Leon and Paguanta...

You can see how this gets to significant multiples from the current price.

The company itself has suggested a maximum blue-sky scenario (assuming top-end resource estimates and full exploration success at all projects) could support a valuation north of £1/share.

I’m not going to make that claim – it requires too many things to go right. But the point is, there’s optionality here.

Catalysts

Q1 2026: Preliminary assay results from the initial 1,500m Eureka drilling programme

H1 2026: Maiden JORC-compliant resource at Eureka (this is the big one)

Early 2026: Completion of Pereira Velho acquisition and start of Phase 1 exploration

Early 2026: Potential completion of Paguanta acquisition (subject to due diligence)

2026: Potential commencement of alluvial gold production at La Norteña

The maiden Eureka resource is the inflection point. That’s when the market will have to reconcile the share price with an actual, verified, JORC-compliant resource number.

If they hit anywhere near Codelco’s numbers, the re-rating should be immediate. If they hit anywhere near Peñoles’ numbers, it’s going to be violent.

And that’s just Eureka. Pereira Velho, Leon, and Paguanta are all additional free options.

The Risks (Because There Are Always Risks)

Let’s be clear.

Drilling risk: The historical estimates might be wrong. The mineralisation might not be where they think it is. The grades might be lower than expected. This is the nature of exploration.

Resource conversion risk: Even if the drilling is successful, converting historical estimates to JORC compliance isn’t automatic. It requires proper QAQC, appropriate drill spacing, and competent person sign-off.

Jurisdictional risk: Argentina, Chile, and Brazil all carry political risk. Permitting delays, tax changes, royalty increases, or outright expropriation are possible (though unlikely in these specific jurisdictions).

Funding risk: If the projects are successful, Ajax will need significant capital to develop them. That means dilution, debt or selling assets. The current £2.6 million cash pile covers exploration through October 2026, but not much beyond that without further fundraising.

Management execution risk: Ippolito Cattaneo is young (relatively speaking, so am I), and Ajax is a small team. Executing a multi-asset strategy across three countries is ambitious. Can they deliver?

Market risk: Junior mining stocks are volatile. Even with great drill results, the market might not care if we’re in a risk-off environment or if gold/copper prices decline.

That said, the risk/reward here looks asymmetric.

Gold Price Context

We can’t ignore the macro backdrop here. Gold at $4,600/oz is a different world from the $1,800-$2,000 environment when most of these deals were structured.

The Eureka gold potential – largely ignored in favour of the copper story – suddenly becomes much more interesting. The La Norteña alluvial gold play, which was pencilled in at maybe US$5.8 million/year in revenue at $2,500/oz gold, is now looking at potentially US$8.3 million/year at $4,600/oz.

Pereira Velho’s economics transform. An oxide, heap-leach gold project in Brazil with 350,000+ ounces of potential JORC resources wasn’t that exciting at $2,000/oz gold. At $4,600/oz? That’s a different conversation entirely.

And here’s the thing about gold juniors in a $4,600/oz environment: the market starts paying up for optionality. A 52,000-ounce historical estimate that might be several times larger on a brownfield project with extensive historical workings? That gets attention.

Ajax positioned itself as a copper-gold story. The copper is the headline - and yes, copper is at a record high.

But the gold might end up being the real story, especially if we stay in this elevated price environment.

Why This Might Actually Work

I’ve looked at a lot of junior mining companies over the years, and most of them are varying degrees of shit.

Overpromising, underfunded management teams who treat the company as a lifestyle business, projects in jurisdictions where nothing ever gets built, and resources that turn out to be barely coherent intersections of slightly-above-background mineralisation.

Ajax doesn’t fit that mould, at least not yet. Here’s why I think this could actually work:

1. They’re buying assets with historical production. This isn’t some ‘we found elevated copper in soil samples’ story. Eureka produced for 400 years. That’s proof of concept. The question isn’t ‘is there mineralisation?’ but ‘how much is there and can we define it economically?’

2. The historical estimates come from credible sources. Codelco and Peñoles aren’t junior prospectors. They’re serious mining companies with reputations to protect. Their estimates might not be JORC-compliant, but they’re not nonsense either.

3. The acquisition prices are absurd. $170,000 for Eureka. $75,000 for Paguanta. These aren’t normal transaction prices. This is distressed selling by companies who want out. Ajax is getting assets for cents on the dollar.

4. The cash burn is minimal. One cash salary. No head office. Everything else in equity. At current burn rates, they’re funded into late 2026. That’s discipline. I like it.

5. The land consolidation strategy makes sense. Don’t just buy one project – buy the whole district. Control all the prospective ground. Then drill systematically. This is how you build a real company, not a one-asset lottery ticket.

6. The Appian relationship is strategic. Having one of the world’s largest specialty mining funds as a material shareholder and potential deal flow source is a massive advantage. Appian knows these jurisdictions, they have deep pockets, and they just sold a Brazilian project for $420 million. They’re not backing Ajax out of charity.

7. The timing is right. Copper demand is insane (EVs, grid infrastructure, data centres). Gold is at $4,600/oz. Silver is rocketing. These are ideal market conditions for what Ajax is trying to do.

Could it all go wrong? Absolutely. The drilling might disappoint. The JORC resource might come in at the low end. Permitting could drag on.

But if you’re going to play in the junior resource space, you could say the same of everyone else.

The Bottom Line

I’m not going to sit here and tell you Ajax is a guaranteed ten-bagger. It’s not. This is a speculative junior explorer with execution risk, jurisdictional risk, and geological risk.

But I will say this: the risk/reward looks compelling from current levels.

If the Eureka drilling confirms even Codelco’s minimum estimate, this stock should rerate significantly. If it confirms Peñoles’ numbers, we’re talking about a potential revaluation that would be... substantial.

Add in the gold upside (which nobody’s really pricing in), the Pereira Velho optionality in a $4,600/oz gold environment, and the free options on Leon and Paguanta, and you’ve got a setup where a lot has to go wrong for you to lose money, but only a few things have to go right for you to make a lot.

The maiden resource in H1 2026 is the key catalyst. That’s when we find out if this is a real copper-gold district or just another junior mining disappointment. But given the historical production, the work done by Codelco and Peñoles, and the fact that this thing was mined successfully for four centuries, I’d argue the odds are tilted in favour of real district.

The market is currently valuing Ajax as if Eureka is worth almost nothing. That’s either correct, and the historical estimates are all wrong, or it’s incorrect, and this reprices.

We’ll find out in the next few months.

Finally, Ippolito is hungry. He compares Ajax to an early Amaroq & Eldur, and I’ve also heard comparisons with Guardian’s Oliver.

I usually attend the London mining conferences and occasionally make the effort to go to Future Minerals in Saudi and Indaba in Cape Town.

Almost everyone I speak to is old, wealthy and coming to the end of their careers. This is to be admired; mining is in the blood and nobody gives it up easy.

But young blood has something to prove, and in the case of Oliver and Eldur, it’s yielded fantastic results.

As students of classical mythology will know, Ajax the Great was outwitted by Odysseus in a verbal duel for Achilles’ armour by popular decision of the Greek army.

It didn’t end well for him, but the good news is that the frontman of this new greater Ajax seems to sport a better oratory.

Strong assets, energetic management.

Back Ajax.

Nice one. Thanks for the detailed write up.

Charles, have you studied the LCM agreement? I see elsewhere quoting that from Jan 25 interest at 30%pa, compounding monthly, is due on the award. That will mount very quickly, if indeed it starts at that point. But it's not clear to me if it does start at 01/01/25, or the date the final appeals are decided.